14% of those who apply for loans belong to a “financially sophisticated” group, says Ledn.

The loan market could reach USD 1 trillion in 5 years, the company says.

The market for loans secured by bitcoin (BTC) and cryptocurrencies shows stagnation. This scenario was revealed after an investigation carried out by the financial services company Ledn was disseminated.

The company surveyed 1,244 bitcoin holders in April 2026 to figure out why these fundings are not growing at the same rate as the overall digital asset economy.

He probewhich was carried out in the United States and Australia, revealed that the main enemy lies in the fact that users prioritize institutional trust and regulatory clarity over commercial benefits like interest rates.

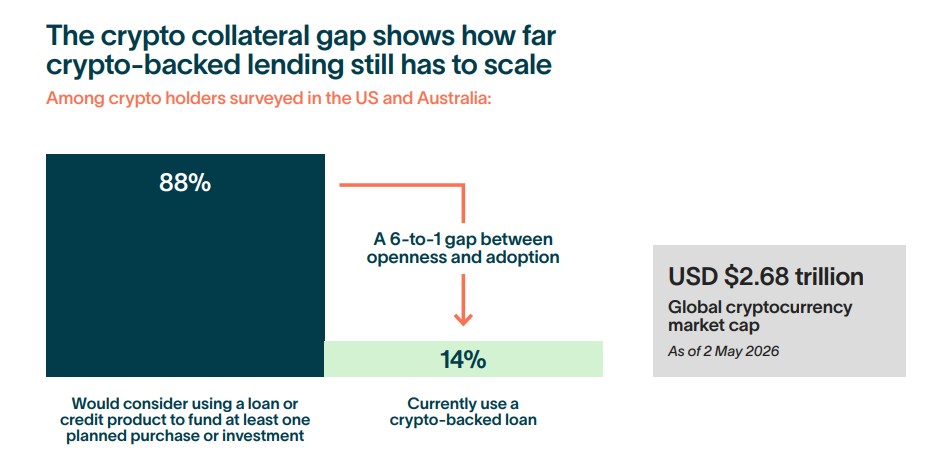

This study showed that 88% of those surveyed would consider requesting loans using their BTC as collateral, but currently only 14% do so. As the report’s authors explained, “this represents a 6 to 1 ratio between overall willingness to borrow and current use of bitcoin-backed loans.”

When those who do not use these services were asked about the reasons that hinder their adoption, “the barriers were mostly related to trust, not knowledge.” Users highlighted that The collateral or guarantee that they deliver in custody requires safeguards that mitigate the fear of losing their funds..

The three most common concerns reported in the study were “managing cryptocurrency price volatility, managing settlement risk, and regulatory uncertainty around cryptocurrency-backed loans.” Interest rates were relegated below these factors.

“Bitcoin is the only major asset class in which collateralized loans have not increased at the same rate as portfolio assets,” the platform’s report detailed. Those who do use the system make up a specific segment that avoids selling their belongings during price fluctuations.

“The 14% that do request loans belong to a financially sophisticated group.” This sector resorts to leveragea mechanism to operate with borrowed funds, with the goal of obtaining liquidity without parting with long-term holdings in the expectation that their value will increase.

«These are not borrowers looking for emergency liquidity. “They use loans to obtain capital without selling long-term positions, the same logic that drives margin loans in stocks and mortgage lines of credit in real estate,” details the financial firm.

The document adds that 72% of owners agree that these instruments “facilitate access to funds without having to sell them, which reinforces the role that these products play in helping holders access capital while maintaining their exposure to the market.”

«Currently, tens of millions of people own bitcoin, it is managed by regulated institutions and analyzed by major rating agencies; However, loans secured by bitcoin are still in their infancy compared to any other traditional asset class of this size,” said Venezuelan businessman Mauricio Di Bartolomeo, co-founder of Ledn.

«The lawsuit has already been resolved. What is still being developed is the trust infrastructure that provides borrowers with the necessary security to operate,” added the executive.

Ledn estimates that this consumer market could scale from the current $3 billion to $1 trillion within a period of five to ten years.

Despite this optimistic projection based on the maturation of the infrastructure, the reality of the commercial environment shows latent dangers of capital loss. For example, on March 16, 2026, the lending, trading and custody platform BlockFills made its insolvency official before the United States authorities, as reported by CriptoNoticias. This entity had to completely paralyze its operations after facing a severe liquidity crisis.

In contrast, there are commercial initiatives that seek to expand financing options. The mortgage firm Better, in alliance with the Coinbase exchange, launched a program on March 26, 2026 that allows you to use bitcoin or the USDC stablecoin to cover the down payment on homes.

Resolving the six-to-one usage gap will depend on the adoption of reserve testing audits and clear regulatory frameworks. The speed with which these tools are implemented will determine whether the sector can overcome the fear of corporate bankruptcies and stabilize the financial ecosystem developed based on bitcoin and digital assets.