Fintechs have granted credit to borrowers who are not necessarily creditworthy.

When financial crises arrive, the percentage of credit defaults increases.

Chris Irons—an independent financial analyst who writes under the pseudonym “Quoth the Raven” and is founder of the ‘Fringe Finance’ newsletter—has been documenting the fragilities of the US and global financial system for years.

Irons builds his analyzes on a sustained distrust of business models that thrive on cheap money and collapse when rates become real again.

In a recent delivery from your newsletter, dated March 19, The financial writer focuses on private credit and the “buy now, pay later” segment —systems that allow you to finance purchases in installments without going through a traditional credit card, and which in Latin America are known through services similar to Mercado Pago Cuotas or Kueski Pay—, two areas that, according to him, are showing the first cracks of a credit cycle that has already changed direction.

“Free money” had an expiration date

Irons’ starting point is not a new diagnosis, but rather a confirmation of something he had been pointing out. “I have warned for years that the ‘buy now, pay later’ industry is built on fairly fragile foundations,” he writes.

AND The underlying problem, according to Irons, is the credit quality of the borrowers. The model consists of granting instant credit with minimal risk analysis to consumers who finance small purchases.

Irons says it without euphemisms: “Companies whose main innovation is allowing consumers to split a $40 online purchase into four payments are probably not lending money to the wealthiest segment of the population.”

Furthermore, the analyst maintains that the model practically guarantees the opposite. When the purchase of fast food or snacks is financed in installments, the profile of the borrower is not exactly low risk. These are consumers who do not have the liquidity to cover these expenses in cash or who have already exhausted the most conventional means of credit.

The witness case that Irons analyzes is that of the Stone Ridge Alternative Lending Risk Premium Fund (LENDX), a private credit fund managed by Stone Ridge Asset Management that purchases loans and securities linked to fintech originators: Affirm, LendingClub, Upstart, Block and Stripe, among others.

The problem arose when investors wanted to exit: “Stone Ridge informed its clients that it would only be able to accommodate about 11% of refund requests.” The fund operates under a structure that limits withdrawals to periodic windows and forces the manager to repurchase only a percentage of the shares per quarter. The mechanism works as long as investors do not panic. When they do, the illiquidity of the underlying loans becomes an unsolvable problem without incurring significant discounts.

It’s not just an American problem

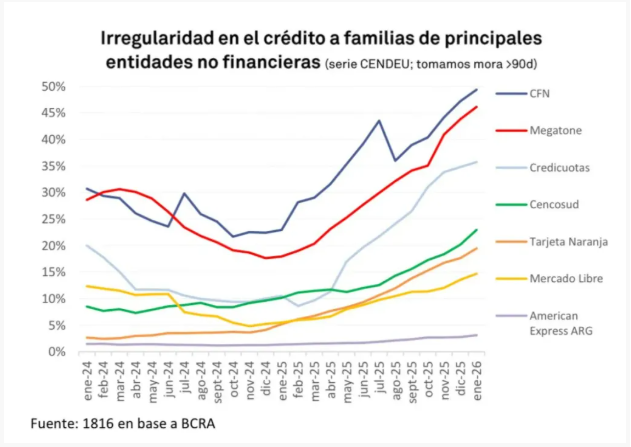

Irons does not say it in his text, but outside the United States, they are beginning to be seen similar problems. For example, according to the Public Opinion Monitor (MOP) of the consulting firm Zentrix, 6 out of every 10 Argentine households took out debt for daily expenses in the last six months. And, the insolvency of many of these borrowers is already beginning to claim its first corporate victims. This is the case of the fintech UALÁ, which faces defaults for more than 40% of the loans granted.

In others fintechs in Argentina see similar situations:

Traditional banks shunned these borrowers for decades for a precise technical reason: “When economic conditions tighten, default rates tend to rise rapidly among weaker borrowers.”

The fintech thesis—access to credit as financial democratization—did not eliminate this structural dynamic; he simply postponed it while the capital markets were willing to finance the experiment. And the experiment lasted as long as cheap money lasted.

Many assets would be overvalued due to cheap money

This table is connected to an analysis published on March 20 in CriptoNoticias, which included the warning from financial writer Charles Hugh Smith about the same underlying dynamic: Private credit inflated the prices of many assets for years because it ended up in existing assets—stocks, real estate, businesses already built—instead of productive investment.

Irons reaches a similar conclusion from another angle: “The combination of stress on BNPL loans and increasing repayment pressure on private credit funds seems like an early reminder that the credit cycle has changed.”

Where does Irons aim for the future? To two specific sectors. The first is commercial real estate, where “property valuations still look suspiciously optimistic given the current financial environment.”

The second is the set of companies that are still listed as if the low rate regime were to return: Blue Owl Capital, Ares Management, the BDCs—business development funds that in the United States channel capital to unlisted medium-sized companies—and certain regional banks with relevant exposure to private credit and BNPL. “Personally,” Irons writes, “I still think most of that market is best avoided.”

And now who can help us?

The exit, according to the analyst, will eventually go through the Federal Reserve (FED). The manual is already written: when the credit market begins to fail, the FED designs a liquidity mechanism.

But that intervention historically comes after a period of forced deleveraging, not before.

If this process has begun in fintech loans and private credit, there may still be an uncomfortable phase ahead in which investors rediscover the real value of their assets. And that’s usually the part that no one enjoys.

Chris Irons, financial analyst.

Does Bitcoin strengthen in such a scenario?

Iñaki Apezteguía, guest author of CriptoNoticias, believes that bitcoin (BTC) and some cryptocurrencies could benefit from a scenario like the one presented here.

In an analysis published by this information portal on March 13, 2026, Apezteguía pointed out that private credit chaos could act as a catalyst for two alternatives that are already taking shape.

The first is bitcoin: Unlike private credit funds, bitcoin “offers 24/7 global liquidity,” “its price is set by the real market every second, reflecting reality instantly,” and “it has no middlemen that can ‘close the door’ or contracts that trap you in obsolete sectors when the market gets nervous.”

The second would be tokenized real world assets (RWA).: Projects that tokenize private credit such as Ondo, Centrifuge, Maple, Goldfinch or Figure offer, according to Apezteguía, exactly what traditional structures cannot provide today, which is total transparency and real-time valuation auditable on the network.

“We are not facing the end of private credit, but rather its definitive transformation,” writes Apezteguía. “Smart money is migrating from opaque, locked-in structures toward bitcoin and cryptocurrency infrastructure, which solves trust issues that Wall Street can no longer hide.”