In a world where Bitcoin (BTC) has gone from being a technological curiosity to a coveted asset, a group of companies has decided not only to adopt Bitcoin, but to turn it into the pillar of its financial strategy.

Microstrategy, now called Strategy, leads this movement, and is imitated by many others such as Metaplenet, Twenty One and Nakamoto.

In the last month, new Bitcoiners treasures have been launched. Among them, those of Gamestop, Zap Solutions, Roxom (this is an Argentine company), H100 Group, Walnut, Greenmerc and Atai.

These and other companies have opted strong, accumulating thousands of BTC in their balances. But corporate frenzy, which implies issuing debt and selling actions to finance mass purchases of Bitcoin, has lit the alarms.

Is this a financial revolution or a bubble about to explode? In the words of who identifies in the social network X as “lowstrife”, It is of a “toxic leverage” that could be, in his opinion, “the worst that has happened to Bitcoin and what it represents.”

Corporate bitcoin fever

Companies that have adopted Bitcoin as the treasury asset are not limited to buying and maintaining it. The strategy of many are more complex and potentially dangerous.

These companies use a financial feedback cycle: Bitcoin acquire with their own funds, they incorporate it into their balances And then they use these assets as a basis for raising more capital through emissions of shares, bonds, loans or preferential actions.

This fresh money is immediately destined to buy more bitcoin, feeding a financial “wheel” that seems not to stop.

For example, Strategy, directed by Michael Saylor, has turned this practice into an art. The company, which was originally dedicated to business intelligence software, currently owns 580,250 BTC, which makes it the public contribution company with the highest Bitcoin holdings.

To finance these purchases, Strategy has resorted to mechanisms such as At-The-Market (Atm), a method that allows you to issue and sell new shares directly in the market. This approach, however, has a cost: the constant dilution of the value of the shares of existing investors.

“Toxic leverage” and its mechanisms

Lowstrife, who is a critical analyst of this practice, Describe the model as a “toxic leverage” Because it depends on a key metric: the multiplier of the net liquidation value (MNAV). The MNAV measures the relationship between the market value of a company and the value of its underlying assets, in this case, Bitcoin.

If the MNAV is greater than 1.,0, It means that the company’s shares quote above the value of their Bitcoin holdingswhich allows more capital to be raised by issuing new shares. Strategy has perfected this mechanism, using the ATM to issue shares and finance new purchases of Bitcoin.

However, this model has a critical weakness. If the MNAV falls below 1.0, as happened in 2022 and can be seen in the following graph, Strategy would face difficulties in raising capital.

In that scenario, The issuance of new actions further dilutes the value for existing shareholders, and the company’s capacity to maintain its strategy She looks compromised. “This is the mechanism by which this explodes,” Lowstrife warns, pointing out that the system depends completely on the feeling of the market, not, according to it – on solid financial foundations.

In addition to the ATM, Strategy uses instruments such as convertible debt and preferred actions to amplify their yields. Convertible debt, for example, It allows the company to issue bonds that can become actions in the futureprovided that the price of shares reaches a default level. At the moment, Strategy has 8.2 billion of dollars in convertible bonds with maturities between 2028 and 2032.

If the shares do not reach the necessary price for conversion, the company must refinance the debt or sell bitcoin to pay it, what could trigger a massive sale of its assets. Affecting Bitcoin’s price.

On the other hand, preferential actions, such as those of the Strategy Strf series, are a forms of perpetual debt that pays a fixed dividend of 10%. These actions have no expiration date, which means that the company must pay dividends indefinitely.

To finance these payments, Strategy resorts to the ATM again, diluting even more shareholders. Lowstrife criticizes this approach, arguing that today’s Bitcoin purchases are made “at the expense of the Shareholders of Tomorrow”. In an ambitious plan, Strategy intends to issue $ 21,000 million in preferential shares of the 8%series, which would require an annual dilution of 300,000 million dollars to cover dividends, according to the analyst’s estimates.

The risks of dilution and dependence on feeling

The Strategy model and other similar companies not only depends on the price of Bitcoin, but also on investor enthusiasm.

The MNAV, which reflects the perceived value of the company’s Bitcoin holdings, is an indicator based on the feeling of the market. “There is no mechanism or reason why you must quote the value of the assets,” says Lowstrife. If the MNAV falls below 1.0, the company’s capacity to collect capital collapses, which could trigger a descending spiral.

