Swift, the global financial messaging network that connects banks and institutions around the world, gave details of its plans to incorporate a distributed ledger based on cryptocurrency technology into its infrastructure.

More than 30 institutions are working on this initiative (including JPMorgan Chase, HSBC, Deutsche Bank and Bank of America).

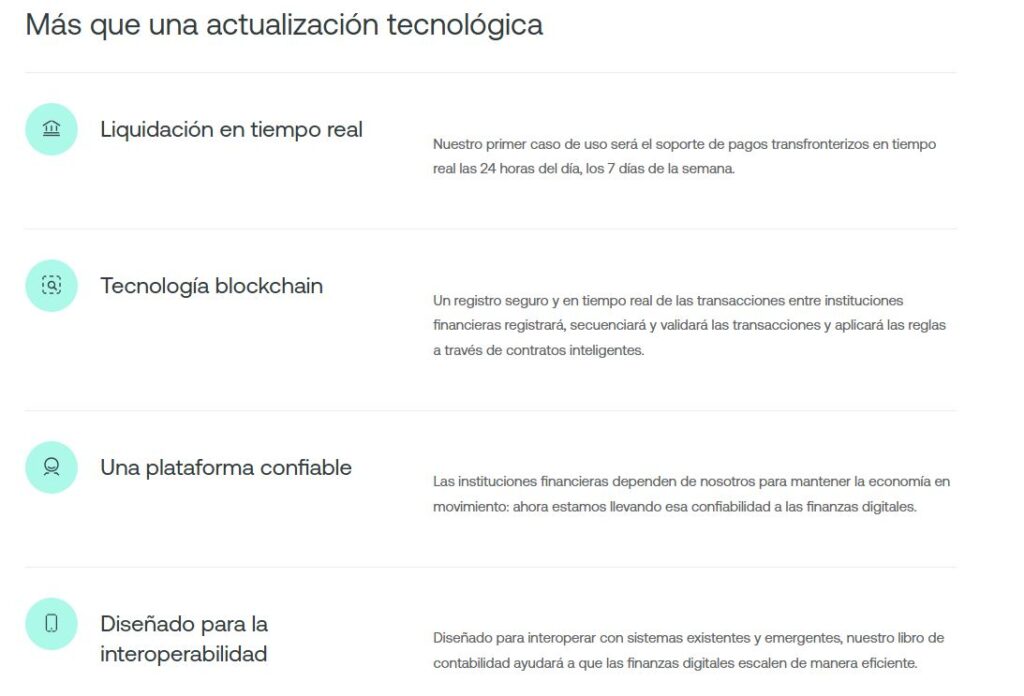

The development of Swift aims, first of all, to enable real-time cross-border payments, available 24 hours a day, seven days a week.

To do this, it relies on cryptocurrency network technology, with an accounting book that will record, organize and validate transactions between financial institutions.

Swift highlights that the proposal seeks to transfer its historical role as a reliable infrastructure of the traditional financial system to the field of digital finance.

The design prioritizes interoperability with existing and emerging systems. The goal is to facilitate institutional adoption and allow digital finance to scale efficiently.

“This is a game-changing measure for cross-border payments, providing a shared, real-time record of transactions between financial institutions and enabling instant, always-on payments,” indicated from Swift.

The development, which is advancing without the participation of Ripple Labs (the issuing company of the XRP cryptocurrency) raises a big question among the Ripple community: Is it a blow to XRP?

What happens is that, at not participate in the initiativea scenario of direct competition is configured with the objectives of the firm directed by Brad Garlinghouse.

“It does not replace XRP”

The XRP community has been attentive to Swift’s movements. This is demonstrated by the X user known as Chain Cartel, who think: “Swift just admitted it: it is building Ripple without saying Ripple.”

“Read what Swift says carefully,” he notes in a post on his X account. He then lists key concepts such as “shared, real-time ledger,” “always-on payments,” and “instant settlement between financial institutions.”

According to Chain Cartel, It is neither Bitcoin, Ethereum nor a generic technological experiment. “This is precisely the architecture that Ripple has been building for a decade,” he says.

In that sense, remember that “Ripple’s model was always based on a neutral settlement layer, real-time atomic completion, shared visibility of the ledger between institutions, interoperability with traditional rails such as Swift, RTGS (real-time gross settlement systems) and ACH (automated clearing houses), and a design focused on liquidity, not speculative consensus.”

As CriptoNoticias has explained, Ripple aims to facilitate payments between financial institutions, prioritizing speed, certainty in settlement and connection with existing infrastructure, rather than a system designed for speculation or retail use. However, so far, it has failed to implement this narrative in the market.

Chain Cartel points out that this Swift development is not direct competition for Ripplebut —according to him— it is a convergence.

“Swift doesn’t replace rails, it coordinates them. Ripple doesn’t replace banks, it connects them,” he explains. From their pro-Ripple speculation, the underlying message is clear: “Swift is recognizing that the future of the payments system needs a ledger layer. Not just messaging, and the only model proven at scale is Ripple’s.”

Finally, he warns that this process responds to a classic pattern of adoption by traditional systems: “First they describe it. Then they replicate it. Then they integrate it.” And he concludes with a forceful phrase: “The market is not yet discounting this.”

That is, Chain Cartel’s reading is that the development of Swift does not weaken Ripple. On the contrary, it reinforces the thesis that its approach is becoming the standard towards which global financial infrastructure converges. This is a change that, according to him, the market has not yet finished sizing.