From the aunt in the Cúcuta market to the mechanic in Maracaibo, USDT is already the payment of every day.

Is it about financial inclusion… or is it simply changing the color of the master?

On the streets of Venezuela, Argentina, Colombia or Bolivia, fiat money can vanish before it hits your pocket. In Latin America, decades of inflation have turned savings into a mirage that a single political decision can erase overnight. In that void an ally appeared that no one expected. It has no branches, it has no ATMs on the corners, it is not accountable to any local economy minister. It only exists in the digital world, but for millions of Latin Americans it is already more real than the role of the dollar issued by the Federal Reserve (FED). It is called USDT from the Tether company and, for better or worse, it has become the de facto dollar of half a continent.

The true dimension is felt in the routine. She is the mother in Cúcuta, in Colombia, right on the border with Venezuela, who receives 200 dollars in USDT from her husband in Miami. She knows she has to go to the neighborhood store to exchange them for rice, oil and diapers, but she can do it in three days because she no longer has the money. extreme concern that the Colombian peso will lose another point in the afternoon.

He is also the mechanic from Maracaibo, in the oil-producing west of Venezuela, who gets paid for the week every Friday. You do not receive it in the bank’s dollar, not in parallel dollars. It is USDT, the digital stablecoin that is used so that Monday is enough for bread and fare.

Likewise, he is the merchant from La Paz, in the middle of the Bolivian highlands, who accepts payments in stablecoin from Chilean tourists and avoids three-day lines and bank commissions. For them, USDT is the certainty that Monday’s money will still be worth something on Friday.

In a popular market in eastern Venezuela, I asked a vendor why I used USDT and not bitcoin (BTC). He looked at me as if the question came from another planet and then answered without hesitation: “I don’t want a coin that promises to make me rich tomorrow. “I want one that prevents me from continuing to become poorer today.” That simple phrase, said between bags of onions and boxes of tomatoes, is a reflection of what is happening in almost the entire continent.

