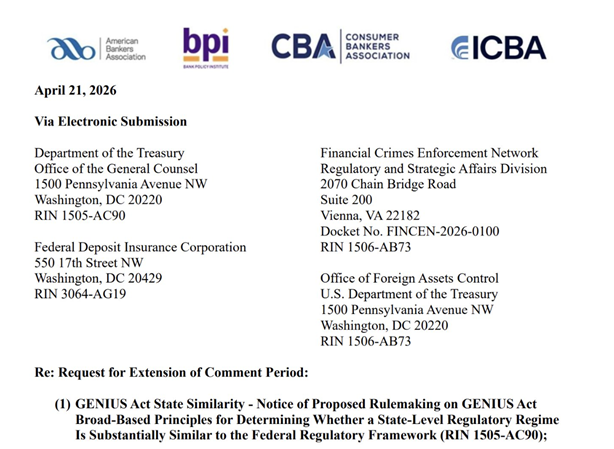

The regulation of stablecoins in the United States entered a new phase of delays on April 21, 2026, after the American Bankers Association requested a 60-day extension to comment on the implementation rules of the GENIUS law.

In parallel, Senator Thom Tillis warned that the Clarity law debate will not advance in April and could be moved to May due to the lack of consensus in Congress, especially around the treatment of “yield” (interest) in stablecoins.

The application of the banking sector is part of the regulatory development phase of the GENIUS law, where federal agencies continue to define the rules that will determine its application. The objective of the extension is to have more scope to evaluate the impact of the frameworkespecially in its interaction with the traditional financial system.

The GENIUS law, approved in 2025, establishes the first federal framework for stablecoins in the United Statesas reported by CriptoNoticias. The regulations require 1:1 support in high-quality liquid assets, periodic audits and supervision by authorized entities. Although it prohibits the payment of direct interest to holders, it allows certain rewards linked to the use of platforms, which has generated an area of open interpretation.

The Clarity law, for its part, seeks to define the classification of tokens and establish the distribution of powers between the Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC). However, Its progress continues to be conditioned by the lack of agreement on key aspects of the regulatory design.

The debate has intensified tension between traditional banking and the digital asset sector. While financial institutions push to limit any mechanism that could resemble a return on deposits, the industry maintains that The rewards linked to the use of platforms do not constitute interest, but rather adoption incentives.

In this context, Congress has chosen to extend the discussion deadlines and avoid accelerated definitions on concepts not yet agreed upon. This has contributed to slowing down the legislative calendar for both projects.