MicroStrategy (MSTR), the technology company led by Michael Saylor, has captured the attention of financial markets thanks to its bold investment strategy in bitcoin (BTC).

Hailed by some as a masterstroke, its approach has been replicated by several companies. However, some analysts They consider that this strategy could be getting dangerously close to the brink of collapse.

Is MicroStrategy playing with fire by going deeper into debt to buy bitcoin? Mike Fay, a market analyst, has warned about what he calls “the infinite money error.”

The renewed interest in MicroStrategy comes from its innovative strategy of using bitcoin as a primary treasury asset. Investment in digital currency has led its shares to rise significantlybeing one of the favorites among cryptoactive investors.

In fact, the success has been such that the company reached a new milestone by seeing its stock exceed $227 last Monday. Thus establishing a new historical maximum, as seen in the following graph of TradingView.

This renewed enthusiasm is due to the perception that MicroStrategy has found a profitable formula: borrow at low interest rates and use those funds to acquire more bitcoin.

Analyst Mike Fay highlights how the company has managed to turn low-cost debt into an asset that has historically generated high returns, far exceeding the interest paid on the loans. But this strategy, although effective in the past, is fraught with risks, and Fay thinks it could come to a head.

What is the “infinite money bug”?

The logic behind the “infinite money bug”: MicroStrategy continues to accumulate debt at low interest rates, using its cash flow generated by the software business to cover the interest.

Meanwhile, buy bitcoin in the hope that its price will continue to rise in the long termwhich would increase the value of the company’s shares, says the analyst.

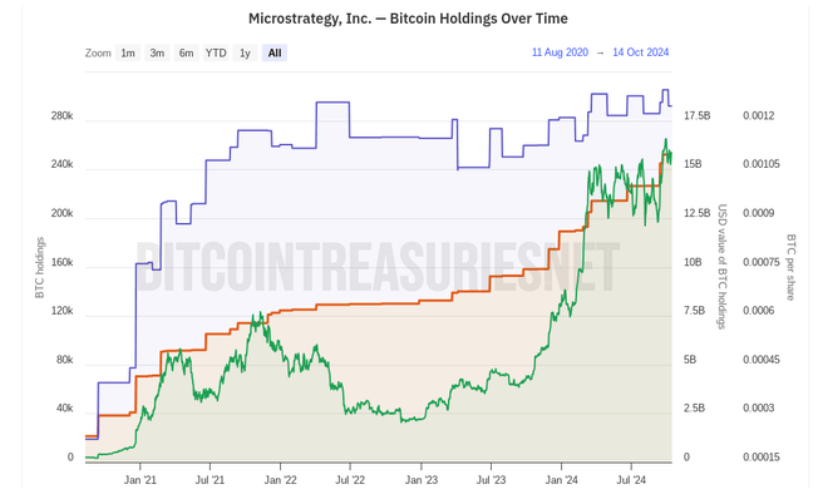

This strategy has so far allowed the company to post a 2.9% increase in the value of BTC per share so far this year, according to Bitcoin Treasuries data.

The company’s optimistic projection suggests that this yield will continue to grow at an annual rate of 4% to 8% between 2025 and 2027. However, Fay is not convinced that this strategy can be sustained in the long term.

In his view, the biggest risk is that MicroStrategy’s capital depends more on speculation around bitcoin than on revenue from its core software business. The money that comes in from that part of the business is used to pay the interest on the debt.

A dangerous flywheel

Last June, the American company announced its intention to raise $700 million to buy more bitcoin, through a private offering of convertible senior notes due 2032aimed at qualified institutional investors. These bonds offer periodic interest and guarantee the return of capital at maturity, as reported by CriptoNoticias.

However, Fay raises questions about the company’s ability to continue financing these purchases with long-term debt. While the company has so far managed to generate positive returns, Fay warns that the time could come when MicroStrategy is forced to sell part of its BTC holdings to cover their debt commitments.

The risk is obvious: if the price of bitcoin falls, MicroStrategy’s value will also plummet, affecting shareholders. Besides, The increase in the company’s operating costs is beginning to be a warning sign.

In the second quarter of 2024, general and administrative expenses represented 63.2% of incomea figure that could complicate the company’s long-term stability.

“Personally, I think it is more prudent to invest capital in bitcoin directly or in one of the spot ETFs at this time. A 160% premium on BTC holdings through MSTR implies a BTC price of $171,000.”

Mike Fay, financial analyst.

Should BTC reach that price, the best performance from now on will be in BTC instead of MSTR, the analyst says. “I could certainly be wrong again, but I prefer to buy the asset that I know MicroStrategy will buy instead of buying [las acciones] MSTR,” he adds.

Stony Chambers dissents: an exaggerated risk

Despite these warnings, the analysis firm Stony Chambers has a different view.

According to this firm, the fear that MicroStrategy shareholders do not actually own the BTC that the company reports on its balance sheets is “very misplaced.”

This concern arises from the fact that BTC assets are managed by a subsidiary called MacroStrategy, which some have interpreted as a sign that shareholders do not have direct control over the assets.

However, the firm clarifies that MacroStrategy assets are protected from creditor claims and that shareholders maintain legal rights over those BTC.

In his opinion, this logic is “totally absurd and probably just comes from a bad place of trying to create sensationalism to get attention.”

What’s more, Stony Chambers believes MicroStrategy stock should rise even further as the company has demonstrated an effective ability to increase the value of BTC per share.

According to the firm, MSTR shares are a clear buy, arguing that the company has been able to integrate bitcoin as a fundamental part of its financial strategy.

Companies that follow in the footsteps of MicroStrategy

Despite the doubts of some analysts, MicroStrategy’s strategy has inspired other companies. Metaplanet Inc., a Japan-based company, has adopted bitcoin as its primary reserve asset, with surprising results.

The company raised its reserve to more than 855 BTC, which caused the shares to rise 15.7% in a single daygoing from 6.40 dollars (955 yen) to exceeding 7.37 dollars (1,255 yen) on October 15, as seen in the graph provided by TradingView.

On the other hand, Samara Asset Group, a company based in Malta, has also announced the issuance of bonds for 30 million euros to acquire bitcoin.

Both companies are following in MicroStrategy’s footsteps, betting that bitcoin’s value will continue to rise and that the strategy of using it as a reserve asset will generate benefits for its shareholders.

Although MicroStrategy’s bets have paid off so far, warnings about its dependence on BTC and its growing debt cannot be ignored. While it is true that the company has achieved a balance so far, its ability to maintain this strategy will depend on the behavior of the bitcoin market and its ability to generate stable income in its core business.