The non-custodial model secures funds in smart contracts, eliminating third-party risks.

Identification (KYC) allows Firefish to provide services in a greater number of jurisdictions

The bitcoin (BTC)-backed lending market continues to mature, moving away from pure speculation to offering robust financial tools to long-term holders.

In a recent interview with CriptoNoticias, Pablo Contreras Villarreal, member of the Firefish team—a lending platform Peer-to-Peer (P2P)—, offered his perspective on the evolution of this sector and why he believes that the technology created by Satoshi Nakamoteither has become the most solid financial guarantee tool today.

As with many bitcoin adopters, Contreras’ path was not linear. His first contact occurred in 2018, but initial skepticism and market volatility kept him on the sidelines. “They introduced it to me in 2018 and I, like many people, walked past me and said: ‘No, I don’t have money now,’ ‘No, it’s very expensive,'” Contreras said.

However, the macroeconomic context of 2025, added to a restructuring of his personal life, led him to reconsider his position. “This is the time to get into bitcoin,” he told himself, deciding to deepen his knowledge through the diploma organized by the NGO Bitcoin Argentina.

This academic training allowed him not only to understand the technical foundations of the protocol, but also to professionally integrate into the ecosystem through Firefish, a firm of Czech origin that sought to expand its market presence in Argentina.

Peer-to-peer and non-custodial lending

The business model that Contreras describes moves away from traditional banking and centralized cryptocurrency platforms that suffered collapses in previous cycles. Firefish operates under a logic Peer-to-Peer (peer to peer) and non-custodial (without custody).

As the interviewee explained, the platform acts as a meeting point between natural persons: those who need liquidity and have bitcoin to offer as collateral, and those who have capital (in fiat currencies or stablecoins like USDC) and are looking for a return.

The key to security is that the company does not touch the funds. «Firefish does not take that bitcoin and negotiate it, but it remains in a contract, in a smart contract which is in the Bitcoin blockchain,” Contreras explained. This guarantees that “there is no one to speculate” with users’ assets, mitigating the counterparty risk that has affected other entities in the sector.

Bitcoin as “perfect collateral” for loans

One of the central points of the conversation revolved around the suitability of bitcoin as a backup asset. Contreras made reference to the “perfect collateral” thesis, a concept that the platform actively promotes.

When asked whether bitcoin is superior to traditional collateral such as gold or real estate, his response was forceful, based on the liquidity demonstrated during the current year.

«Everyone knows that in 2025 many, many thousands of bitcoins have been released onto the market that at another time would have dropped, would have destroyed the price. The enormous liquidity and sale, that is, the interest in being purchased that bitcoin has, is being demonstrated,” he analyzed.

For the interviewee, the intrinsic characteristics of the digital asset —its 24/7 trade, its divisibility, its scarcity and its global market— They elevate it above other options. “It has become, today, a pristine and perfect collateral to, basically, support any type of operation,” he stated. For this reason, the platform maintains a strict policy: “Bitcoin only. It is a platform by bitcoiners for bitcoiners.

The debate over privacy and KYC

A sensitive topic in the bitcoiner community is user identification or, in English, Know Your Customer (KYC). Being a regulated platform in Europe, Firefish requires identification, sparking a debate about privacy versus economic benefits.

Contreras addressed this point pragmatically, noting that Regulatory compliance translates into direct benefits for the user’s pocket. “Anonymity is still expensive in this bitcoin world,” he said, explaining that platforms that do not require identification tend to have higher costs due to the risk involved.

«I believe that the future is a future at least mixed between your bitcoin or your world Non-KYC and the world that is gradually adopting it,” he said in a personal capacity. For him, mass adoption implies some integration with the traditional financial system: “If we want bitcoin to be adopted, we cannot expect total anonymity forever.”

Firefish Expansion and Risk Management

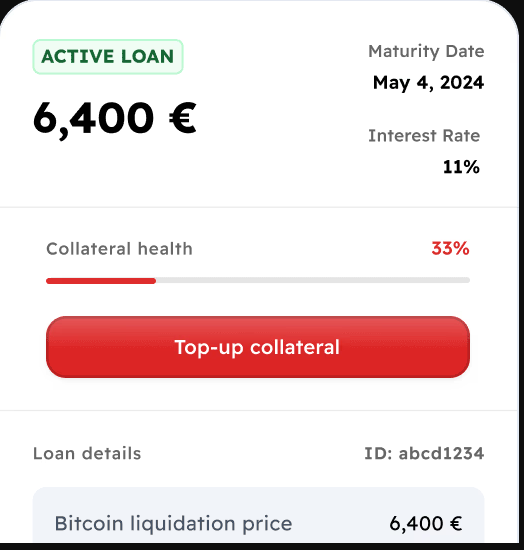

Regarding the financial health of the loans, the system is based on overcollateralization. The interviewee explained that alerts are issued (margin calls) if the value of bitcoin drops dangerously, urging the user to deposit more collateral. “Those bad collateralizations that produce liquidations are not in Firefish’s interest at all,” he said, highlighting that in almost three years of operation they have not carried out forced liquidations.

The company’s revenue model is transparent: a 1.5% annual fee on loans. Looking ahead, the strategy of the company co-founded by Igor Neumann appears to focus on strategic alliances. “They are studying partnerships. “They are studying partnerships to be able to expand around the world,” Contreras said, suggesting that organic growth through local partners is more viable than opening physical offices in each jurisdiction.

The vision presented by Contreras reflects a maturation in the use of digital assets: tools that take advantage of the transparency of Bitcoin to offer efficient financial services, prioritizing technical security and the solvency of collateral over short-term speculation.