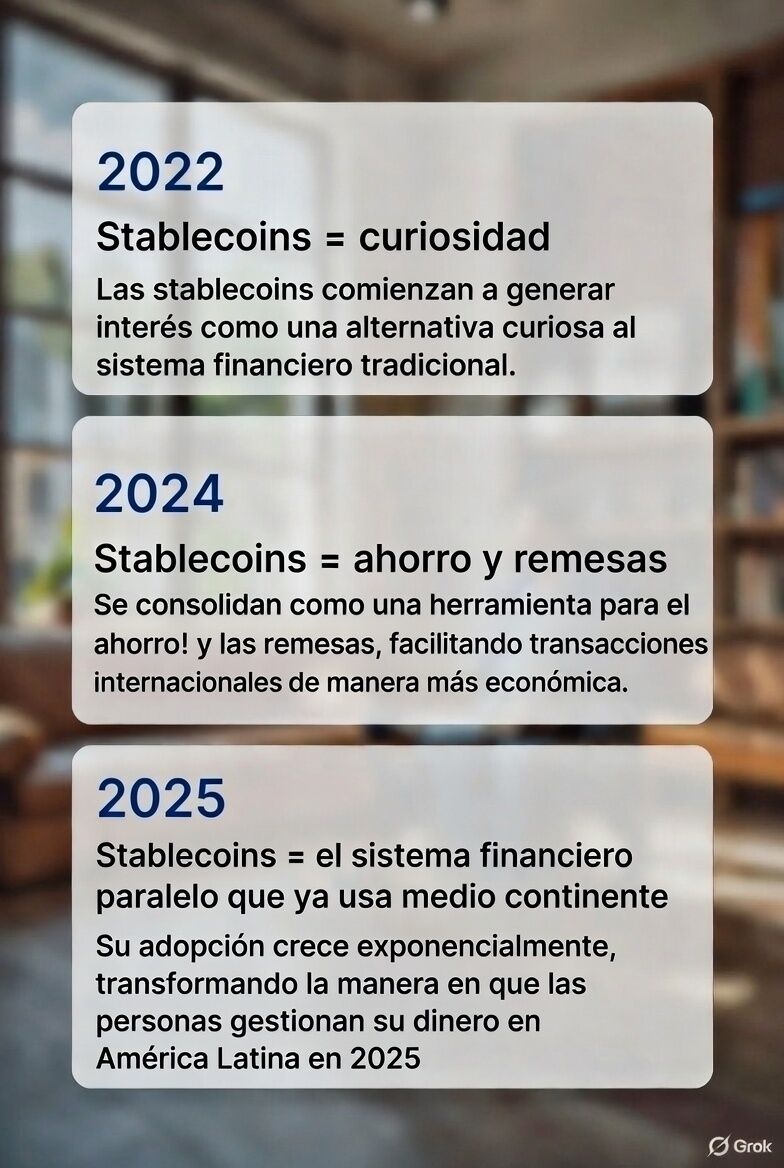

The genesis of this dependence dates back to the inflationary crises of 2018, but 2025 has marked its institutional consolidation. According to Juan José Martínez, a Venezuelan cryptocurrency enthusiast, the trend responds to a visceral need. In an environment where the national currencies of Venezuela, Colombia, Bolivia and other countries on the continent are volatile and banking systems exclude 30% of the adult population, USDT offers something that local governments cannot guarantee. That is stability and immediate liquidity.

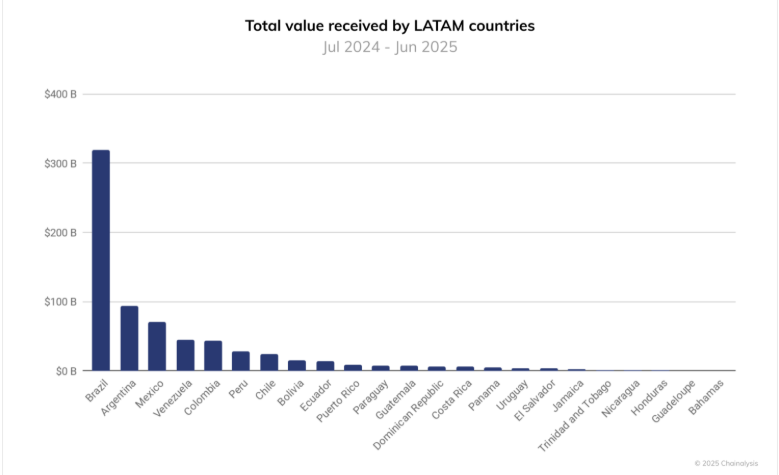

Between 2022 and 2025, Latin America moved 1.5 trillion dollars in cryptoassets, an annual growth of 63% that makes any traditional banking metric ridiculous. In Venezuela, USDT already covers 47% of local transactions and 30% of supermarket payments. In Argentina and Bolivia, history repeats itself: the stablecoin has become an informal reserve of value and a means of everyday payment because official money simply stopped fulfilling its function.

It is the market’s response to the sanctions and devaluation that it now uses a liquidity network that operates outside of traditional geopolitics.

Lifeguard or new colonialism?

For him 30% adults Latin Americans who remain without a bank account, USDT is the difference between eating or not eating at the end of the month. It offers instant liquidity, without lines, without documentation and without a bank classifying you as a “risk” for living in the wrong neighborhood. But the price is high.

On the one hand, Tether offers a real lifeline in economies where the bolivar melts at 270% annually or the Argentine peso loses 2% in a single week. USDT offers instant access to a slightly more stable dollarwithout lines at a bank.

On the other hand, it is the delivery of monetary sovereignty to a private company registered in the British Virgin Islands and regulated, ultimately, by the United States Department of the Treasury.

