For the specialist, most people do not want a stablecoin, “they want a dollar.”

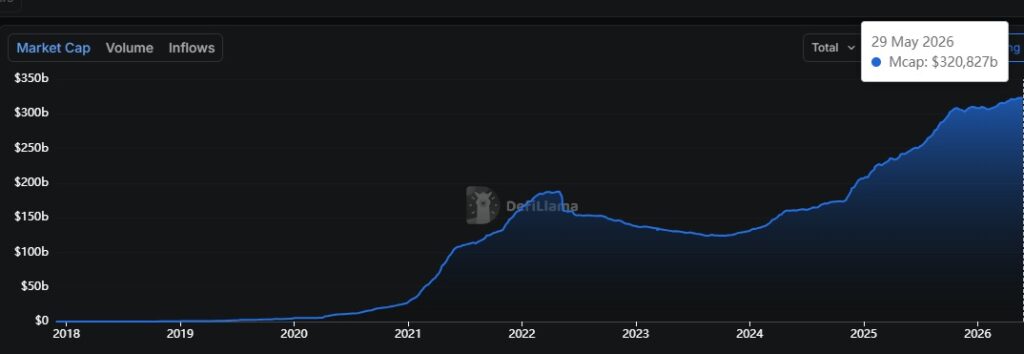

In his opinion, the capitalization of stablecoins at 305 billion “is not a peak.”

The stablecoin market is undergoing a structural transformation that transcends financial speculation, to become an intrinsic part of the daily lives of many users around the world.

This is how Reeve Collins, co-founder of Tether, sees it, who explains that these digital assets should not be considered traditional cryptoassets, such as ether, bitcoin or XRP, for example. In his opinion, stablecoins They are a “new format for money” that has adapted to people’s daily lives.

According to the specialist, the expansion of these financial instruments demonstrates that the infrastructure based on distributed accounting technologies is ready to absorb the flows of the global economydriven by the need to solve real-world logistics problems and by key partnerships with traditional payments giants like Visa.

Collins asserts that the fact that the stablecoin market is growing and exceeding USD 320,000 millionin contrast to the rest of the cryptocurrencies, is a demonstration of the differentiation between these assets. In his opinion, Stablecoins go beyond being “speculative instruments.”

«A speculative asset lives and dies according to market sentiment. When sentiment changed and much of the crypto market retreated, the supply of stablecoins continued to grow. Two things moving in opposite directions at the same moment are not the same kind of thing. The market was separating the trade from the tool, for everyone to see,” he says in an exclusive interview with CriptoNoticias.

In the founder’s opinion, the figure of 320,000 million dollars “is not a peak”, but rather evidence of a adoption of a structural nature. He ensures that the main users of this technology are not looking to make financial bets, but rather to find solutions to everyday cross-border inefficiencies. The specialist clarified the motivation behind this phenomenon:

Most people don’t want a stablecoin; wants a dollar. What they want is a dollar that moves globally, settles quickly, operates twenty-four hours a day, and works natively on the internet.

Reeve Collins.

What Collins says has been demonstrated in practice, especially in Latin American countries such as Argentina and Venezuela. More precisely in the Caribbean nation, the use of stablecoins has proliferated significantly in the last year as a result of the scarcity of physical currencies. and the need to protect oneself from inflation and devaluation.

CriptoNoticias has documented how people, businesses and companies from Venezuela have joined the stablecoin ecosystem, relying on local and international platforms that have facilitated the retail and commercial adoption of these digital assets.

The breakdown of the traditional banking model

In analyzing the reasons why the financial system has failed to optimize international transfers, Collins points to design flaws in correspondent banking which, he says, They end up being lucrative for the institutions.

So remember that money, unlike information, is still trapped in an “obsolete infrastructure of manual records and reconciliations” because, in his words, “inefficiency pays dividends.”

«The system is not broken. Works exactly as designed. The part that most people overlook is that design is profitable. Each institution in the chain charges a fee and each settlement window creates economic value for someone holding the money in transit. The slowness was never an accident, it was the product,” agrees the specialist.

The founder of the WeFi finance platform believes that, in the face of this scenario, Bitcoin technology offers an alternative architecture based on shared ledgers.

