Strategy finances BTC purchases with shares, convertible debt and preferreds.

If the premium in MSTR price disappears, it could face dilution or even selling of bitcoin.

Strategy, the company led by Michael Saylor and the largest corporate holder of bitcoin (BTC) in the world, faces new criticism for the financial model it uses to continue accumulating the digital currency.

Ricardo Fernández, a Chilean analyst and fund manager, who specializes in high-yield corporate debt, published a report in this regard on May 15, 2026.

According to Fernández, the strategy of The company relies on a circular structure based on constant issuance of common stock, convertible debt, and preferred stock to purchase more BTC.

“The essence of the strategy lies in buying BTC with highly overvalued MSTR shares,” he says. According to the specialist, this mechanism can become “a recipe for disaster” if the market stops valuing Strategy at a high premium over its net asset value.

That net asset value, known in the market as mNAV, compares Strategy’s market capitalization to the estimated net value of its BTC holdings net of debt.

At the moment, Strategy maintains 843,738 bitcoin, valued at about $65,429 millionaccording to data from the company itself. Its mNAV multiple sits near 1.28, implying that the market values MSTR approximately 30% above the estimated net value of its BTC reserves.

According to Fernández, that premium is the centerpiece of the model. “MSTR’s financing model only outperforms BTC if the shares are trading at a significant premium to their net asset value,” he notes.

However, it is worth clarifying that in the past the mNAV has fallen below 1.00 and the company continued buying BTC, which keeps the debate open about to what extent the model can be sustained if that premium continues to fall.

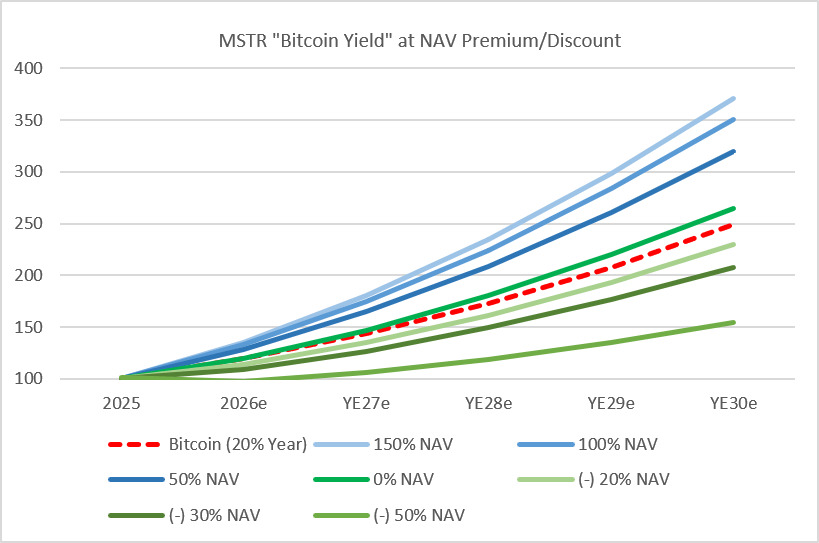

The following graph shows precisely that relationship. There you can see how the so-called “Bitcoin YieldStrategy’s (ability to increase bitcoin per share) depends directly on how much premium MSTR maintains over its mNAV. In the scenario where the premium disappears or becomes negative, Expected performance begins to deteriorate rapidly.

As seen, the dotted red line represents a scenario where bitcoin rises 20% annually in a sustained manner. From there, The author projects different scenarios for MSTR depending on how much premium the stock maintains over its net BTC reserves.

The blue lines represent optimistic scenarios where MSTR is trading between 50% and 150% above its NAV. In those cases, Strategy manages to vastly outperform BTC thanks to its ability to issue overvalued shares to purchase more BTC.

On the other hand, the green lines show scenarios where that premium disappears or becomes a discount. There MSTR’s performance begins to deteriorate rapidly and even falls below BTC. “Mr. Saylor wants to double the value of BTC per share in seven years,” explains Fernández. However, he adds that this “cannot be achieved unless MSTR is trading 150% above its net asset value.”

The report maintains that the scheme works as a “circular reference”: the company buys more BTC because the market assigns it a valuation higher than the value of its reserves; and, at the same time, that accumulation of BTC helps sustain the bullish perception on the stock.

The growing weight of debt and preferred securities

Fernández also warns about the growth of Strategy’s financial obligations. Currently, the company maintains more than $8.2 billion in debt and about $13.5 billion in issued preferred stock. These preferred instruments include series such as STRF, STRK, STRD and STRC.

Preferred shares function as a kind of hybrid between debt and traditional shares and They grant collection priority over common shareholders and pay high dividends, ranging from 8% to 12% annually.

According to recent company data, the payments associated with these preferred They already represent around 1,488 million dollars annually in dividends.

Fernández considers that this is where one of the main risks of the model appears. “The 10% dividend on preferred stock and convertible debt obligations forces continued dilution or sale of BTC, undermining long-term value for shareholders,” the report maintains.

In other words, if Strategy loses the ability to continue financing itself through new issues, it will eventually it could be forced to issue more common stock, take on more debt, or even sell some of its BTC to cover financial obligations.

That scenario is no longer purely theoretical. During the quarterly results presentation on May 5, Saylor commented the firm evaluating using part of its BTC reserves to finance dividends related to STRC, one of the preferred instruments issued by the company.

Although the company continues to have access to the capital market and still retains a dominant position within the corporate BTC ecosystem, the report warns that The scheme depends on external financing continuing to flow.

