The entity was born to prevent crises, but its mistakes have been very costly.

After a history of concentrated power failures, bitcoin changed everything.

Few institutions have sparked such intense debate as the United States Federal Reserve (FED). Born in 1913 under the premise of providing stability and avoiding banking crises, the entity has become a central actor in the modern financial system. More than a century later, its legacy invites us to wonder if it truly fulfilled its mission of bringing order or if, on the contrary, it has contributed to multiple imbalances that persist today.

Far from arising by chance, the creation of the FED was orchestrated by powerful financial interests, an argument supported by accredited specialists and academics.

Following this vision, Murray Rothbard, one of the main references of the Austrian School of Economics in the 20th century, maintains that The creation of the FED was the result of years of discreet negotiations and agreements between politicians and powerful banking groups.

In his work The Case Against the Fed (1994), Rothbard explains that figures like JP Morgan, the Rockefellers and Kuhn, Loeb—backed by like-minded economists—designed an institution that, ostensibly, sought to promote the public good. But it indicates that in practice gave a handful of private banks the privilege of creating money out of thin airinitially with a certain link to gold, although this connection would weaken until it disappeared.

The author’s criticism does not stop at the mere denunciation of the founding process. His central concern was that by giving a small group of bankers and bureaucrats the legal monopoly of issuing money without metallic backing, the door was opened to practically unlimited monetary expansion. Since 2009, this abuse of power has also been roundly questioned with the emergence of bitcoin (BTC).

Origins and criticisms of the Federal Reserve

After the breaking of the last link with the classical gold standard, first in 1933 at the domestic level and then, definitively, in 1971 at the international level, The FED obtained a margin of discretion unprecedented in monetary history.

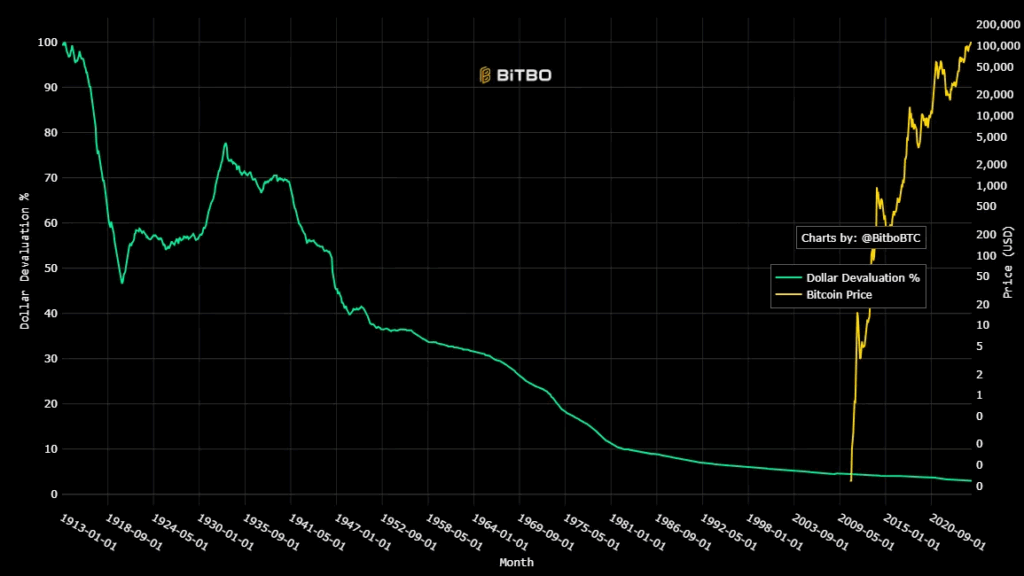

The impact of this freedom can be evaluated with almost surgical coldness through a single variable: the loss of purchasing power of the currencies that for two centuries functioned as a global reference.

This example is analyzed by Diego Giacomini, in his book “The Revolution of Freedom” (page 244), who points out that, between 1913 and 2020, fiat money in the United States and Great Britain destroyed much of the purchasing power of their currencies.

Thus, the author relied on historical series of the Consumer Price Index (CPI) of both countries – and on statistical data from the work “Two centuries of Argentine Economy” (1810-2018) -, which followed the same monetary path in very close moments.

On December 23, 1913, the US Federal Reserve was founded, taking the United States and Great Britain as examples, which makes sense, since both were the hegemonic empires of the last two hundred years. Between 1913 and 2020, their retail price indices rose more than 9,277% in Great Britain and more than 2,770% in the US. That is, in these last 107 years, fiat money destroyed a good part of the purchasing power of both currencies, causing an unprecedented inflationary process (…) On the contrary, between 1810 and 1913, under a gold standard and without fiat money, and in a context in which bureaucrats could not manage the amount of money with complete discretion as is the case today, a healthy deflation occurred: -31.9% in Great Britain and -19.6% in the USA.

Diego Giacomini, economist.

