For thousands of cryptocurrency users in Spain, the routine of buying or selling bitcoin (BTC) and cryptocurrencies through their usual applications is about to be transformed. That is because on July 1, 2026, the transitional regime of the Regulation on the Cryptoasset Market (MiCA) formally expires, closing the eighteen-month window that allowed companies to operate under the prior registration of the Bank of Spain.

As of that date, any cryptoasset service provider (CASP) that lacks the express authorization of the National Securities Market Commission (CNMV), or a valid European passport, must immediately suspend its activity in the country.

This rule change exposes an operational paradox for a technology of a decentralized nature. While the protocol of the decentralized Bitcoin network remains intact and outside the scope of state guidelines, the access and exit points of money, i.e. The gateways that connect cryptocurrencies with the euro are fully integrated into the traditional financial perimeter.

Therefore, whoever decides to trade with fiat money within the legal commercial framework must submit to the same supervision and compliance standards that apply to banking entities.

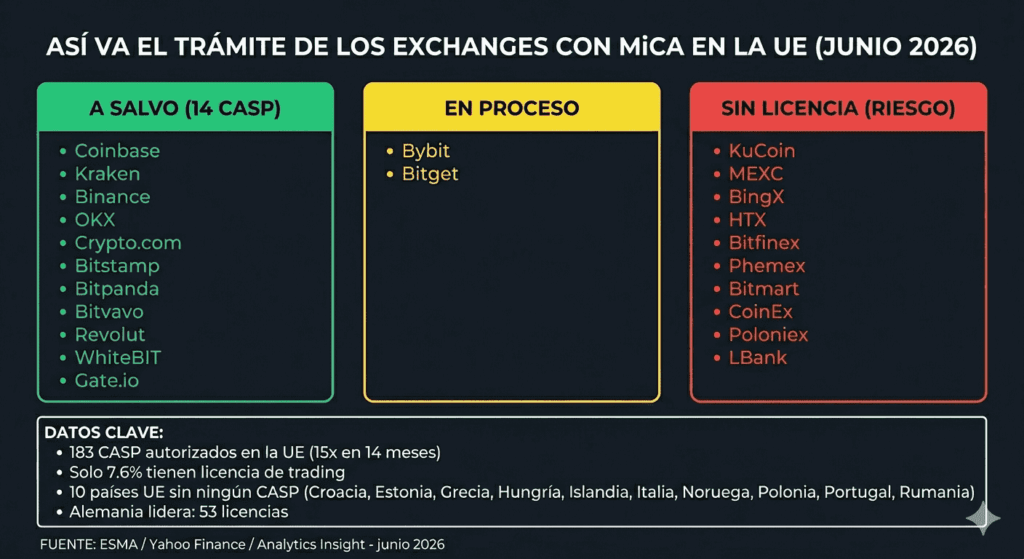

Why do 10% of cryptoasset exchanges survive MICA?

The transition to this new regulatory environment has caused a drastic contraction in the number of authorized actors on the continent. Richard Fetyko, CEO of the analysis firm altFINS, highlights the magnitude of this process institutional when reviewing data from the European bloc.

In this regard, according to CriptoNoticias reports, the issuer of the largest stablecoin in the world, Tether (USDT), chose not to validate this state design immediately. Paolo Ardoino himself, CEO of Tether, repeatedly warned that the requirements imposed by Europe are extremely “uphill.”

Ardoino pointed out that the obligation to maintain 60% of reserves in bank deposits not only limits operation, but also introduces systemic risks to the funds themselves, which caused the main regulated platforms in the region to begin applying operational restrictions on this asset, USDT.

The figure of 183 CASP includes entities with different levels of authorization. Only 14 of them have a Class 3 license (150,000 euros of capital), which is what allows an exchange to operate with custody of client funds, the usual model for trading platforms. The remainder have Class 1 or 2 licenses, which cover non-custodial advisory, brokerage or trading services.

Behind this massive withdrawal there is an economic and bureaucratic barrier that is insurmountable for most operators. This is because obtaining a MiCA license from scratch for a startup requires an initial outlay of between 50,000 and 100,000 euros just to start the processing process, as Fetyko pointed out.

Once achieved, maintain an average structure adapted to Regulatory requirements represent a recurring cost of between 500,000 and two million euros annually.

