The stablecoins could reach 3 billion dollars in capitalization by 2028.

If the Genius law would legitimize the stablecoins, strengthening the dollar.

The next time you slide your Visa or Mastercard card, hold a moment to think that behind that daily familiarity, there is a silent trend rewriting the rules of money, and the old monarchs barely realize that the crown no longer adjusts them so well.

Think about the volume of payments processed by a giant as a visa. Now, imagine a digital network that, in certain aspects, already moves twice that volume. Well, that is not a futuristic projection; It is the current reality of the stablecoins, A phenomenon that is silently redefining who holds true power in the global capital flow.

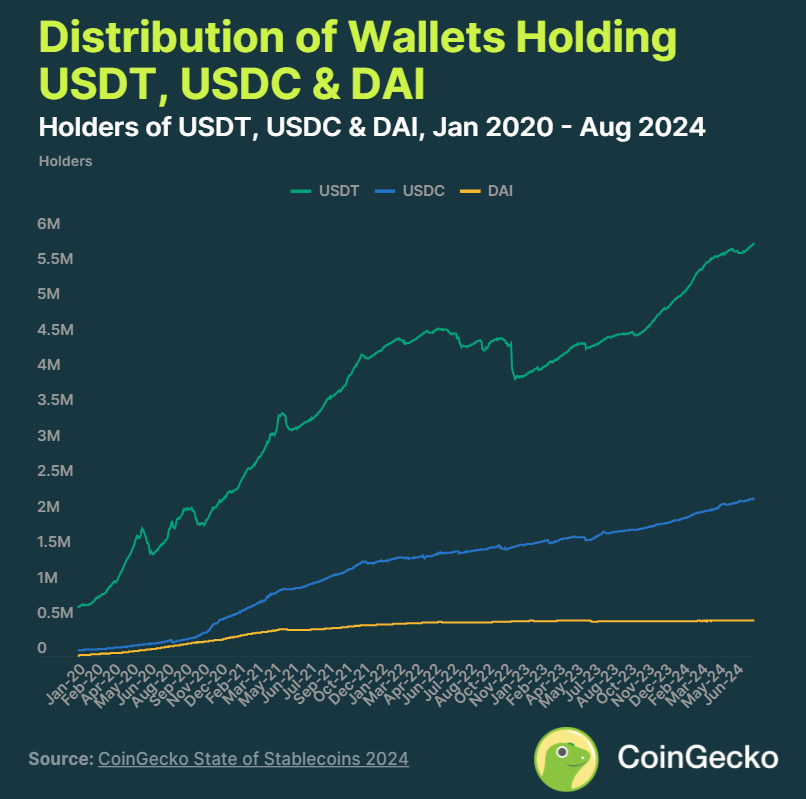

The mirage of traditional dominance becomes evident when confronting figures. A report Recent of Messari, on the state of the stablcoins in the first quarter of 2025, illustrates how the combined capitalization of the main stablcoins exceeded 200 billion dollars.

The figure demonstrates a growth of more than 48% if we compare it with the total market capitalization of the stablecoins, which in March 2022 reached a maximum of 182 billion dollars. This before falling to 135 billion dollars at the end of 2022 after Terra’s collapse, according to A Coingcko report.

The anatomy of this new domain of the stablecoins is based on fundamental pillars that inherited systems fight to match. Efficiency and speed are essential.

On-Chain analysis platform data such as Dune Analytics reveal that networks like tron, processing more than 69% of the USDT volumeconsistently keep rates of transaction below a dollar and second confirmation times. This contrasts with the congestion and high costs that often plague even pioneer networks such as Ethereum, or with the slowness and opacity of traditional cross -border transfers, which, which According to the World Bank They can cost more than 6%on average.

Global adoption of stablcoins and accessibility without borders

But the scope goes far beyond simple technical efficiency. The accessibility and global adoption of The stablecoins are redefining the panorama. Cryptootic reports have highlighted the high adoption of them in Latin America, something that is also happening in other parts of the world such as Southeast Asia and Sub -Saharan Africa. Its use expands in global finances.

Growth is simply exponential. The fact that they already represent, according to estimates of analysts such as Bernstein Research or Vaneck, a market capitalization of up to 2.8 billion dollars for 2028They are a chronicle of a power.

This maturity and systemic relevance are now reflected in the regulatory action that the United States is promoting that is on the verge of registering a milestone with the imminent approval of the Genius law that proposes a regulation for the stablecoins.

If this law is approved, this would represent the first comprehensive federal legislation for the regulation of the stablecoins and, by extension, the first significant legal framework for digital assets in the country. This movement, far from stopping the trend, could legitimize it and accelerate its institutional adoption by providing a framework that grants clarity and security to the industry.

From the Bitcoin Policy Institute it is mentioned that the genius law, by providing “clarity and security to the industry”, could promote the growth of the stablecoins, aligning with the objectives of the US Treasury Department. UU. To expand the dollar system and strengthen the demand for sovereign debt.

Regulation in progress: the impact of the genius law

The Genius bill is now in a process of debate and revision of amendments, within which the most highlighted is the possibility that the regulation for the Stablecoins includes the entire text of the Law of Credit Cards (CCCA), which was presented by Senator Roger Marshall (Republican by Kansas) and co -written with Senator Durs (Democrat by Illinois).

The CCCA was initially introduced in 2022 and reintroduced in 2023, but has faced obstacles for a strong opposition from banks and credit card companies, especially Visa and Mastercard.

The objective of the initiative is break the mastery of the credit card market in the US.which is mainly controlled by Visa and Mastercard. These two companies represent approximately 83% of the general purpose credit cards, according to data from the Federal Reserve, and processed transactions for more than 3.4 billion dollars in 2021, generating 93 billion dollars in commissions for merchants in 2022.

These commissions, which include both exchange rates and network rates, are considered by the proponents of the CCCA and excessively high and a factor that contributes to inflation, since the costs are transferred to consumers in the form of higher prices.

In that sense, the CCCA proposes to reform the payment market demanding that banks with assets exceed 100 billion dollars allow Electronic credit card transactions are processed by at least two non -affiliated networksone of which cannot be visa or mastercard.

Convergence of stablcoins and credit cards: a unified future?

Although at first glance the Genius law and the CCCA seem to address different issues (credit cards and cryptocurrencies), the meeting point is in the shared objectives of promoting competition, reducing costs in payment systems and regulating the role of financial institutions in electronic transactions.

Both projects seek to diversify and modernize payment systems by introducing alternatives that challenge the control of established financial institutions. The CCCA aims to weaken the Visa and Mastercard duopoly, while the stablecoins offer an alternative route for digital transactions that do not depend on traditional card networks. The integration of the CCCA in the Genius Act reflects an effort to align these reforms under a broader vision of competition in electronic payments.

In such a way that if approved, the combination of these reforms could Accelerate the adoption of stablocoins as an alternative to credit cardsespecially in sectors where processing rates are an obstacle. For example, these cryptoactives could be integrated into point -sale systems for merchants, competing directly with card networks.

In short, Stablecoins are reconfiguring the global financial landscape, challenging the hegemony of traditional payment systems with unprecedented efficiency and accessibility. Its rapid growth and mass adoption, backed by regulatory frameworks such as the Genius and potential law. This convergence of regulation and technology indicates a future in which the stablecoins, projected to reach 3,000 million dollars by 2028, They could redefine financial power, leaving traditional giants fighting to maintain their crown.

Discharge of responsibility: The views and opinions expressed in this article belong to its author and do not necessarily reflect those of cryptootics. The author’s opinion is informatively and under no circumstances constitutes an investment recommendation or financial advice.