The high interest rates on these loans make it difficult to repay on time.

Globally, a private credit crisis is forming.

In Argentina, 6 out of 10 families resorted to non-bank debt in the last six months, that is, outside the traditional financial system, to cover basic expenses such as food, services or rent.

It is a phenomenon that reflects the situation that the country is going through: It is no longer about financing consumption, but about going into debt to make ends meet. This is reflected in a report from the consulting firm Focus Market, released on April 6, 2026.

The analysis is based on a survey carried out on 2,670 households, complemented with data from the Permanent Household Survey (EPH) for the third quarter of 2025 and statistics from the Central Bank of the Argentine Republic (BCRA).

The report indicates that Argentine households accumulate more than 39 trillion pesos (approximately 27 billion dollars) in debt: of these, 32.1 trillion Argentine pesos correspond to the banking system and 6.9 billion Argentine pesos to non-banking commitments.

The gap is also reflected in the averages per household, with bank debts that are around 5,702,809 pesos compared to 1,149,431 pesos in the non-banking segment.

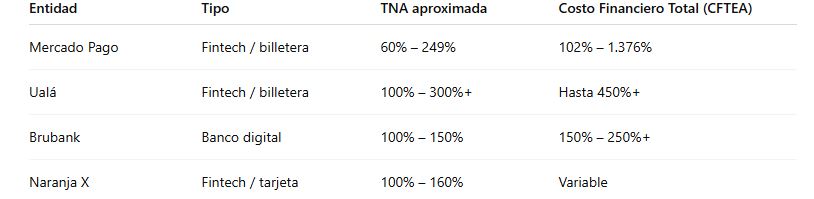

Fast credit, but increasingly expensive

In a context of salaries lagging behind inflation and a cost of living that continues to increase, more and more families are turning to non-bank credit, that is, loans granted by neobanks and digital platforms, such as Mercado Pago, Ualá, Brubank or Naranja X, instead of traditional banks.

The main attraction is speed: almost immediate approval and low admission requirements. But that access comes at a high cost.

The rates vary depending on the user profile, but in all cases they are at high levels. In Mercado Pago, for example, personal loans can have nominal rates ranging from approximately 60% to 249% annually, with a total financial cost that can range between 102% and 1,376%.

In Ualá, loans start from rates close to 100% and can exceed 300%with total costs that reach over 450% annually.

Brubank, for its part, rates tend to move in a range between 100% and 150%, with financial costs that can exceed 250%, while Naranja rates close to 100%–160% annuallydepending on the client.

This means that many families take on expensive debt to cover basic expenses, which ends up aggravating the problem they are trying to solve.

And from here another issue arises to take into account: the problem is not only credit, but default.

In January 2026, Delinquency in loans to households reached 10.6%, the highest level in more than two decadeswith 15 consecutive months on the rise.

A bubble that could burst worldwide

What happens in Argentina is not an isolated case. At the international level, Signs of tension begin to appear in the private credit marketa segment that grew strongly outside the traditional banking system, as CriptoNoticias has been reporting.

“The global financial system is sitting on a time bomb made of cheap credit,” warned analyst Charles Hugh Smith.

The bottom line is structural: both locally and internationally, credit outside the banking system can expand rapidly, but that growth is not always accompanied by an improvement in income or economic activity.

When that gap widens, Debt becomes more difficult to sustain, increasing the risk of tensions and fragility in the systemsince the lending companies themselves are beginning to be harmed by borrowers’ defaults. If there were a massive collapse of lending companies, there would be a chain effect that would affect several areas of the global economy.