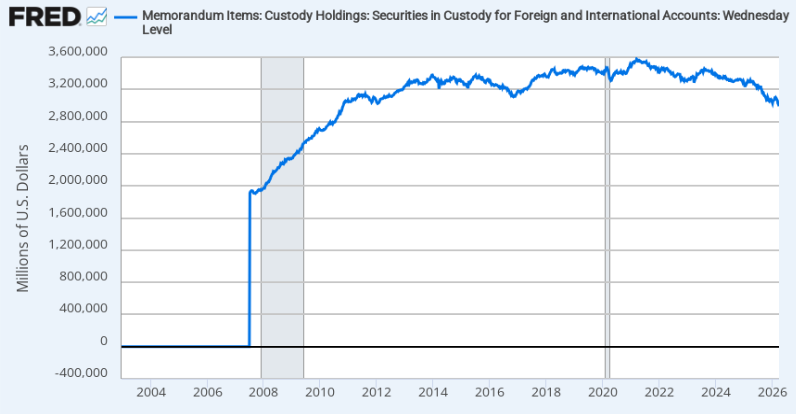

Holdings fell to about $2.7 trillion.

Brazil held holdings of $168 billion in January 2026 after net sales.

In recent weeks, the United States sovereign debt market has recorded a capital movement that has not been seen for more than a decade. As the conflict in Iran keeps energy supply routes under pressure, foreign central banks reduce their holdings of Treasury bonds held at the New York Federal Reserve (FED) to the lowest level since 2012.

Official data from the FED (WSEFINTL1 series) confirm a net outflow of $82 billion since the end of February, leaving the total balance at 2.7 billion. Although these figures are conclusive, analysts debate whether we are facing a short-term tactical response or the beginning of a structural change in the global financial architecture.

The most direct explanation lies in the energy bill. When the price of oil escalates, net importing countries, such as India or Türkiye, face double pressure. This is because they need liquid dollars to pay for crude oil and, at the same time, they must intervene in their markets to prevent their local currencies from depreciating.

In this scenario, Treasury bonds act as a reserve of immediate liquidity; Selling them is the fastest way to obtain the necessary dollars to stabilize their domestic economies.

However, this liquidation occurs in a context of high geopolitical sensitivity. Deutsche Bank Analysts warn that, if this low foreign demand continues, long-term bond yields could rise by more than 100 basis points.

This revives the debate on reserve diversification, where some observers see growing interest in alternative assets such as gold or bitcoin (BTC), although total holdings data (public and private) suggest that the dollar remains the lynchpin of the system.

Another report, also from Deutsche Bank cited by CriptoNoticias in October 2025, indicates that bitcoin could be part of the balance sheets of central banks by 2030. The bank’s analysts indicate that bitcoin behaves increasingly like gold, with lower volatility and little correlation with other assets, which positions it as a possible complementary reserve option, although gold would maintain its leadership for now.

From a regional perspective, Latin America maintains a secondary role in this adjustment. Although Brazil shows a trend moderate decline in its assets, with 168 billion dollars recorded in January, current selling pressure comes mostly from economies outside the hemisphere.

Historically, the region represents less than 10% of these global assets, and their central banks often prioritize exchange rate stability through diversified reserves.

At the end of the first quarter of 2026, the downward trend persists. The evolution of these portfolios will depend on critical factors such as the duration of hostilities in the Middle East and the ability of US bonds to continue offering security in a world where, for many central banks, energy liquidity has become the top priority.