Highlighting this last argument is very necessary because, from the perspective of the Austrian School, The FED is the machine that made the unlimited expansion of money possible.

To illustrate this phenomenon, one need only look at the M2 money supply—a broad measure of money in circulation that includes deposits and savings. In January 1959, the first official data point of the M2 series registered 286.3 billion dollars (USD). Today, in October 2025, it exceeds USD 22.2 trillion, a multiplier of almost 78 times that reflects the discretionary abuse of issuance under the control of the FED.

Such an increase has visible effects on public finances. In recent periods, total US public debt has skyrocketed, rising from $23.2 trillion at the end of 2019 to $38.1 trillion in November 2025, a 64% increase in just six years.

Furthermore, the institution’s history includes episodes of acute catastrophe, in which its intervention not only failed to prevent crises, but even aggravated them.

When management worsens the collapse

The most famous—and devastating—case of this trajectory is the Great Depression of 1929-1933.the deepest economic collapse the United States has ever recorded. From Rothbard’s perspective, the problem is structural: the FED’s design gives a small group of bankers and bureaucrats power that allows unlimited monetary expansion, creating systemic vulnerabilities.

For his part, Milton Friedman, liberal economist and Nobel Prize winner in Economics, criticism concrete decisions during depression. When Britain abandoned the gold standard in October 1931, the FED responded by abruptly raising the interest rate from 1.5% to 3.5% in just two weeks. This measure reduced liquidity rather than increasing it at the time, accelerating a wave of bank failures and deepening the depression.

In this way, structural and tactical criticisms complement each other: while Rothbard warns about the risks inherent to the system, Friedman shows how specific mismanagement can amplify the effects of these weaknesses. The central point is that monetary systems with concentrated power are likely to amplify errors.

The Federal Reserve System was established in 1914 with the goal of preventing crises like the depression, and yet its existence ended up being responsible for the depression being so severe. You cannot look to the future without considering what happened before. Terrible mistakes were made that led to the depression, and the government’s immediate actions to help those most affected were desperate, reactive and unplanned… They were supposed to provide liquidity and instead they reduced liquidity. The amount of money in the United States fell by a third between 1929 and 1933.

Milton Friedman, economist who won the Nobel Prize in Economics in 1976.

Almost a century after the Great Depression, the crisis of 2008-2009 produced, in the long run, a similar structural result: more debt, more inflation and greater concentration of power. For a hundred years, critics of the FED, from the most radical Austrians to moderate monetarists, pointed out these problems with surgical precision, but no one managed to offer a practical solution that did not depend on convincing those who caused so much damage.

That changed forever in January 2009 when the Bitcoin genesis block was mined. Thus a proposal began to take shape that, as CriptoNoticias reported in a note on the impact of inflation, has the capacity to give people back control over their saving capacity.

The rise of bitcoin

After decades of discretionary monetary expansion and chronic inflation, BTC emerged as an alternative that few expected. Satoshi Nakamoto’s whitepaper presented a digital monetary system peer-to-peer (P2P), capable of operating without intermediaries or central authorities.

That was, in effect, a declaration of war against the very system that Rothbard and Friedman had criticized so harshly from their respective approaches. Bitcoin, like any invention arising from human action, has found a way to flourish even within coercive systems, sowing the conviction that it is possible to do things differently and demonstrating, over time, that people are not condemned to any regime.

The design of BTC directly confronts the two major problems that the Austrian School attributes to the FED: it eliminates the monopoly on the issuance of money and imposes fixed mathematical rules that no bureaucrat can modify. Its supply is limited to 21 million coins.

Today, more than fifteen years after its birth, Satoshi’s project has ceased to be a niche curiosity to become the best-performing asset of the last decade and a half. Its resilience, unknown for any fiat currency, has attracted institutional investors and even sovereign funds and the possible new president of the FED.

Will bitcoin be the blow that puts an end to fiat money? Only time will tell. Meanwhile, in a world where central banks print trillions to bail out their allies and socialize losses, those who save within this system experience firsthand the effect of inflation, a silent and brutal wealth transfer machine. BTC, on the other hand, shows us that it is possible to organize money in a completely different way.

Although the inflationary process is often disguised with euphemisms and cushioned by subsidies, in emerging economies it hits much harder than in developed countries: families who are unable to cover the basics for their children and retirees who see their pensions devalued month by month. The root of this suffering goes back to the unlimited discretion that central banks gradually began to assume since 1913.

Faced with this crossroads, each person who decides to save in BTC instead of pesos, bolivars, liras or even dollars that depreciate, issues an irrevocable vote of no confidence towards the concentrated powers. The same occurs with governments that, as in El Salvador or Bhutan, have strategically understood the weaknesses of the global monetary system and have opted for the asset, even implementing educational programs to promote its adoption.

Disclaimer: The views and opinions expressed in this article belong to its author and do not necessarily reflect those of CriptoNoticias. The author’s opinion is for informational purposes and under no circumstances constitutes an investment recommendation or financial advice.