The Department of Labor is considering creating “safe harbors” to regulate bitcoin in savings accounts.

Latinos in the US lead the adoption of BTC, but only 35% have a retirement plan.

Saving for retirement in the United States often conjures up an image of predictable stability: mutual funds, bonds, and a steady trickle of dollars accumulating over decades in a savings account called a 401(k). However, a quiet regulatory battle in Washington is about to introduce bitcoin (BTC) and cryptocurrencies to the retirement plan board.

The Blockchain Association submitted a formal letter of support to a new rule Department of Labor (DOL) to pension administrators evaluate digital assets under the same magnifying glass of neutrality as any other investment.

This initiative seeks to reverse an order issued in 2022, under the Joe Biden administration, when the US government issued severe warnings against the inclusion of crypto assets in retirement savings.

Now, the new proposal, published on March 30 under President Donald Trump’s guidelines to reduce obstacles to alternative investments, changes the approach.

Instead of banning, create “safe harbors” (or safe harbors) covered by the historic ERISA law. This means that a manager will not automatically be penalized for listing bitcoin, as long as it demonstrates with documentation that it has carefully analyzed rigorous factors, including fees, liquidity, estimated return and market complexity.

The potential impact of this legal technicality is important, as it regulates the destiny of billions of dollars belonging to more than 90 million workers.

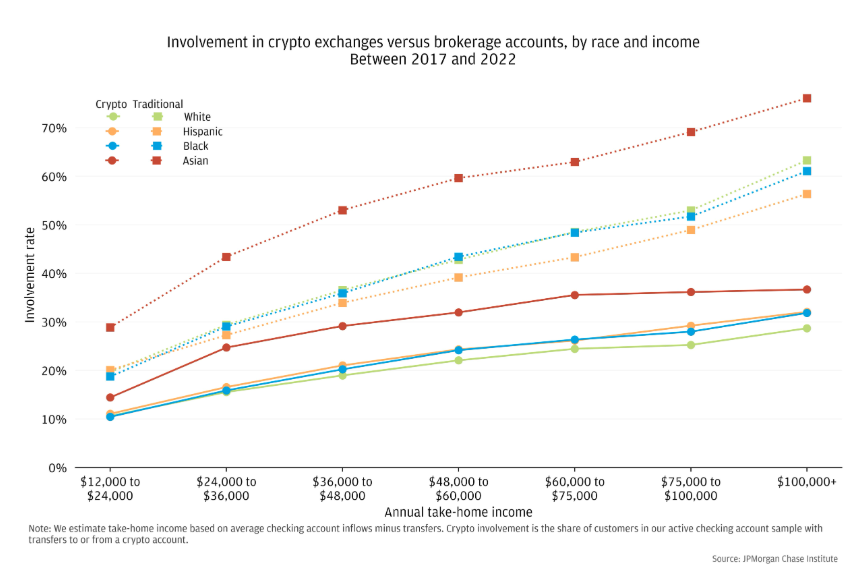

For the Hispanic community in the United States, the measure contains a profound paradox. On the one hand, Latinos record adoption and use rates of cryptocurrencies individually notably higher than the national average; On the other hand, their participation in formal retirement plans sponsored by companies is barely between 30% and 35%.

“Americans should not be blocked from accessing digital assets just because they are related to cryptocurrencies,” the Blockchain Association argued, suggesting that the reform could be the incentive that brings Hispanic workers closer to the institutional savings system through an asset they already know.

However, the idea of mixing the future of workers during their old age with crypto assets is something that raises widespread alarm. Organizations like the Economic Policy Institute and Better Markets warn that these assets such as bitcoin and cryptocurrencies weaken the fiduciary responsibility of administrators and prioritize industry interests over employee safetyexposing family funds to extreme volatility.

However, these criticisms ignore that although bitcoin is usually classified as a highly volatile asset in the short term, it has accumulated more than 16 years raising its overall value. This is a constant long-term appreciation that is not shared by traditional currencies such as the dollar, whose purchasing power tends to depreciate despite being historically perceived as low-volatility refuges.

In any case, regarding the status of the measure to allow bitcoin in retirement funds, the public comment period closed on June 1, 2026, and Now the ball is exclusively in the Department of Labor’s court..

The institution must process the avalanche of opposing opinions to draft the final text. Its verdict will depend on whether Wall Street unifies investment criteria allowing bitcoin to colonize pension funds, or if it maintains the exclusion barriers.

And while the United States decides, Latin America has already begun to chart its own path. As CriptoNoticias recently reported, in Colombia, the pension giant Porvenir launched a voluntary pension portfolio that offers regulated exposure to bitcoin through the BlackRock ETF, joining a trend already integrated by local competitors such as Skandia and Protección.

This resolution in Washington, therefore, will not only redesign the wealth of millions of future American retirees, but will also end up shaping the speed of the global regulatory evolution of digital assets.