In the short term, macroeconomic factors are influencing more than bitcoiner narratives.

In the long term, the scarcity of bitcoin continues to give it great appreciation potential.

Mathematical models that for years explained the price of bitcoin stopped working. That is the central premise of the analysis published on March 27, 2026 by Tommaso Scarpellini, investment specialist.

The main thesis that Scarpellini presents in his Financial Serenity newsletter may be uncomfortable for many: scarcity—the bullish argument par excellence—is not governing the price of bitcoin.

Scarpellini identifies two models that historically dominated the bitcoin valuation narrative and that today, according to him, “are failing miserably.”

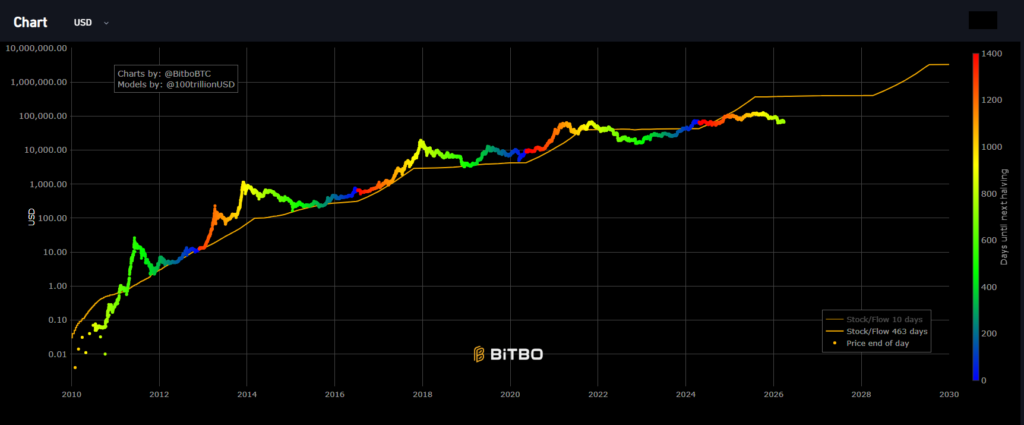

The first is the stock-to-flow (S/F)which measures the value of an asset in relation to its relative scarcity.

By that metric, bitcoin has an S/F of 113, more than double that of gold, whose ratio is 60. Logic would indicate that bitcoin should be more valuable than the metal.

However, the analyst points out that the model “until 2022 described the trend of bitcoin well, but that today it is failing,” and observes that “it is less and less talked about” within the community.

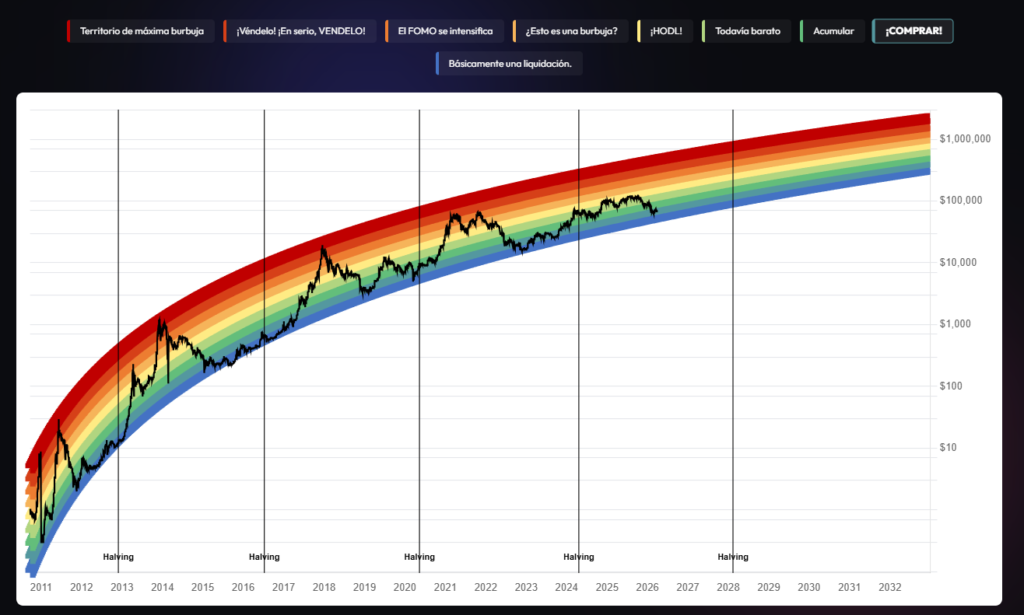

The second model in question is the Halving Price Regression (HPR), popularly known as the “rainbow chart”.

