Pantera analyzed 542 tokenized assets with a total value of $320.6 billion.

77.6% belong to the “wrapped” category, a digital version of traditional assets.

Investment firm Pantera Capital posits that the real-world asset (RWA) tokenization market is still in an early stage of development.

In his most recent reportpublished on May 6, 2026, Pantera notes that much of the RWA industry continues to replicate traditional financial structures, rather than building truly native instruments for decentralized networks.

To support his thesis, specialists compared the current moment of tokenization with the early years of the Internet. In this regard, they say:

The first stage of internet media consisted of newspapers copying and pasting articles onto websites. Delivery speed improved. Availability was expanded. But the format was identical.

Pantera Capital, investment company.

For the firm, something similar is currently happening with a large part of the tokenized assets: The technological channel has changed, but the operational logic remains almost the same as in traditional finance.

Most of the assets are still in the “wrapped” phase

The company analyzes 542 tokenized assets from 11 different categories, equivalent to about $320.6 billion in tracked market value. The study concluded that 77.6% of the products evaluated still belong to the “wrapped” categorythat is, structures where a digital token exists, but the actual functioning of the asset continues to depend on the underlying asset held by custodians, external registries and traditional financial intermediaries.

An example of this model is some tokenized US Treasury bond funds, such as BlackRock’s BUIDL, where the token functions more as a digital proof of the real asset than as a completely autonomous instrument.

In that graph, the brown color represents the “wrapped” assets, which are 460 of the 593 surveyed. Gray corresponds to hybrid assets, with 66 cases. Dark green marks the native assets, just 16. Beige identifies 51 unqualified assets, because they correspond to pilots or advertisements that are not yet active. The main reading is that 77.6% of the market remains concentrated in the “wrapped” phase.

The report maintains that, in many cases, “the token adds a layer of data, but does not change anything about how the asset actually works.”

Pantera also developed its own index called Tokenization Progress Index (TPI), designed to measure the actual degree of tokenization maturity. The general average obtained by the assets analyzed was 2.04 points out of 5.

Pantera measures the maturity of each tokenized asset based on three dimensions: issuance and redemption; transferability and settlement; and complexity and composability, that is, the ability of an RWA to be integrated and used within other digital financial protocols. In the graph, light green represents the first dimension; the dark green, the second; and yellow, the third.

Stablecoins appear as the most advanced category, with better combined scores. At the opposite end are real estate (real estate) and private investment capital (private equity)two categories that still present low operational maturity.

One of the central data of the report indicates that 91.1% of the assets evaluated still depend on issuance and redemption mechanisms controlled by administrators or custodians. Only 13 assets reached models considered autonomous. This dependency explains why many products continue to function as “wrapped”: The token may exist on the network, but its issuance, redemption, or validation is still tied to external infrastructure.

The company clarifies that this does not imply that the wrapped tokens are useless. In fact, it recognizes that they can improve distribution, access and operational speed. However, considers that they still represent an initial stage of the process.

For Pantera, the main problem is clear: “The market is getting broader, not deeper.”

The market grows, but remains concentrated

According to the study, In 2025, 168 new tokenized assets were launched, a growth of 115% compared to the 78 products registered in 2024. However, the majority of these launches continue to replicate models of low technological complexity.

The stacked bars show the number of new tokenized assets launched each year, divided by asset class. The gold line reflects the value on-chain total of the market. The most marked jump is observed between 2024 and 2025, when the value went from 200.6 billion dollars to 313.7 billion. At the 2026 cut, the market reached $321.1 billion.

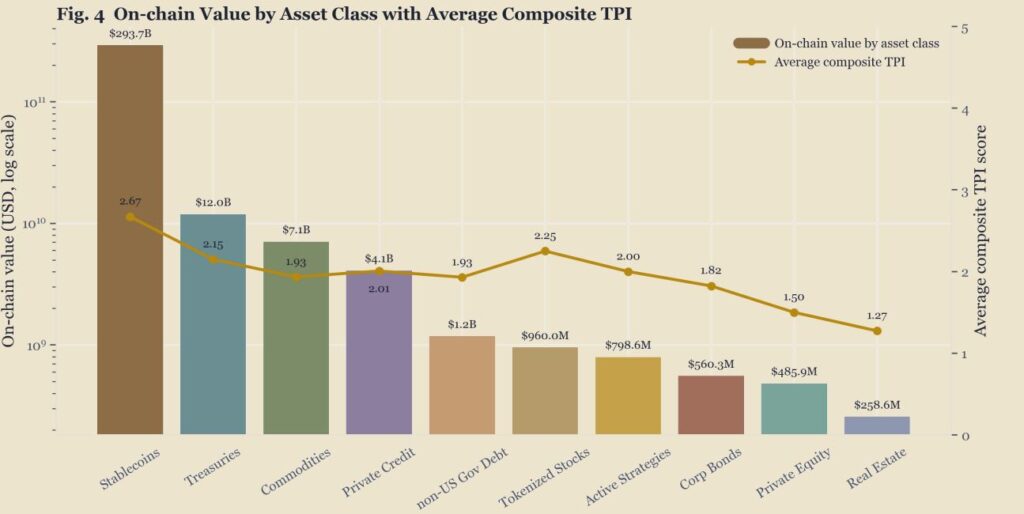

The document also shows a strong market concentration. Stablecoins represent $293 billion, equivalent to 91.6% of the total value tracked by Pantera.

In this graph, the bars indicate the value on-chain of each asset class, while the golden line marks the average TPI of each category. The stablecoins concentrate 293.7 billion dollars and have the highest average TPI, of 2.67. They are followed by tokenized US Treasury bonds, with $12 billion and a TPI of 2.15. The difference shows that the market is not only concentrated in one asset class, but also in the category that achieved the highest operating profit.

According to the firm, stablecoins are currently the only category that It achieved significant economic scale along with concrete utility within the digital financial ecosystem.

Pantera considers truly “native” products to be those designed directly to operate on decentralized infrastructure, without relying on parallel registries or external manual processes.

Among the most advanced examples mentions sky dollar (USDS, formerly DAI) from MakerDAO and GHO from Aave. Unlike traditional wrapped assets, these assets were created to function entirely within automated protocols, with issuance, collateralization and operations managed through smart contracts, as explained by CriptoNoticias.

The report argues that the next stage of tokenization will not be defined by simply “putting more assets on the network,” but rather by building instruments that are impossible to replicate through traditional financial infrastructure.

At this point, Pantera mentions future products with continuous settlement, automatic collateral management, programmable generation of financial performance and assets whose cash flows, risks or ownership rights can be separated and traded individually in real time.

The report also highlighted that large traditional institutions are already actively advancing tokenization. These include BlackRock, Franklin Templeton, Fidelity, WisdomTree and JPMorgan, mainly through products linked to tokenized US Treasury bonds.

Specifically, Franklin Templeton projects a more accelerated expansion of the market and highlights that tokenization will end up integrating traditional financial institutions and digital assets into a common infrastructure. In fact, it predicts that it could exceed $16 trillion in 2023.

However, Pantera highlights that even a large part of these institutional developments continues to operate under “wrapped” models, where core processes continue to depend on traditional financial infrastructure and offline validations.