In the past, Trump has made decisions with bond yields in mind.

According to analysts, Trump would seek to accelerate an agreement with Iran or have the FED cut rates.

The US bond market is under pressure not seen since the 2025 tariff war, and several analysts believe that Donald Trump’s government will soon intervene.

This week, more precisely on March 26, 2026, Adam Kobeissi, founder and editor-in-chief of The Kobeissi Letter newsletter, published on X a warning direct: “The bond market is by far the biggest problem for the United States right now, much bigger than the energy price situation.”

To understand why this matters, we must go back to February 28, 2026, when the United States and Israel began attacks against Iran in a war that is now one month old.

In the early days, The market’s attention was focused on the rise in the price of oilas CriptoNoticias was reporting. But that would no longer be the main concern.

From oil to bonds

According to The Kobeissi Letter, the real problem moved: “the biggest problem now is the bond market, and what is quickly becoming the main obstacle for the global economy.”

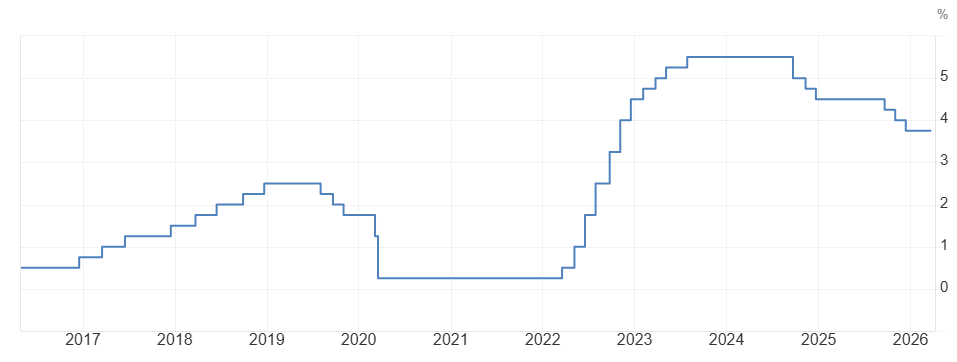

Specifically, the yield on the 10-year US Treasury bond – a key indicator of the cost of money throughout the global economy – rose from 3.92% to 4.42% since the start of the war. That’s 50 basis points in less than a month.

To put it in perspective: By the end of 2025, the market expected the Fed’s benchmark rate to fall to the 2.75%-3.00% range during 2026. Today, according to rate futures cited by Kobeissi, the base case shows rates unchanged through September 2027. Worse still: “rate hikes were back in discussion, with a ~43% chance that the Fed will raise rates before end of 2026. »

That rate increases are being discussed again —when a few months ago it was being discussed how many cuts there would be— It is a dramatic reversal of expectations.

Inflation and employment: the Fed’s double problem

The Federal Reserve has two terms: maintain price stability and maximum employment. The problem is that today both objectives are in conflict.

Kobeissi details that, according to his data, 12-month inflation expectations jumped to 5.2%, the highest level since March 2023driven in part by the rise in oil prices derived from the conflict with Iran.

Furthermore, analysts at the financial bulletin estimate that if crude oil averages $95 per barrel for three months, the consumer price index (CPI) could climb up to 3.2% year-on-year and possibly more, considering the secondary effects of the war on the supply chain. It is worth clarifying that, at the time of this publication, on March 28, 2026, the price of a barrel of Brent is $106.

Added to all this is the fact that the labor market in the United States deteriorates. Nonfarm payrolls were revised downward by 1,029,000 jobs through 2025, the largest correction in at least 20 years. The average duration of unemployment jumped to 25.7 weeks in February, a four-year high. “The US economy cannot withstand the 10-year bond yield approaching 4.50%, much less 5.00% or more,” the analysts warned.

The “Trump threshold” and intervention

There is a recent precedent that The Kobeissi Letter analysts consider key. In April 2025, during the tariff crisis known as “Liberation Day”, Trump paused the tariffs for 90 days just as 10-year bond yields hit the 4.50%-4.70% zone.

The day after the announcement, Trump himself declared live that he was “watching the bond market”. Since then, that range functions as what the report reviewed here calls the “Trump policy change zone”: the level at which the Government feels enough pressure to change course.

Today bond yields are at 4.42%. The distance is minimal. That’s why analysts interpreted the March 23 announcement — when Trump postponed attacks on Iranian power plants and spoke of “productive” talks — as the first sign of intervention.

What will happen to bitcoin?

While The Kobeissi Letter does not reference bitcoin in its analysis, we can draw some speculative conclusions. The answer to the question in this intertitle is not linear: it depends on the type of intervention that occurs.

If the intervention is a peace agreement with Iranbond yields would fall, expected inflation would moderate, and appetite for assets considered “risky” would return. In that scenario, bitcoin will probably go up along with technology stocks: it is the most bullish case in the short term.

If the intervention is to get the FED to cut interest rates, history favors bitcoin. Low rates imply cheaper dollars and greater search for yield in alternative assets. But there is a deeper reading: if the Fed cuts with inflation at 5%, the implicit message is that it is willing to tolerate that inflation. And that is precisely the strongest argument for bitcoin as a store of value against the degradation of fiat money.

Instead, If the intervention fails or is delayed, the scenario becomes complicated. Rising yields imply tighter financial conditions: investors sell risky assets to cover losses on other positions. In that case, the price of bitcoin would suffer a greater drop.

For all this, the market must remain attentive to each new event related to the war in Iran. Any statement from Trump or any of the actors involved in the conflict can cause a change in economic course and have an impact on bitcoin and other financial assets.