A “wave of circle imitators” is coming, anticipates Hayes.

The businessman suggests “trading this shit as if it were a hot dad.”

Arthur Hayes, co -founder of Bitmex and financial analyst, predicts that the digital asset market will witness a new collapse: the burst of the bubble of the stablecoins.

The businessman See risks In the accelerated success that is having the action of Circle (CRCL), a USDC Stable Currency company, on Wall Street.

As Cryptonoticias has reported on June 5, CRCL debuted in the New York Stock Exchange (NYSE) with a 168% rise compared to the price of its initial public offer (IPO).

In the following graph of TrainingViewthe great CRCL performance can be observed from its departure to the market until the time of writing this note.

In this regard, Hayes says: “Circle is extremely overvalued, but its price will continue to rise.” In his opinion, the price that investors are willing to pay for their shares It is not justified by their real performance or perspectives against competitors such as Tetherthe USDT station.

In other words, the analyst believes that a narrative is too optimistic and that attracts little informed investors who are paying for more for a company that still depends on Coinbase, the exchange of the United States. This is because Circle delivers 50% of its interesting interest in interest (NIM) to the platform in exchange for access to its client network.

Now, Hayes emphasizes that “this exit to the bag marks the principle, not the end, of the Stablcoins fever of this cycle” and states:

“The bubble will explode after the launch of a stablecoins issuer to a public market, probably in the United States, which separates the naive from tens of billions of capital through a combination of financial engineering, leverage and a spectacular talent. As usual, most of those who detach from their precious capital will not understand the history of the stablcoins and the payments within the cryptocurrencies What the ecosystem has evolved as it has done and what implications this has for the emitters that will be successful or not. ”

Arthur Hayes, co -founder of Bitmex and financial analyst.

Throughout his thesis, Hayes is skeptical and proposes a tour of the historical context that gave rise to the domain of the stablcoins, especially USDT. It is that, without this review, his warning on the bubble might seem a mere speculative opinion.

Thus USDT came to be the dominant stablecoin

Hayes recapitulation begins in 2015, when in the Grand China region (Hong Kong, Continental and Taiwan China), exchange platforms such as Bitfinex, Okcoin and Huobi faced a critical problem: local banks, under regulatory pressure, closed their accounts, hindering the movement of fiduciary money.

At that time, Tether offered a digital dollar that allowed rapid and cheap transfers without depending on the traditional banking system. In a market where Chinese investors sought to protect themselves from the devaluation of Yuan – like the one that occurred in August 2015 – and access dollars, USDT became a virtual “bank account”gaining the trust of the Asian cryptographic community.

Then, Hayes mentions the rise of the initial offers of coins (ICO) in 2017, a moment that consolidated Tether’s domain. It is that, at that time, platforms such as Poloniex and Binance, which could not operate with Fíat money due to bank restrictions, adopted USDT to offer altcoins exchange pairs, creating an economically significant network of users.

This integration, combined with the mass adoption in the global south (term that refers to economies such as Africa, Latin America and part of Asia), made USDT to the leading stablecoin, with unsurpassed profitability by not paying interest to their depositors. It should be clarified that Tether obtains profits mainly investing the money that supports USDT in assets such as United States Treasury Bonds, generating interest on these immobilized funds.

“Between 2015 and 2017, Tether achieved a product-market adjustment and created a competitive advantage over future competitors. Thanks to the confidence deposited in Tether for the Chinese commercial community, USDT became accepted currency in the main exchange platforms. At that time, it was not used for payments, but it was the most efficient way to transfer digital dollars inside and outside the capital markets cryptocurrencies, ”explains Hayes.

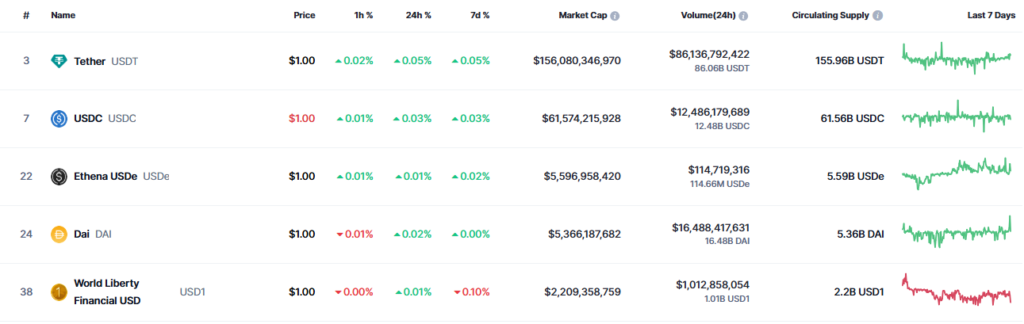

Currently, USDT is the most valuable stable, with a market capitalization that exceeds156 billion dollars.

