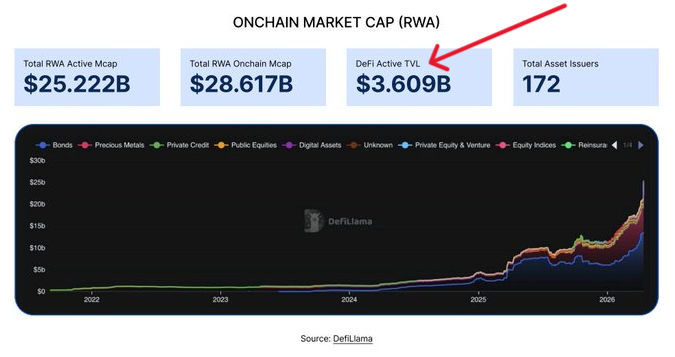

The RWA market reached USD 25,222 million, of which only 3,609 million operate in DeFi.

According to the report, the future of the sector depends on the use of assets and not the volume of issuance.

The DL Research team together with the on-chain analysis platform DefiLlama published the report “The State of RWAfi Q1 2026” on April 23, in which they stated that the market for tokenized real-world assets (RWA) reached $25,222 million, but that only $3,609 million operate within decentralized finance (DeFi) protocols.

According to the analysis, RWA use grew five times in just over a year, going from about USD 4.1 billion at the beginning of 2025 to USD 25.222 million today, while About 86% of all that tokenized capital remains unused within the DeFi ecosystem.

For the authors, the growth of the RWA market does not equate to the effective use of those assets within the DeFi ecosystemsince “a lot of what is called RWAfi today is actually just tokenization. “Placing assets on the blockchain and actually using them are two very different things.”

To measure this gap, DefiLlama uses its own metric called DeFi Active TVL (Total Active Locked Value in DeFi), as seen in the following image:

According to the report, the measurement captures how much of the tokenized capital is actually used within DeFi protocols. Includes collateral on loans, positions in perpetual markets and sources of return.

Why is the gap structural, according to researchers?

He report exposes several factors that explain why tokenized capital does not translate to use in DeFi. One is the lack of active and unified markets to buy and sell those assets.

According to the analysis, The operation is divided between different issuers, chains and platforms. The authors also warn that the portion actually in circulation is usually much smaller than the total supply available on the networks, which makes integration with lending protocols difficult.

Added to this is a structural limitation of the model. DL Research and DeFiLlama maintain that RWA tokens do not eliminate dependency on legal infrastructure and off-chain operations (offchainin English).

Each token represents an underlying right mediated by issuers, custodians, legal entities or external registries. The user does not acquire direct ownership of the physical or financial asset that backs the token, but rather a contract with the structure that issues it.

With these elements, the authors conclude that the next stage of the sector will depend on the effective use of tokenized assets, not the volume of issuance. Under that reading, the 86% gap marks the starting point of the challenge and not a temporary figure.