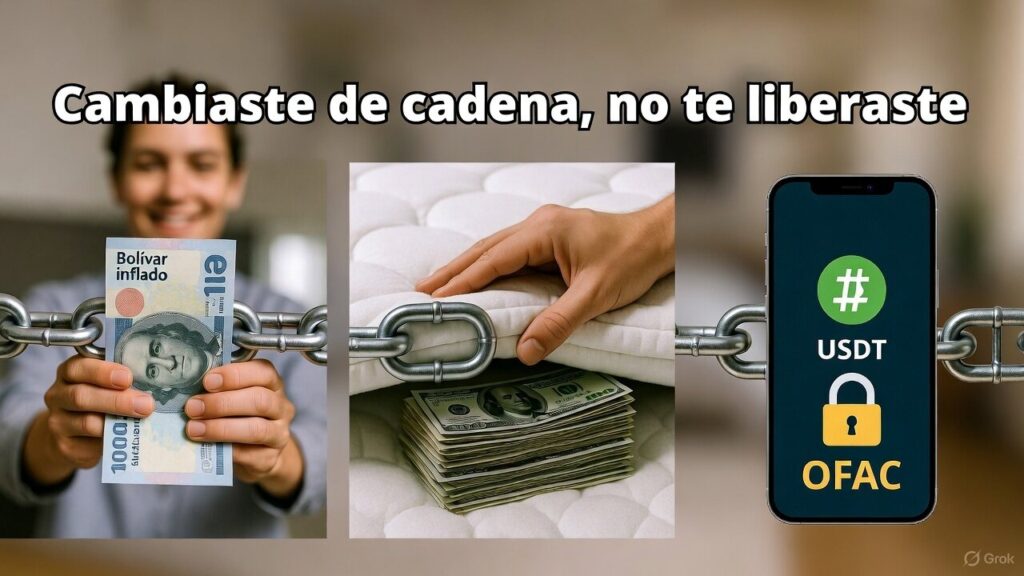

When you have 1 USDT in your wallet, you do not have a real dollar, but rather a simple ticket or digital check, itself a promise that Tether Limited will give you a US dollar (or its equivalent) when you claim it.

That note is theoretically backed by the company’s reserves (cash, Treasury bonds, loans and commercial paper), but Those reserves are controlled exclusively by Tether, not you. That is why USDT is not your digital dollar, but rather a digital dollar lent by a private offshore company that can freeze, redeem or lose it whenever it wants or when the government orders it.

That’s because each address can be frozen in seconds by order of the Office of Foreign Assets Control (OFAC), dependent on the United States Department of the Treasury. And it has already happened more than many times, as detailed in an editorial article by CriptoNoticias. It means that the monetary policy that really protects your savings is decided by the Federal Reserve, even if you don’t live in that country.

Of course, in practice, the average citizen he exchanged a local inflation that impoverishes him for a possible remote confiscation which can also impoverish it. It exchanged control of a corrupt government for control of a private entity and US regulators. It is a patch to cover the hole you have in your finances.

The net result is more efficiency when solving an immediate situation, yes, but also a new form of dependency in which you went from the bolivar to the physical dollar, from the physical dollar to the digital dollar issued by Tether. The systemic risk is brutal.

You changed one poison for another

If tomorrow Tether suffers a run, receives a massive freeze order or simply fails in its reserves, there is no lender of last resort for millions of businesses and families that today operate almost exclusively with USDT.

The collapse would be instantaneous and without a safety net. And therein lies the greatest danger: the extreme comfort of the patch can anesthetize the urge to fix what is broken.

As long as USDT works, local governments have less pressure to control inflation, to truly bank their population, or to launch credible sovereign digital currencies.

The patch that many believe is perfect ends up being the enemy of the real cure. In 2025, Latin America did not adopt USDT due to ideology, as is the case in bitcoin communities. He adopted it because it was the only option left on the table. The uncomfortable question is whether, by embracing that option, we are building financial inclusion or simply changing the color of the master.

Disclaimer: The views and opinions expressed in this article belong to its author and do not necessarily reflect those of CriptoNoticias. The author’s opinion is for informational purposes and under no circumstances constitutes an investment recommendation or financial advice.