As the United States Congress heads for a decisive vote on May 14, 2026, the digital asset ecosystem is preparing for a paradigm shift that promises to replace years of legal uncertainty with definitive rules of the game.

Given this imminent approval, the CLARITY Law project must be understood as the mechanism that formalizes the true integration between the traditional and digital financial systems, establishing better foundations for an institutional coexistence that the industry has pursued for years.

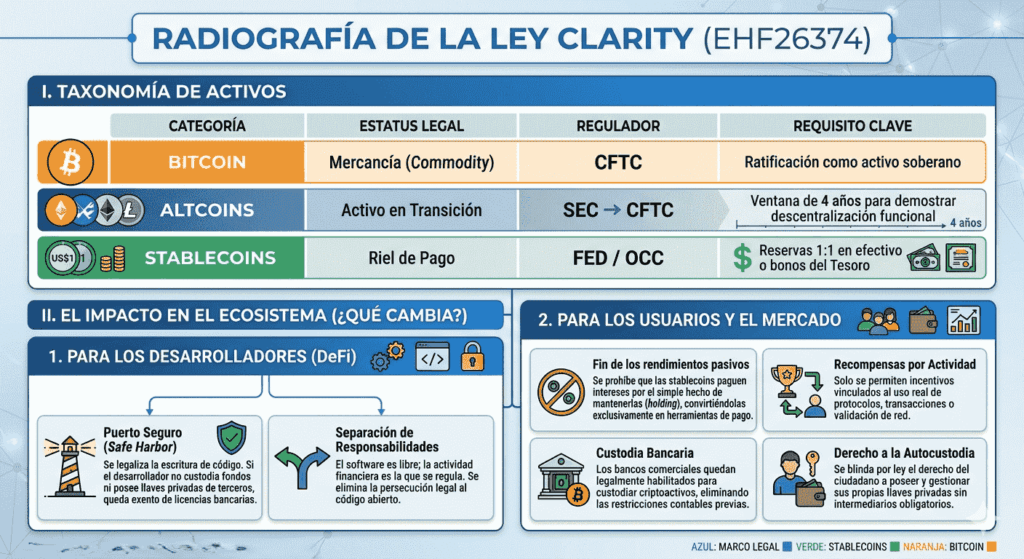

To understand the impact of this lawit is necessary visualize the market divided into three lanes of mandatory circulation. In the first, bitcoin (BTC) is consolidated, formally ratified as a digital product (commodity), which gives it legal protection against traditional securities regulations.

The second lane is occupied by altcoins, which now face a four-year clock to prove that they are autonomous protocols; Otherwise, they will be treated under the rigor of business actions. And finally, stablecoins, which are integrated into the system as payment infrastructures monitored by the Federal Reserve.

This rearrangement addresses a historical conflict such as the criminalization of the codeevidenced in recent cases such as Tornado Cash, where justice questioned whether the development of privacy software was equivalent to facilitating money laundering, as reported by CriptoNoticias at the time.

Now that the CLARITY Act has been approved, through the “Safe Harbor” clause, it will be established that writing decentralized finance (DeFi) software does not constitute a financial activity in itself.

Under the premise that a developer does not guard other people’s funds or possess the private keys of its users, the document considers the code as a free expression and not subject to banking licenses. This distinction protects technological innovation and allows traditional banks to incorporate these tools with solid legal support.

New restrictions for the user and banking

For the common user, the approval of the bill represents an immediate transformation in their digital wallet. This is because stablecoins will stop offering passive returns and become strictly payment and settlement tools.

With this specific measure, regulators aim to prevent capital from draining out of traditional banking, a central concern for institutions such as the American Bankers Association (ABA).

«We want Congress to establish rules for digital assets and create responsible safeguards. The current version still does not adequately prevent companies from offering interest-like rewards,” said Rob Nichols, president of the ABA.

Final integration raises, however, an inevitable tension between privacy and oversight. By formalizing the entry and exit points of capital (on/off ramps), the digital financial system gains the visibility necessary for regulatory compliancealthough this generates resistance in sectors that prioritize transactional anonymity.

Therefore, the industry is preparing for a transition towards formality where bitcoin stands as the untouchable sovereign asset, while the rest of the ecosystem adapts to operate under the standards of the global financial system.

It means that The CLARITY Law marks the end of a stage of technological isolation to give way to a structure where the code and banking finally operate under the same institutional language.