A blunt example of Tether’s domain in the “global south,” according to Hayes, is Nigeria. In this country, where the local currency (Naira) suffers from high inflation and restrictions to access dollars, the stablecoins, especially USDT, have become a crucial alternative. Hayes recounts a conversation with a bank manager who revealed that approximately one third of Nigeria’s Gross Domestic Product (GDP) is managed in USDT, despite the efforts of the Central Bank for prohibiting cryptocurrencies.

This adoption, which arises “from below” and not by regulatory imposition, illustrates how USDT has penetrated economies with fragile financial systems. In that sense, he highlights: “By when regulators realize and try to act, it is already too late, since adoption is endemic in the population.”

For Hayes, this historical context demonstrates that the success of a stablecoin depends on its distribution channels – exchanges, social networks or traditional banks -, an access that new emitters cannot easily replicate.

That is why he states: “The western actors, many of whom raised money with the narrative of the payments with cryptocurrencies, rushed to create competitors for Tether. The only one who survived on a large scale was USDC of Circle. However, Circle is at a clear disadvantage because it is an American company based in Boston (how disgusting!) cryptocurrencies in the Great China. ”

At this point, Hayes’s analysis becomes more questionable. The derogatory mention towards Boston and the lack of development about what it implies “not having a connection with the Great China” weakens the argument, which relies more on personal impressions than in specific data.

The bubble begins to inflate

But what was the use of that historical tour of the stablcoins? Well to show How have they gone from being a technical solution to a narrative that attracts new investors. And the sample of this is the exit to the Circle bag, that is, a catalyst for this new speculative fever in the market. For Hayes, “the next wave of quotes will be the Imitators of Circle” and, therefore, considers:

“In relative terms, these actions will be even more overvalued in the price/AUC ratio (assets in custody in Spanish) than Circle. In absolute terms, they will never eclip using their distribution channels.

Arthur Hayes, Bitmex co -founder and financial analyst.

What happens is that the new Stablecoins emitters face a hard barrier to overcome, since USDT and USDC are already integrated into the main exchange platforms, which favor their circulation. Likewise, social media giants such as goal or X (formerly Twitter) and traditional banks such as JP Morgan will develop their own stablecoins internally, closing the doors to third parties.

This structural domain leaves little space for competitors, condemning imitators to an almost certain failure, according to the entrepreneur.

All this occurs while the United States Congress debates the sanction of the National Innovation Orientation and Establishment Law for Stablecoins, known as Genius. It is a regulation that It seeks to regulate the issuance of stable currencies in that country and integrate them into the financial system. The project was approved by the Senate and must now be treated in the House of Representatives.

In this regard, Hayes says: “The magnitude of the scam depends completely on the regulation of the stablecoins promulgated in the United States. The more freedom the emitters are allowed as to what a stablecoin supports and if they can pay yields to their holders, the greater the financial engineering and the leverage they can use to mask a scam. If a regulatory regime is assumed. Demanding or void, the case of Terra/Luna could be repeated, in which an issuer will create a fleeting algorithmic Ponzi scheme for Stablecoins.

Specifically, Hayes states that if regulations in the United States on Stablecoins are too lax or directly non -existent, emitters will have room for risky or deceptive financial practices. For example, they could create little solid support systems or use leverage (indebtedness) to offer high artificial yields, thus attracting investors with little sustainable promisesas happened with UST, the Terraform Labs stable.

As Cryptonoticia reported, the stable currency of Terraform Labs, which promised to revolutionize the sector, collapsed when losing its parity with the dollar, affecting thousands of investors. Undoubtedly, it was one of the most traumatic financial events in recent years he left Higher losses to 40,000 million dollars.

It should be remembered that UST offered an annual percentage yield (APY) greater than 20 % through Anchor Protocol, an algorithmic system designed to maintain its stability.

By way of conclusion, Hayes believes that once investors discover that these new stablcoins lack mass adoption, their shares will leave millionaire losses. Therefore, his advice is: “negotiate this shit as if it were a hot dad.”

In other words, current euphoria would be an opportunity to make profits in companies’ actions, but investors must be on alert to get out before the stablecoins bubble explodes.