Users choose stablecoins to avoid the constant failures of local banking.

Retail adoption is advancing rapidly despite the lack of a regulatory framework in the country.

Keeping savings under the mattress or buying foreign currency at a physical exchange house have been, for decades, the classic economic survival mechanisms in Latin America. However, in Colombia, that historical need for refuge has shed its skin. Citizens now prefer to resolve their daily lives with stablecoins such as Tether (USDT) and USD Coin (Circle) built in a system parallel to the banking system.

The most recent data of the State of Stablecoins in Latin America report by Rain reveal a much more pragmatic reality in Colombia. Citizens are simply looking for an efficient way to manage the fruits of their daily work.

To understand the magnitude of this phenomenon, just look at what happens on centralized cryptocurrency exchanges. There, 99% of the Colombian pesos that enter these systems are immediately converted into stablecoins, mainly USDT and USDC.

This behavior works like a voluntary entry toll. Even in periods where the Colombian peso shows exchange strength, user preference leans towards the stability of a global reserve currency. The peso enters the ecosystem, but is transformed into a crypto asset, which is used as a digital dollar, almost instantly to guarantee long-term liquidity.

Behind this structural behavior, there are three key factors that explain why Colombia is consolidating itself as the fifth country with the largest volume of digital assets in the region.

Stablecoins are used daily in Colombia

This migration of the Colombian peso to stablecoins responds to structural needs that the traditional banking system has not been able to resolve with the same agility.

1.-The search for predictability and refuge

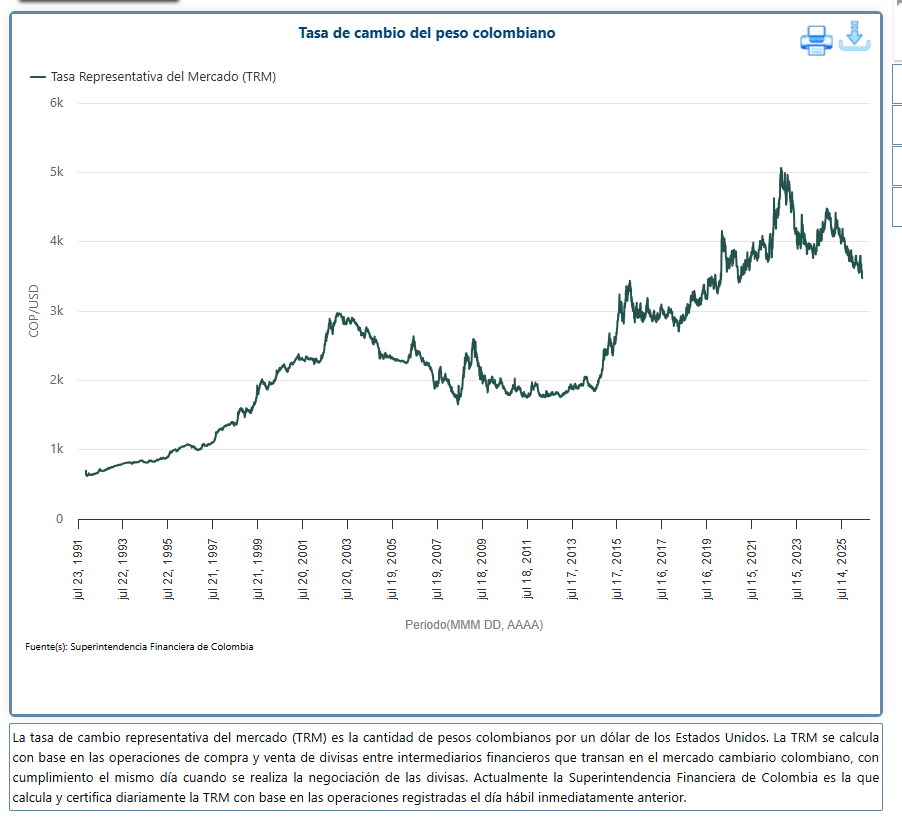

Although the Colombian peso has registered a revaluation close to 4% against the dollar During the last year, citizens’ economic memory and the search for long-term predictability dictate other behavior.

For the ordinary saver, this mechanism translates into a proactive alternative to local inflation, which It stood at 4.4% year-on-year at the end of the first quarter of 2026. By acquiring these stablecoins, people have access to a global financial safeguard without having to go through the complex bureaucratic procedures or strict income requirements that traditional entities require to open an account in foreign currencies.

This migration to the digital dollar does not mean that the user is completely exempt from the loss of purchasing power, as the US economy is also experiencing its own price inflation.

However, the retail saver assumes this exchange because historically it is a much smaller and more predictable devaluation, whose long-term technical objective is around 2% per year, offering stability that the local currency has not been able to consolidate structurally.

2.-An alternative to the failures of traditional banking

The second factor responds to a need for operational contingency. The frequency with which traditional banking platforms fail in the country has driven the use of stablecoins as an alternative and uninterrupted transactional channel, available 24 hours a day.

This same fluidity benefits a growing group of remote workers and freelancers, who avoid multi-day waits for international fiat money transfers and unfavorable exchange rates imposed by local banking entities.

3.-The optimization of remittances

The third trigger is the profound impact on the remittance sector, a channel that moves nearly 10 billion dollars annually in the country. Traditionally, sending money from abroad meant losing between 5% and 7% in commissions from traditional intermediaries and agencies.

With the use of USDT or USDC, these transaction costs are reduced to minimal fractions and the funds are settled in a matter of minutes, transforming the economy of the receiving families.

The adoption of stablecoins in Latin America is structural, not speculative. Stablecoins are solving concrete problems, including preserving purchasing power in high-inflation economies, reducing the cost and latency of cross-border payments, and giving individuals and businesses convenient access to US dollars.

Rain report on the state of stablecoins in Latin America.

Lack of regulation and operational alerts

Meanwhile, Colombia ranks 22nd in digital asset adoption globally, but lacks a consolidated regulatory framework. The lack of rules generates uncertainty for companies and users.

Julián Colombo, director of Public Affairs for Latin America at Bitso, stated in the past that the lack of regulation prevented cryptoassets from being brought closer to a more massive and corporate public, which needs clear rules. However, in the country adoption is now flowing unchecked.

As CriptoNoticias recently reported, the Government of Gustavo Petro was moving forward with a bill to regulate the sector. But currently expectations are focused on defining who will be the president who will provide answers to an industry that has been betting on a clear framework for digital assets.

Another fact that has generated concern in Colombia is the parallel increase in illicit activity. Global reports indicate that the volume of transactions with illicit cryptocurrencies reached USD 158 billion in 2025, 145% more than in 2024, and that stablecoins represent almost 95% of flows to sanctioned entities.

In Colombia, networks linked to the Sinaloa Cartel and Chinese money laundering organizations have been documented. All these signs that the growth of this parallel payments market is not without warnings.

For monetary authorities and local regulators, the outlook poses a direct dilemma. The trend indicates that the adoption of these tools will hardly recede as long as the operational frictions and costs of the traditional system persist.

Therefore, under the rigor of the current landscape, the regulatory debate can no longer focus solely on the warning about volatile assets, but on how to address a digital financial infrastructure that thousands of citizens have already integrated into their daily economy.