The tax system allows compensation for capital losses to reduce the payment of taxes on savings.

The lack of tax culture prevents taking advantage of legal benefits by not closing declining positions.

The collapse in the cryptocurrency market does not necessarily imply a pause in obligations to the treasury. While thousands of investors in Spain maintain portfolios in negative values after the bullish cycle of 2021, the lack of management of these losses could lead to administrative complications before the Tax Agency.

This situation leads various analysts to warn that the 2025 Income tax calendar requires a proactive review, even when the financial balance is unfavorable.

The discussion becomes relevant this April 13, 2026 after a intervention by Esteban Rivero, founder of Cero Uno, Spanish specialist in cryptoasset taxation. He observes that many users will be forced to report their movements to the Treasury in the next tax return after having held assets that have lost between 87% and 99.9% of their value.

Thus, the warning highlights that, although there are no benefits, the exchange or sale of these currencies generates a change in assets that must be reflected in the tax history of the taxpayer.

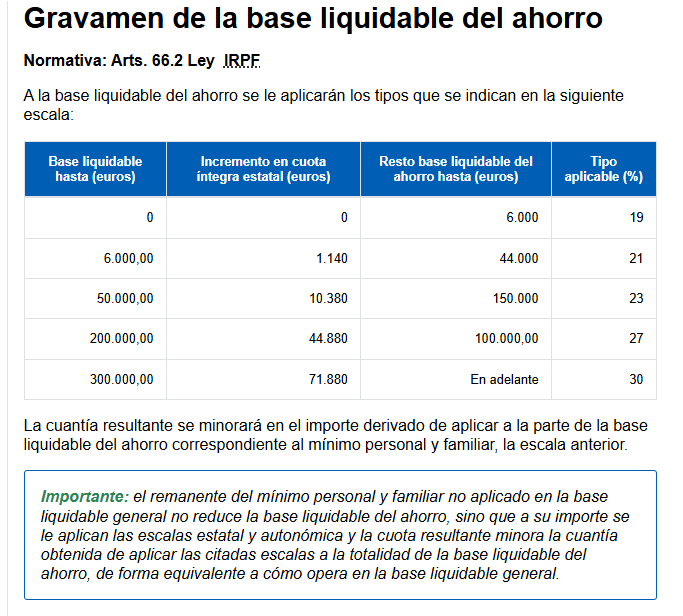

Precisely in the Spanish system, cryptocurrencies are taxed as property assets, so each sale or exchange of a token activates a taxable event where the profit or loss is determined by the difference between the acquisition value and transmission.

Under this tax framework, the results are consolidated in the savings tax base. The strategic value of this process lies in the compensation of losses: a tool that allows losses to be subtracted from the profits obtained in the same year.

For example, if an investor loses 2,000 euros when selling an altcoin, but gains 2,000 euros with bitcoin, his tax base would be zero, and he would be exempt from paying taxes on that profit. However, this mechanism, which can be applied even to profits from the following four years, It is wasted if the user keeps their portfolios “in the red” without executing the formal sale.

“Every day I see investors who continue to maintain these positions today, and they are going to have to manage the tax they must pay in the Personal Income Tax (IRPF) in Spain,” said the specialist.

“There is a lot of culture missing at the tax level,” Rivero added, suggesting that prolonged inaction can prevent the taxpayer from taking advantage of the legal benefits of disability compensation.

In this context, the official data reflect a significant gap in the tax formation of the sector. According to the 2023 Income records, of the more than 286,000 operations declared, 151,000 were closed with a negative balance.

Despite this volume, studies by TaxDown and Criptan indYodog that 70% of Spaniards with exposure to cryptoassets do not know how to declare correctly these movements, a significant figure in a market where the average investment per person is close to 5,000 euros.

At the same time, the state’s supervision capacity has been strengthened, as reported by CriptoNoticias. The Treasury already consolidates data from local exchanges through forms 172 and 173, in addition to information on assets abroad via form 721.

The European DAC8 directive will be added to this framework in 2026, designed to standardize the automatic exchange of information between the Member States of the European Union and reduce the margins of opacity.

This regulatory evolution generates divided positions. While one sector of the community prioritizes long-term accumulation without considering tax cycles, other investors They begin to execute strategic sales to declare their losses and thus reduce the overall tax burden of their portfolios. The recommendation agrees that planning should be an integral part of asset management, and not a last-minute procedure.

For the moment, the analysis of the sector continues to generate debate while the Tax Agency maintains its policy of updating control mechanisms. Although the mere possession of an asset does not generate an immediate debt, any exit from the position during fiscal year 2025 will activate a reporting process that requires precision to avoid sanctions or wasting the current compensation mechanisms.