Defaults in households went from 2.9% to 11.2% in one year, reflecting pressure on income.

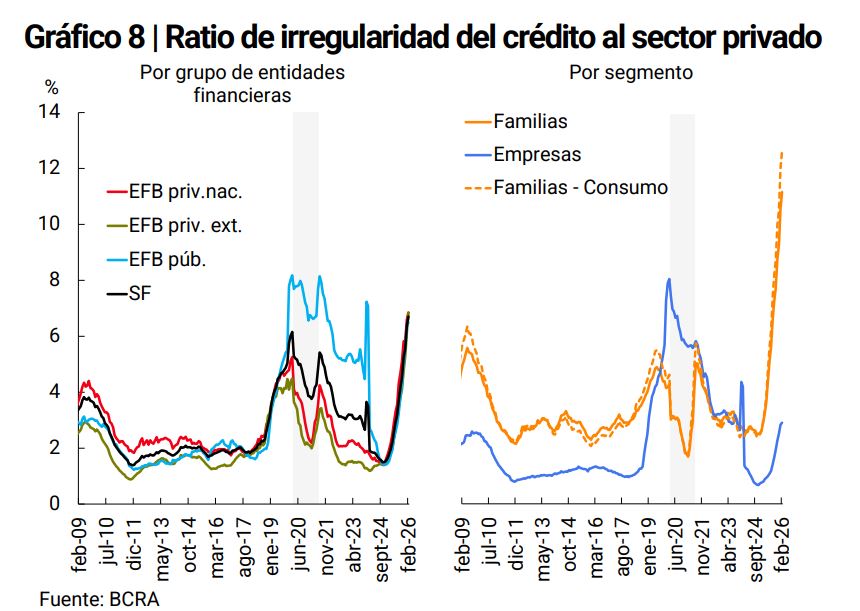

The level of irregularity in credit to the private sector reached 6.7%.

Late payment of loans in Argentine families reached 11.2% in February 2026, according to the most recent report from the Central Bank (BCRA).

This surveywhich was published on April 24, shows a sustained deterioration in household credit, in a context of pressure on income and lower consumption dynamism.

This current level is contrasted with the values observed at beginning of 2025. According to official data from the BCRA, family defaults were around 2.94% in February of that year. From that reference, This implies that, in one year, household delinquency multiplied by 3.80.

It should be noted that default is the delay in paying a debt. In banking terms, it measures what proportion of the loans granted show non-compliance with quotas.

The comparison is not consolidated in a single BCRA report, since the entity publishes monthly data without reconstructing the evolution of the complete data in each edition. However, when cross-referencing reports from different periods, the magnitude of the deterioration becomes evident.

In turn, the non-performing ratio of credit to the private sector (an indicator that measures the proportion of loans with payment problems over the total loans granted) stood at 6.7% in February, with an increase of 0.3 percentage points compared to the previous month and 4.9 points in the interannual comparisonconfirming a broader deterioration of the financial system.

The report also shows that this phenomenon occurs in a context of contraction of credit in pesos to the private sector, which fell 1.5% in real terms (discounting the effect of inflation) during February. The dynamics were heterogeneous: loans with “real collateral” (such as a vehicle or a home) grew, but commercial and consumer loans decreased, directly affecting the financing capacity of families.

The graph on the credit non-performance ratio allows us to clearly see the recent deterioration. In the right panel, the solid orange line represents defaults in families, while the blue line shows defaults in companies.

There you can see how defaults in homes accelerate strongly in the final stretch exceeding 11%, while that of companies remains at significantly lower levels, around 2.9%.

In turn, the dotted orange line (corresponding to the consumption segment within families, such as credit cards) shows an even more marked dynamic, with peaks above the general average, indicating that the deterioration is more intense in personal loans and cards.

Overall, the graph shows a clear divergence: the problem of late payment is concentrated in households, especially in consumer credit, while the corporate segment shows a more stable behavior.

A global credit crisis is brewing

What is happening in Argentina occurs in a sensitive international context for private credit. As CriptoNoticias has been reporting, this market grew strongly outside the traditional banking system and today faces greater signs of tension.

Analyst Charles Hugh Smith warned that “the global financial system is sitting on a time bomb made of cheap credit.” The warning points to the risk that debt has grown faster than income and real activity.

When this gap widens, payment difficulties increase and so does the pressure on lenders. Therefore, the rise in defaults in Argentina can be read within a broader credit fragility, which is not limited to the local market.