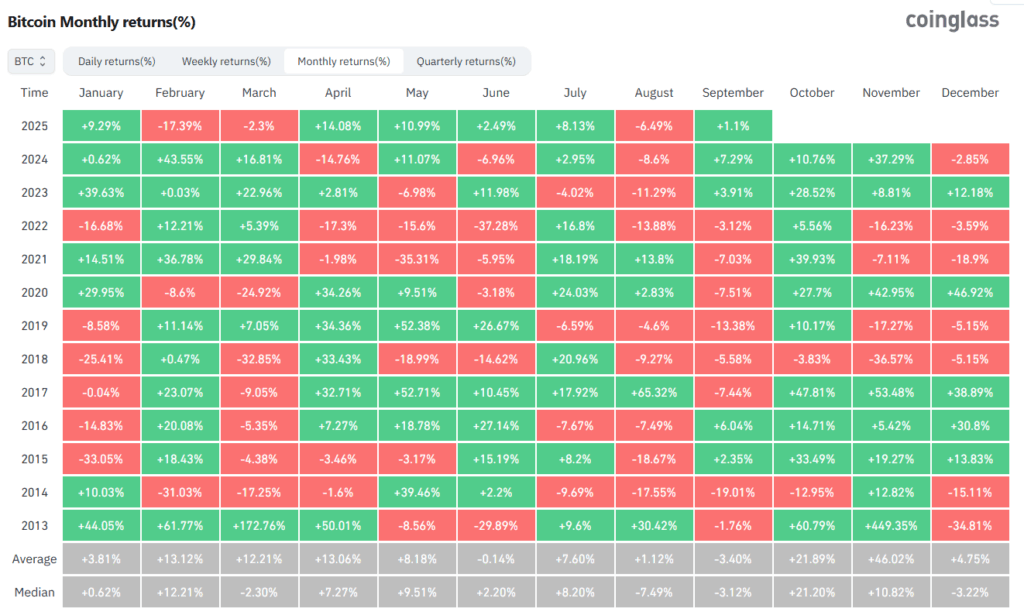

Since 2013, Bitcoin has had 10 positive Octubres and only 2 with negative returns.

If the story is repeated, October could honor its fame of the bullish month, once again.

October appears on the calendar and, with it, the month that usually draws the most smiles in the Bitcoin (BTC) graphics.

Since 2013, statistics are eloquent: 10 Octubres closed green and only two in red (2014 and 2018).

The following table, provided by the Coinglass platform, illustrates this historical behavior of Bitcoin’s price:

This year, the prelude arrives with a September that, despite a last complicated week and episodes of strong volatility, travels with an almost neutral balance – a progress of 1.1% so far this month – and with Growing expectations of a new Federal Reserve Rate (Fed) cuts in October.

The most lax favorable and monetary policy cocktail replaces Bitcoin at the center of all eyes for the start of the fourth quarter.

A CLEAN CLEANING CLOSURE

The final stretch of September was marked by a correction that led Bitcoin to lose the USD 110,000 Already register liquidations for about 1,000 million dollars in derivatives, a classic “shake” of over -up positions that we have already seen in previous cycles.

The following image shows what Bitcoin’s behavior has been during the last 30 days:

At the same time, long-term on-chain movements were observed towards exchanges that, as cryptootics explained it, reinforced the selling pressure and explain part of the setback.

In parallel, the front of the ETF Spot in the United States cut the negative streak of September 24 with net tickets for USD 241 million, headed by the Ishares Bitcoin Trust (Blackrock), and Stablecoins’ offer returned to historical maximums – new record of the total circulating and a particularly relevant USDT flow. In other words: While part of the market takes profits, the liquidity of the ecosystem continues to load.

October: seasonality, rates and liquidity

The seasonal guideline does not guarantee anything, but guides. October has historically been the most upward month for BTC in the last long decade. This year, in addition, it arrives with a macro backdrop that could enhance that inertia: the Fed has already started the cycle of cuts with 25 basic points in September and the markets – including prediction platforms such as Polymarket – point to a second cut in October.

As our cryptopedia explains, lower rates reduce the cost of money, improve risk propensity and usually translate into flows to scarce assets such as Bitcoin.

Below is a screenshot of the Polymarket platform at the time of this publication, in which the high expectation for an interest rate cut in the United States During the month that is about to start:

To that expectation is added a rising systemic liquidity and a weakened dollar: The DXY index accumulates two digits in 2025, a tail wind that, historically, accompanies the rebounds of raw materials, gold and, increasingly frequently, of BTC.

It is no accident that large investment banks, such as Deutsche Bank, stand out the “maturation” of Bitcoin within portfolios and its correlation of performance with gold, while projecting a growing role of digital currency in private reserves – and, eventually, in official balance sheets – towards the end of the decade.

The fourth quarter also arrives with clear signs of the institutional side. In recent days it was known that Morgan Stanley will integrate BTC’s sale on its platform from 2026, reinforcing a trend that is no longer limited to passive exposure products.

In the ETF field, Blackrock recorded in Delaware the “Ishares Bitcoin Premium Inome ETF”, a proposal that would seek to combine spot possession with strategies of Options Overlay To generate performance: evidence that the world’s greatest manager continues to expand its “Bitcoin family.”

And, in the Corporate Front, the fusion of two public contribution BTC accumulators – Strive and Semler Scientific – created a combined 10,906 BTC treasury that reinforces a larger -scale phenomenon: more than 1 million BTC in the hands of companies that are quoted in the stock market and a total value in cryptoactive in corporate hands that already round the USD 100,000 million.

Michael Saylor, a reference for this “Treasury in BTC” thesis, synthesizes the dynamics with a hard fact: ETF, corporations and governments absorb much more offer daily than miners produced from the Halving of 2024. The imper-demand imbalance does not guarantee linear climbs, but it does raise the “floor” of the market when the marketing volatility yields.

Short -term mixed signals, background bias

The market reaches “UPTOBER” with technical indicators and on-chain that, in the very short term, invite prudence. Signatures such as Glassnode have described in September a pattern of “Buy the rumor, sells the news” after the first cut of interest rates.

However, The medium -term picture retains bullish flavor: The gain offer is maintained widely above long -term averages; The standard deviation band suggests that recent setbacks are healthy within a trend that still did not exhaust fuel; And net flows towards regulated products, together with the expansion of the circulating of Stablcoins, tend to positively impact the price once the market digests volatility events.

In communication with cryptootics, Emanuel Juárez, an analyst at HF Markets, commented: «In the short term, the level of 107,221 dollars will be key as support [para bitcoin]. If it is maintained above, the upward trend remains intact, with an immediate objective in the $ 117,875, whose rupture could make way for a new historical maximum ».

The also analyst Juan Rodríguez – conductor of the YouTube channel «Bitcoin y Criptos» -, argues that the recent adjustment “cleaned” the excess of leverage and that the liquidity could reactivate the demand in the fourth quarter.

And statistics, as mentioned from the head of this publication, favors the bullies: October is the month of Bitcoin.

With that frame, The base scenario for the start of the fourth quarter is of bullish bias and growing probability that Bitcoin challenges its historical maximums between October and December.

It is not a promise; It is the result of seasonality, liquidity and institutional adoption converging. The task of the investor, as always, will be to separate signal noise: not pursue candles, monitor supports, and prioritize those metrics – flowers, rates, Stablecoins offer – which, again and again, have explained the great trends of Bitcoin, in addition to keeping in mind the foundations of the digital currency. If the story is repeated, October could honor its fame once again.