The great use of stablecoins shows the interest of Argentines in becoming dollarized.

For now, banks are still prohibited from offering the purchase and sale of cryptocurrencies.

Argentina appears as the central point of the expansion of neobanks in 2026. In a country where the dollar is a refuge from inflation, stablecoins emerge as an alternative for Argentines to maintain purchasing power without depending on the traditional banking system.

Neobanks could take advantage of this opportunity because their digital infrastructure and ability to scale quickly It allows them to offer innovative services that traditional banks cannot (or at least not with the same speed).

Before continuing, let’s define neobanks as 100% digital banking financial entities (regulated by the BCRA in Argentina), without physical branches, that operate through mobile applications or web platforms.

Unlike traditional banks, neobanks were born with their own technological infrastructure based on APIs and flexible systems. This allows them to develop products faster, operate with minimal costs, and scale to new markets in a matter of weeks.

Prominent examples such as Ualá, Brubank and Naranja X already operate in Argentina, concentrating a good part of the growth of digital finance. However, today they cannot offer products linked to stablecoins or cryptocurrencies. Since May 2022, the Central Bank of the Argentine Republic (BCRA) arranged that the entities under its orbit do not participate, directly or indirectly, in the offer of cryptoassets to clients to mitigate risks to users and the financial system.

For now, banks (including neobanks) are prohibited from offering the sale and purchase of cryptocurrencies, so integrating stablecoins in Argentina will require regulatory changes that enable their use within the financial system.

Its advance promises to transform the way Argentines save, invest and relate to the financial system.

Why are neobanks targeting Argentina?

According to a report From Moic Digital, a digital asset marketing agency, in Latin America the use of cryptocurrencies “is not focused on speculation with bitcoin (BTC), NFTs or betting on altcoins.” Furthermore, the report highlights: “The use of stablecoins as savings and payment tools denominated in dollars is highlighted.”

The report also points out that “activity with stablecoins represents between 50% and 90% of crypto transactions in the main markets in the region.” Furthermore, he adds: “Think about it: when someone in Argentina or Venezuela buys cryptocurrencies, they are not buying BTC hoping it will rise, but rather acquiring USDT to protect themselves from the collapse of their local currency.”

It is worth clarifying that the latter, of course, is not entirely accurate, but rather an exaggeration. It is known that both Argentina and Venezuela have a large bitcoiner community, which includes long-term hodlers and also short-term traders or speculators with bitcoin and cryptocurrencies.

But, returning to the report reviewed, stablecoins not only reflect a cultural change, but also a business opportunity. In fact, Moic Digital suggests that Neobanks could capitalize on this interest by incorporating services based on digital currencies.

In other words, Moic’s thesis is that neobanks should enter that segmentoffering savings, payments and investment in digital dollars within a regulated and accessible environment for the common user.

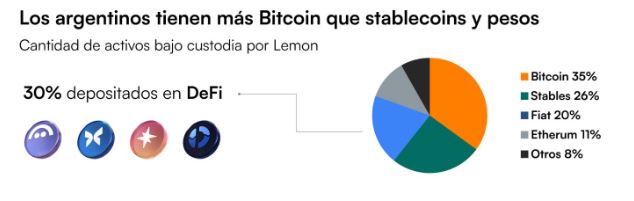

How does this look in Argentina? To read the phenomenon it is convenient to separate possession from use. According to data from Lemon (a bitcoin and cryptocurrency exchange), The portfolio composition of local users shows more bitcoin (33%) than stablecoins (26%) and pesos.

However, when the operations are observed, stablecoins gain relevance due to their savings and payment function in digital dollars. That is to say, although the users of that exchange have more BTC in their walletseveryday use is increasingly concentrated on stablecoins.

Lemon’s spokesperson explained to CriptoNoticias that “in 2024, the panorama changed: inflation decreased, the dollar stabilized against the peso (exchange stability) and BTC reached historical highs.”

“One might think that with calm, stablecoins would lose relevance. But the opposite happened. Even with the opening of the exchange market in 2025, when the stocks were eliminated and the purchase of dollars in banks was enabled, the volume operated in stablecoins within Lemon grew by more than 20% compared to the previous semester,” they detailed.

That is, stablecoins They are no longer just a haven of value or protection against inflationbut a functional infrastructure on which payments, loans, remittances and global financial products are built, as seen in the following graph:

In short, according to Moic Digital’s observations, neobanks are already targeting Argentina and other Latin American countries because the region meets the conditions that turn this thesis into a concrete opportunity: a de facto dollarized economy, a financially active population in the digital environment, but outside the traditional banking system; and an ecosystem of digital assets that already operates as a parallel financial system.

If they promote and obtain clear rules for operating with BTC and stablecoins, neobanks will be in a position to further unite the traditional financial system with the digital infrastructure that moves the region.