This is a non-linear regression built on bitcoin prices on the dates of each halving. The HPR projects that each halving cycle should raise the price in a predictable trajectory. But according to Scarpellini, “the model has failed to describe the evolution of the market, and the cycle remains anchored at the bottom of the rainbow.”

These alleged flaws in the model have meant that Blockchain Center, the organization that created this graph, has had to make several modifications to it over time to adjust it to the price of bitcoin.

In any case, it is necessary to clarify that The “rainbow graph” has no pretense of seriousness. As CriptoNoticias has explained, the creator of this model himself, Holger Rohm, points out that it is nothing more than a meme or a joke that he invented to raise the morale of bitcoiners.

Additionally, it is worth clarifying: The fact that a model has not correctly predicted a specific cycle does not equate to its definitive invalidation. It can be argued that the relevant S/F evaluation horizon, for example, is decades, not months.

Scarpellini’s criticism, however, is not technical but structural: The problem would not be the calibration of the models, but rather their base assumptions.

Bitcoin as a high beta asset

If scarcity is not driving the price of bitcoin, what is driving its price movements? For the analyst, the answer lies in the bitcoin’s growing correlation with US technology indices.

“The correlation has increased to the point of becoming, in my opinion, a kind of high-volatility asset of the S&P 500 and the Nasdaq 100,” he writes. In practice, this means that bitcoin amplifies stock market movements: it rises more when the Nasdaq rises, and falls more when it falls.

The underlying reason, according to Scarpellini, is that «The price of bitcoin only follows its demand. And demand, in turn, does not depend on scarcity. It’s probably never been like this.”.

This point is, perhaps, the most provocative of the text. If demand for bitcoin was never really linked to scarcity—but rather to speculative appetite, global liquidity, and institutional flows—then the narrative architecture that many bitcoiners rely on would be built on a weak foundation.

The weight of the war with Iran

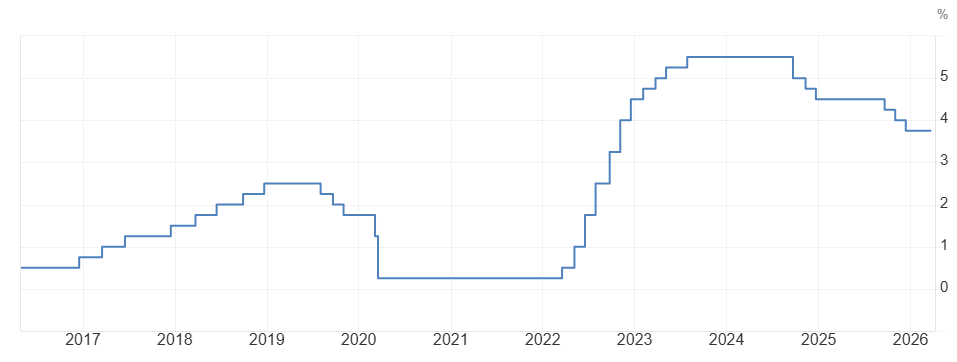

Here the analysis becomes immediately relevant. Scarpellini directly connects the geopolitical situation to bitcoin’s performance: the conflict in Iran raised one-year breakeven inflation—a metric that reflects what the bond market expects inflation to be over the next twelve months—to around 5%. That pushes up expectations about short-term interest rates, which in turn contracts the liquidity available for assets considered “risky.”

“If the short-term cost of money increases, the liquidity that the Federal Reserve injects into the system and Trump’s fiscal stimulus will have a less significant impact on the concept of bitcoin scarcity,” the analyst argues. And he discards the comparison with gold: the metal benefited from massive purchases by central banks, a government flow that bitcoin does not yet enjoy. “Therefore, bitcoin naturally follows a dynamic much closer to that of the money market,” he concludes.

In the long term, things change

However, despite what many might think after reading this far, the analyst does not conclude with a bearish recommendation.

His long-term bullish argument rests on three pillars: that the market considers the inflationary impact of the energy conflict to be transitory, that the scarcity of bitcoin is real (more than 21 million bitcoins will never exist) even though it is not being “monetized” in the current cycle, and that institutional flows—ETFs, corporate strategies—will continue to expand.

“In the long term, an interesting gap in valuations could emerge,” he writes. His final rating for the BTC/USD pair is “hold,” with the caveat that those who buy at these levels must have enough horizon to absorb what the market estimates as an adjustment cycle of up to five years.

Scarpellini’s reading is, in short, that of someone who does not believe in bitcoin out of conviction — “for me, bitcoin has no use,” he declares bluntly — but does believe in the structure of the industry that supports it. A distinction that, in the eternal debate between maximalists and skeptics, places their analysis on uncomfortable ground for both sides.