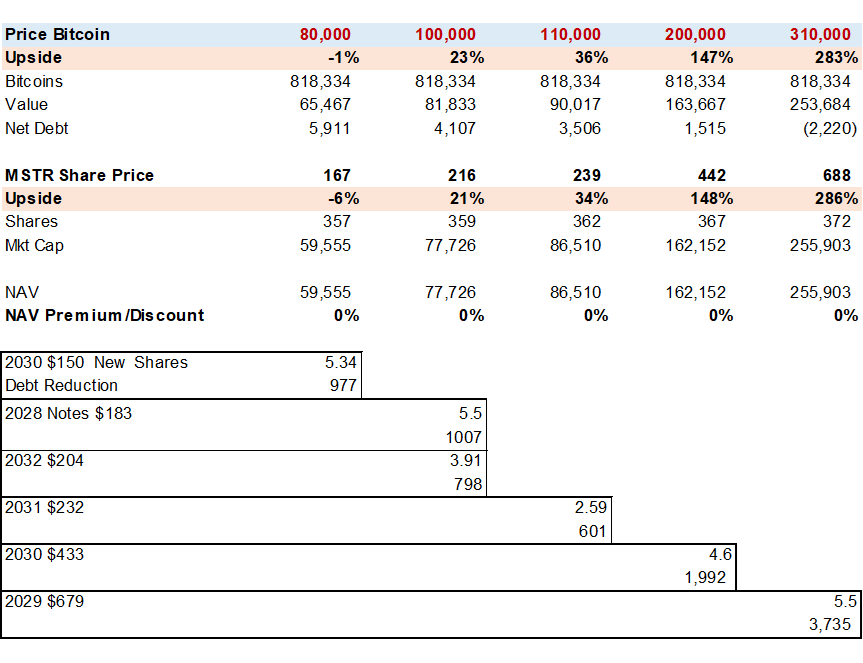

To support his thesis, Fernández shares a table that projects different scenarios for Strategy depending on the future price of the currency created by Satoshi Nakamoto:

What Fernández does is compare how much BTC would rise against the potential performance of MSTR under a scenario where the stock is trading without a premium over the NAV, that is, at the same value of its net reserves.

The analysis is based on different hypothetical prices for bitcoin, from 80,000 to 310,000 dollars. From there, calculates how much Strategy’s BTC reserves would be worth, how its net debt would evolve, and what the theoretical price of MSTR would be.

One of the most important points appears at the bottom of the graph: It details Strategy’s various convertible debt issues and the prices at which the bonds could be transformed into shares.

For example, convertible debt due 2029 requires MSTR to reach approximately $679 per share to be fully converted to equity. Other issues require prices higher than 433, 232 or 204 dollars.

According to the analyst, this shows that much of Strategy’s financial structure depends on BTC continue to rise significantly and that MSTR maintains high valuations on the stock market.

If that doesn’t happen, the company could face more costly refinancings, further dilution, or pressure on its BTC reserves.

The comparison with a Ponzi-type “loop”

The criticism recalls similar analyzes previously carried out by Jacob King, a financial analyst who compared the Strategy model with a mechanism that constantly feeds back.

As reported by CriptoNoticias, King maintains that the cycle begins when a company issues debt or shares to acquire BTC. This purchase helps reduce the available supply of BTC and favors price increases, which increases the company’s market capitalization and attracts new investors. This new capital allows the process to be restarted again.

According to King, the risk appears if bitcoin goes through a severe and prolonged decline. In that scenario, Companies could lose access to financing while maintaining balance sheets highly exposed to BTC.

Although King himself acknowledges that an extreme collapse remains unlikely, the debate gained steam because other companies that tried to replicate the model ended up facing financial problems.

On May 5, 2026, CriptoNoticias dedicated a publication to Sequans Communications, a French company that adopted BTC as a treasury asset in 2025, explicitly following the approach promoted by Michael Saylor.

However, The company ended up selling more than 2,000 BTC after the deterioration of its financial situation. Sequans went from accumulating 3,234 BTC to holding only 1,114 BTC. The company reported losses of $50 million in the first quarter of 2026including accounting impairment of BTC and realized losses from actual sales. In addition, about 73% of the remaining BTC were collateralized as collateral for convertible debt.

The case showed an important difference from Strategy: while MSTR still retains broad access to the capital market, companies with weaker operating businesses may be forced to sell BTC to cover liquidity or debt needs.

“I see no reason to own MSTR shares,” says Fernández

Fernández’s conclusion is clear: “I see no reason to own MSTR.” For him, if an investor “has a positive outlook on BTC, they should buy it” before expose yourself to risks associated with debt, dividends, refinancing and potential share dilution.

Yet Michael Saylor’s defenders argue exactly the opposite. For them, Strategy represents a new financial tool capable of amplifying corporate exposure to bitcoin using traditional capital markets.

For example, the Venezuelan influencer David Battaglia, commented recently: “I feel like I don’t have enough MSTR in my portfolio”

And Saylor continues his constant accumulation narrative (even admitting that they may make some bitcoin sales). “You don’t want to be a net seller of BTC because it’s capital. You want to end each year with more BTC than you started with,” Saylor said.

The difference between both positions is in how leverage is interpreted. For Fernández, the structure adds financial risks that do not exist when purchasing BTC directly. For Saylor and his defenders, however, This financing allows increasing BTC per share and turning Strategy into a corporate accumulation vehicle.

And that is the bottom line: whether Strategy built an innovative financial model or whether, as Fernández warns, it depends too much on the market remaining willing to pay a high premium on its BTC reserves.