Bit Digital did not used to be on the list of Bitcoin’s favorite miners.

Now, they will get profits with the appreciation of ETH and Ethereum Staking.

Bit Digital (BTBT), a Bitcoin mining company that lies in Nasdaq, is carrying out a strategic change that marks a new stage in its history.

As Cryptonoticias has reported on June 25, the firm announced the start of a transition To form a treasury in Ether (ETH), the native asset of the Ethereum Network. He also reported that he will close his Bitcoin mining operations.

For Mandela Amoussou, financial market analyst, the strategic change is A successful decision Because “BTBT had not been on the list of Bitcoin favorite miners in recent years for a concrete reason: they depended largely on third -party accommodation partners.”

He also says: “His aggressive outsourcing was creating operating problems almost every two quarters. This dependence on third -party infrastructure seemed efficient at first sight and offered a light growth model of assets (or that seemed), but in reality it meant vulnerability to the risks of counterpart and external interruptions. This vulnerability has been maintained in the documented history of the digital bit operations Forced, housing partners and even infrastructure fires that left a significant offline capacity. ”

This shows that one of the greatest structural challenges facing BIT Digital is the lack of control over its own infrastructure. What in theory seemed an agile and economical model, he presented to the company to a series of external incidents that committed their operations.

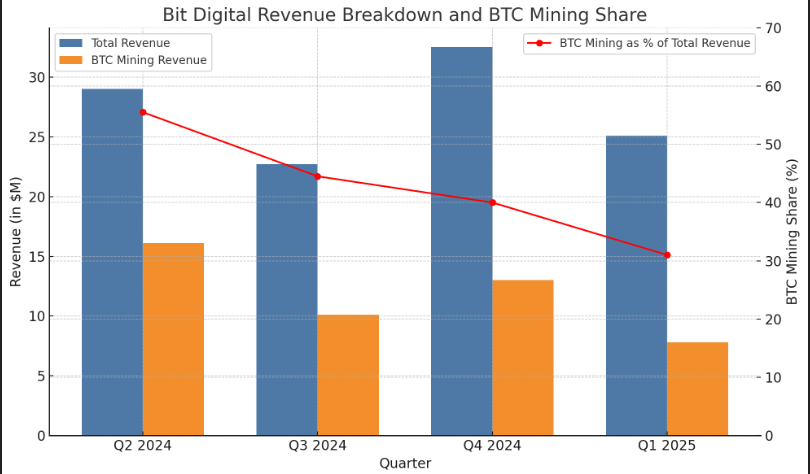

The strategic change of BIT Digital is not limited to abandoning Bitcoin mining, which in the first quarter of 2025 It represented only 31% of total income, compared to 55% in the second quarter of 2024. The following graph shows the breakdown of digital BIT income (blue bars) and the participation of Bitcoin mining (yellow bars) along four quarters, from the second quarter of 2024 (Q2 2024) to the first quarter of 2025 (Q1 2025).

The company is diversifying its business model towards three key areas. First, ETH is accumulating as an asset of corporate treasury, Through the issuance of business debt (A strategy similar to that used by Strategy to finance your Bitcoin (BTC) purchases without depending on your operational income).

However, unlike the firm directed by Michael Saylor, BTBT opts for ETH for its ability to generate passive income through staffing, a mechanism that allows you to obtain yields by participating in the validation of transactions in the Ethereum Network. “The ETH Staking is, in particular, an interesting business line due to its low cost of income, resulting in a higher gross margin,” says Amoussou.

It is important to note that the company began its accumulation and Staking strategy of ETH since 2022. Currently, BTBT has a portfolio of approximately 27,623 ETH.

Secondly, it is developing high performance computing infrastructure (HPC) under the Whitefiber brand, a booming sector promoted by the demand for applications such as artificial intelligence. Finally, BIT Digital is venturing into data centers accommodation services, a segment that began to grow after the acquisition of ENOVUM in the late 2024. It is a business model that consists of offering space, energy, connectivity and technical support so that other companies can install and operate their own hardware in the digital BIT facilities.

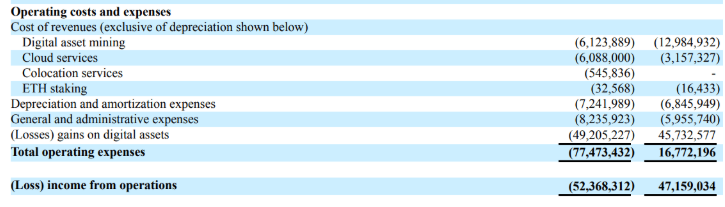

The financial results of the first quarter of 2025, presented in the Digital BIT 10-Q Report before the Bag and Securities Commission (SEC), reflect the initial success of its strategic diversification. In particular, ETH Staking Revenue experienced a 72% growthfrom $ 325,000 in the first quarter of 2024 to $ 561,000 in the same period of 2025, evidencing the potential of this new strategy that BTBT adopted.

On the other hand, cloud services, driven by the GPU infrastructure demand, experienced a growth of 83.92%, with revenues that went from 8.01 million dollars in the first quarter of 2024 to 14.8 million dollars in the first quarter of 2025.

In addition, The services accommodation of data centers generated 1.6 million dollars in the first quarter of 2025compared to zero in the same period of the previous year, showing growth in an area of high potential.

These data confirm that, as Amoussou points out, “Mining is no longer in the center of the digital BIT growth strategy; scalable lines such as Eth Staking, the GPU cloud and the services accommodation of data centers have taken over the income structure.”

To finance this transition, BIT Digital launched an issue of 75 million shares at $ 2 each, raising $ 150 million. These funds will be used mainly to acquire more ETH for corporate treasury, strengthening its digital asset accumulation strategy and expanding Whitefiber infrastructure.

In addition, the company has a program for the sale of shares (ATM) of 500 million dollars, which already raised 48 million after the first quarter. However, this strategy is not exempt from significant risks, as Amoussou says: “Duplicate the purchase of ETH for treasury assets with the planned increase of 150 million dollars is a bold bet and provides a potential generation of performance from the staking, but also creates a risk of concentration with ETH, and BTBT will potentially be more closely linked to the volatility of the ETH price.”

This implies that, if eth prices falls, BIT digital income could be negatively affectedeven if other operational segments have a good performance. In addition, the issuance of new actions introduces a risk of dilution for existing shareholders, since the increase in the number of shares can reduce the value per share.

Anyway, and taking into account the low valuation, with a multiple of 2 times price/sales (Price-to-Sales Ratio, or price-sale ratio). This means that investors pay $ 2 for each dollar of annual income of the company, a competitive figure compared to other companies in the sector.

For Amoussou, this combination makes BTBT an attractive opportunity: “I think it is worth buying [acciones de] BTBT. The company’s turn towards the HPC and ETH treasury is transformational. Investors should not forget the continuous dilution potential and the growing risk of ETH exposure concentration. But at these price levels, the risk/reward seems increasingly attractive. ”