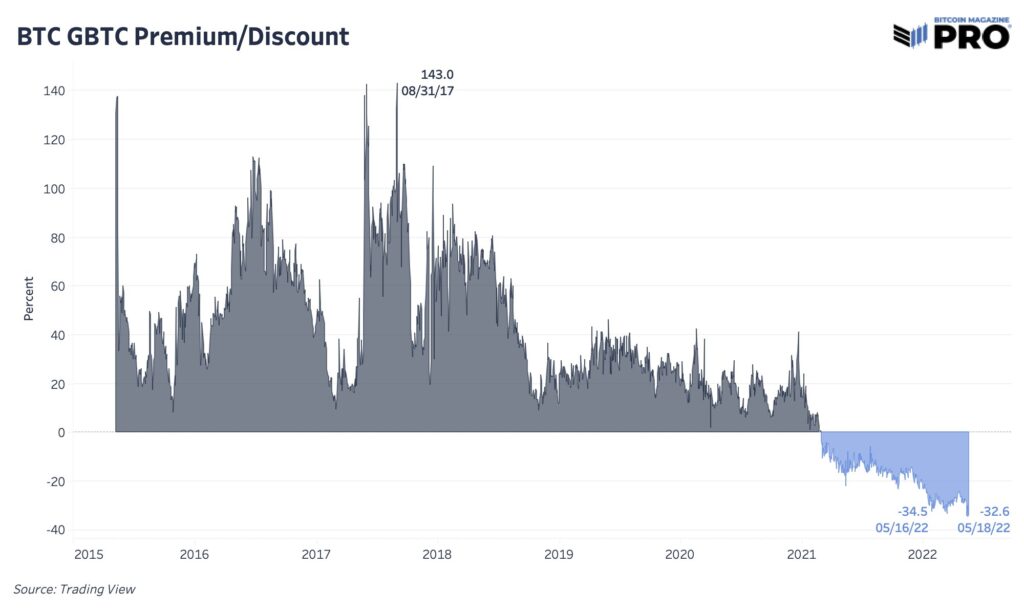

Lowstrife compares this risk with that of Grayscale Bitcoin Trust (GBTC), an investment vehicle that experienced drastic fluctuations in its appeal due to the feeling of the market. The following graph shows how the GBTC compared to Bitcoin’s value, He quoted with a premium of up to 143% in 2017, but also fell to a discount of -34.5% in May 2022reflecting how investors’ enthusiasm can fade.

But not all are critical of the model of issuing debt to accumulate BTC. Adam Back, a prominent figure in Bitcoin’s history, It offers a perspective different. He argues that, unlike a closed fund like GBTC, Strategy has flexibility as an operational company. In other words, if the MNAV falls below 1.0, the company could sell BTC to repurchase its own actions, stabilizing its value.

However, lowstrife Rebato that this strategy does not eliminate the risk, since selling BTC to finance repurchase could aggravate the fall of the MNAV and erode the trust of investors.

«Saylor has been in all podcasts, television interviews and tweets with millions of impressions saying one thing: you never sell your bitcoin. What do you think happens with the confidence in the company if you have to sell your bitcoin because they need cash flow or the MNAV is weak?

Lowstrife, market analyst.

Critical voices: A slap to the principles of Bitcoin?

The strategy of these companies has not only generated financial concerns, but also ideological criticisms. Lowstrife considers that this model is “a slap in the face of what is supposed to be Bitcoin”: an asset created to challenge the traditional financial system.

In his opinion, Strategy and other companies remember the financial engineering of 2008which led to the creation of Bitcoin as a decentralized alternative. «It is not a financial revolution. They are media scammers seeking leverage, ”he says.

Lunaticain, another critic and generator of content about Bitcoin, Share this vision. Describe the fashion of Bitcoin’s treasury as “the shitcoins and the ICO of this cycle”.

In the context of cryptocurrencies, shitcoins are digital currencies of doubtful quality or value, while ICO (initial offers of coins) were a popular form of fundraising in 2017-2018, many of which turned out to be speculative or fraudulent.

Although Lunaticain does not establish a direct connection with the lowstrife analysis, both share the concern that these companies are inflating their value artificially when linking with Bitcoin, instead of contributing to its genuine adoption.

A new metric for a new paradigm

In the midst of criticism, Strategy defends his approach with a bold argument: traditional financial metrics, such as profits per action (EPS), They are not suitable for assessing Bitcoin -centered companies.

Phong Le, CEO of Strategy, argues that Bitcoin is not only a financial asset, but a “transformative force” that redefines corporate finances. To reflect this, the company proposes new key performance indicators (KPI): BTC yield, which measures the income generated from Bitcoin holdings; the gain in BTC, which evaluates the growth in the amount of bitcoins possessed; and the gain in dollars in BTC, which reflects the increase in the dollars value of those holdings.

“Traditional metrics do not capture the real value generated by a company with BTC,” said Le. “We need to educate the world about what the relevant kpi are.”

However, the path taken by Strategy has not been exempt from controversy. A collective claim against Strategy alleges that the company and its executives, including Michael Saylor, have misrepresented the risks of their treasury strategy, minimizing Bitcoin’s volatility and presenting metrics that artificially inflate the value of the company. Demand maintains that these practices have left investors with devalued shares.

An optimistic model but with risks

As Strategy and other companies continue to accumulate Bitcoin, the risks accumulate to the same extent. The dependence of the MNAV, the constant dilution of the actions and the load of the convertible debt and the preferred actions create a system that, according to critics, is unsustainable in the long term.

If the feeling of the market changes or the price of Bitcoin does not meet expectations, These companies could face a liquidity crisis, forcing them to sell their Bitcoin holdings and triggering a fall in its market value.

For now, the enthusiasm for Bitcoin’s treasury continues to attract investors who see in these companies a form of indirect exposure to the digital currency. However, analysts such as lowstrife and lunaticoin resonate strongly: This model, far from being an evolution of Bitcoin’s spirit, could become his Achilles heel.