He explains that this innovation allows direct settlement with fewer intermediaries and total availability of the service. However, the co-founder of Tether warns that the attribute most valued by current participants is the transparency of the process:

One of the biggest frustrations in international payments is that money disappears in a process that no one can see. With blockchain-based settlement, every move is visible. Many institutions embracing on-chain settlement will tell you that transparency is as valuable as speed. For the first time, they know where the money is throughout the entire process.

Reeve Collins.

The operating environment for digital currencies is changing rapidly with the emergence of federal regulatory frameworks such as the GENIUS Act in the United States or the MiCA regulation in Europe.

According to Collins, these rules provide essential legal certainty for the entry of large players, such as banks, asset managers and governments. “Regulation does not create the market, it unlocks one that was already there,” he clarifies.

As you see it, this regulatory clarity has allowed traditional companies like Visa to integrate into the ecosystem, solving what the businessman calls “the last half mile” of banking based on decentralized networks.

Remember that, previously, funds in digital assets were isolated from daily trading due to the need to resort to exchange platforms for conversion to fiat money.

But now, the alliance with global payment networks allows balances in cryptocurrency wallets—whether under custody or self-custody schemes— can be used directly in traditional points of sale. This way, “settlement happens in the background and the payment experience looks exactly the same as any other card payment.”

Despite the progress, Collins warned of the risks inherent in the process of regulatory institutionalization. He affirms that there is a latent danger that the new regulatory frameworks act as barriers to entry that limit innovation and perpetuate financial exclusion.

The usual pattern when a category is regulated is that clarity favors established players. Firms with greater regulatory resources often move first, the market consolidates around the players already leading it, and the framework everyone calls progress can quietly become a barrier to entry. You can fully comply with every rule Congress passes and still build something that only serves people who already have access to the financial system.

Reeve Collins.

On the other hand, the specialist identifies a new niche of inefficiency in the international philanthropy sector, where he denounces that more than 200,000 million dollars remain held in donor-advised fundsaccumulating returns for the managing entities instead of going to the final beneficiaries. Faced with this, he proposes the concept of “programmable compassion” by using technology to automate and audit the flow of donations:

“The same infrastructure that allows a stablecoin to separate performance and direct it to users can direct the return of philanthropic capital towards the causes it was always intended to support,” he points out. “The question that makes large-scale philanthropy difficult to trust (‘did the money really arrive?’) becomes something you can check instead of waiting for it to happen,” he adds.

Projecting the state of the industry for the next five years, Collins foresees a radical change in the interaction of users, who, he says, They will delegate the mechanical execution of their finances to artificial intelligence (AI) agents. At that point in development, costs and speed of transfer will cease to be competitive factors and become basic generic commodities, depending on your perspective.

In Collins’ vision, the true consolidation milestone for distributed network-based banking will occur when the underlying technology becomes imperceptible to the mass public, repeating the pattern of adoption of other global information infrastructuressuch as emails or text messages, for example.

The milestone that will tell me that on-chain banking has become massive is the same one that all successful infrastructure reaches: invisibility. Nobody thinks about the TCP/IP protocol when sending an email. Nobody thinks about cloud computing when they open an app. Eventually, no one will think about blockchain when moving money. They won’t know that the infrastructure changed. They will only know that their money is finally working as it always should have.

Reeve Collins.

This narrative, that people will pay without knowing that an entire cryptographic and decentralized gear moves behind the operation, has been a point of debate among companies in the sector.

In fact, at the Venezuela Tech Week event, held last May, representatives of Bitfinex and BitGo agreed on the idea that cryptocurrencies are not coming to supplant traditional rails, but to integrate into them, without the end user knowing what is happening.

With a perspective that separates the usefulness of these instruments from the speculative volatility characteristic of assets such as bitcoin (BTC) or ether, the analysis of the co-founder of Tether suggests that stablecoins are completing their migration from exchange tools towards the day-to-day monetary infrastructure.

In essence, the convergence between clear rules and technical accessibility seems to be forcing an evolution where money begins to respond to the operational needs of users and not to the prerogatives of conventional financial intermediaries.