Added to this is that the risk of operating outside this financial funnel is punitive. Fines for ignoring deadlines can reach five million euros or 12.5% of the company’s global revenue. In fact, the rigidity of the legal framework has already had its first practical consequences before its full application, accumulating more than 540 million euros in sanctions in the regionaccording to reports.

«Before MiCA, more than 3,000 cryptocurrency companies were registered and operating throughout the European Union. Today? Only between 170 and 210 have a full MiCA license. “That’s less than one in ten surviving the transition.”

Richard Fetyko.

Additionally, the regulation has faced harsh criticism within the sector for favoring corporate centralization that contradicts the original nature of the technology. Voices from the industry such as , CEO of Fideum, MEP Marcin Sypniewski and Rowan Varrallspeaker at the Digital Assets Forum (DAF3), warned that high compliance burdens are unaffordable for emerging companies.

This high-cost ecosystem, they say, is forcing a consolidation of the market where Large financial institutions and transnational exchanges will end up monopolizing the sector. The collateral risk of this regulatory funnel is regulatory exodus; Plotnikova herself and Przemysław Kral, CEO of Zonda Crypto, point out that there is a real danger that technology firms will abandon European soil to relocate to jurisdictions with much more dynamic and attractive frameworks, such as the Middle East.

The jump from banking to the cryptocurrency custody business

This pressure on the digital native ecosystem coincides with the complex scenario that international platforms face to regularize their situation. While global brands such as Binance, Bitget, MEXC or BingX assume this situation to adapt to the new standard in Spain, traditional banking has accelerated its strategic positioning.

Entities like BBVA, CaixaBank, Cecabank and Openbank they deployed buying and selling services and custody of digital assets directly in their commercial infrastructures.

Behind this deployment there is an infrastructure logic. This is because under the new regulations, secure custody and asset segregation of funds are the mandatory technical pillars for any other derived service.

“The banks that reach institutional custody first are the ones that can build the rest of the offer,” explained in an email sent to CriptoNoticias, Mike Schwitalla, director of Crypto Finance, a firm that provides infrastructure support to these institutions.

«What we are seeing in Spain is exactly what happens in all markets that mature in digital assets: the banks that reach institutional custody first are the ones that can build the rest of the offer. Custody is not the least relevant part of the crypto business for a bank; I see that it is the most relevant, because without it no other service is possible. In Spain this is already understood by the first to have obtained the MiCA license. The question now is what others will do before the transitional period closes.

Mike Schwitalla.

This assimilation to the banking model introduces a critical guarantee such as the mandatory separation of accounts. From now on, The law prohibits exchanges from mixing customer money with the company’s operating capitalapplying the same protection system as traditional banking. In this way, if the provider becomes insolvent, the digital assets are protected and continue to belong, by law, to those who purchased them.

For this reason, analysts consider that the expiration of the deadline does not constitute a mere compliance procedure, but a market consolidation event. Isabella Chase, policy manager for the EMEA region at TRM Labs, points out that the departure of unregulated competitors will reconfigure the scenario in favor of firms that anticipated regulatory investments:

«For already authorized platforms, this represents a moment of market structure. “If a definitive number of unlicensed competitors are forced to leave, competitive dynamics change and companies that invested in compliance infrastructure early are about to see the value of that investment reflected.”

Isabella Chase.

Zero tolerance for unregulated cryptocurrency companies

The room to adapt, therefore, is non-existent. It is seen in the fact that the European Securities and Markets Authority (ESMA) reiterated that no extensions or additional grace periods will be granted for unauthorized entities that continue to provide services to clients in the European Union.

At the local level, The CNMV will also maintain strict surveillance over the promotion of these services.warning that advertising from unregistered platforms will lead to serious administrative sanctions for intermediaries and content creators.

In that sense, for investors in Spain, the adaptation margin ends before June 30. The practical implication of the standard forces users to make a definitive decision about their capital: either they migrate their funds to platforms authorized under the new European standard, accepting the traceability and loss of control of their private keys, in exchange for legal security, or they assume self-custody of their digital assets.

This last route becomes the only viable path if the investor’s priority is to preserve the anonymity and peer-to-peer nature of their transactions, even if this means assuming all technical responsibility for their funds alone. The regulatory framework seeks to mitigate the risks of the retail investor, but the cost of that protection is the total assimilation of intermediaries into the traditional financial surveillance system.