For decades, the channels for sending money across Latin American borders have operated under the same script: processes that take days and corporate commissions that bite into pockets. However, this scenario of financial friction is changing as conventional banks discover that they can no longer ignore the digital asset ecosystem if they want to retain their customers.

Pressured by a silent migration of users towards the digital asset environment, several of the main financial institutions in the region began to integrate stablecoins into their operating systems, transforming these assets into base infrastructure for everyday money.

Unlike previous technological cycles, this change is not being planned from macroeconomic offices, but is driven from the bottom up by the needs of the population.

As explained by the digital infrastructure firm BitGo, in a report shared with CriptoNoticias, the true driving force of this movement is “everyday crypto”, that is, the use of assets to solve real-world problems.

The most critical example is coverage against devaluation: according to sector reports, Argentina reached an adoption rate of almost 20% in 2025, with some 8.6 million residents using these instruments as a refuge from triple-digit inflation.

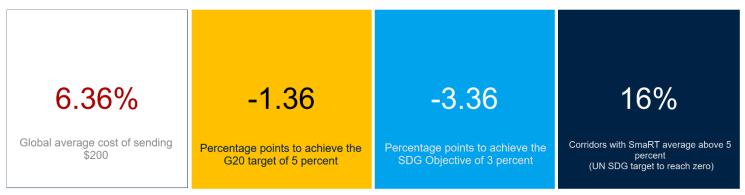

The other great catalyst is the remittance market, a flow that exceeded 160 billion dollars in 2024 and touched 174 billion dollars in 2025. To avoid traditional fees, which according to the World Bankusually exceed 5% or 6% in the region, a growing portion of these funds is moving towards digital alternatives.

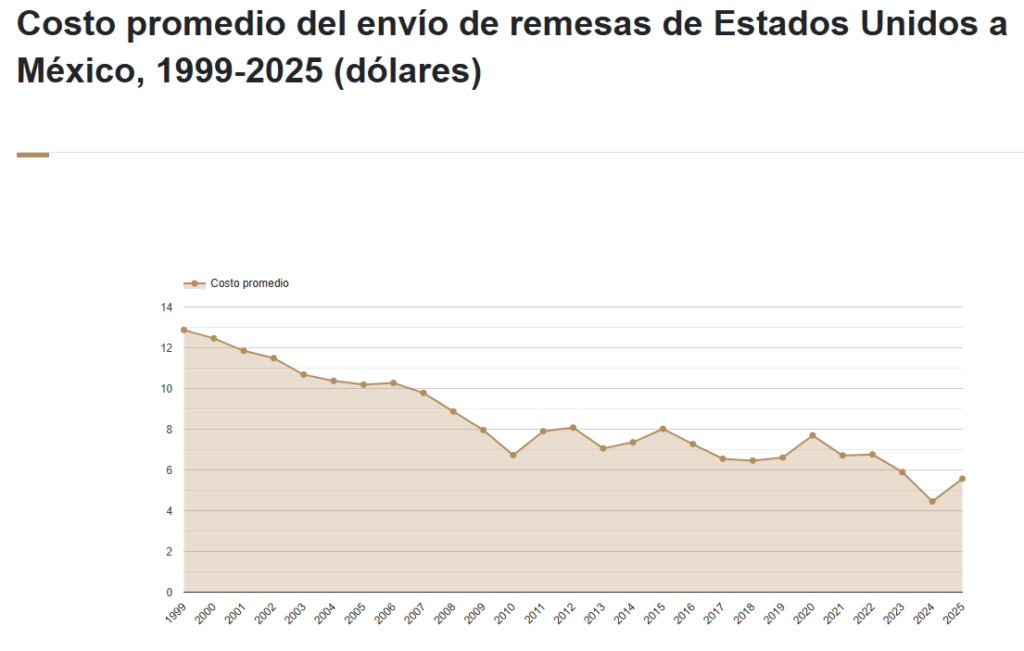

The phenomenon is evident in key corridors such as the one from the United States to Mexico, where despite a historical downward trend in traditional rates, average costs rose again towards $5.5 in 2025, putting pressure on users to look for cheaper options in the bitcoin (BTC) and cryptocurrency environment. This migration of capital has reached a critical mass that forces traditional banks to react to avoid commercial obsolescence.

A silent update of Latin American banking with stablecoins

It is this potential market loss that has led entities of the scale of Banco Santander Brasil, Banco de Crédito del Perú (BCP), BCP of Bolivia, Towerbank in Panama, Caja de Valores in Argentina and the B3 stock market to integrate digital assets into their balance sheets.

The phenomenon is repeated in Mexico, where The Anchorage Digital firm sealed an alliance with the Salinas Groupcontrolled by Ricardo Salinas Pliego, designed for Banco Azteca and other companies in the conglomerate to process cross-border payments using stablecoins.

To channel this millionaire flow, Financial institutions have had to update their own computer engineeringmigrating from analog messaging networks towards an immediate settlement model.

In the conventional system, coordinated by networks such as SWIFT, one bank is limited to sending an electronic message to notify another that the money must be moved, a process that usually takes 48 hours.

In contrast, the integration of stablecoins through programming interfaces (API) allows the exchange to occur directly on the digital asset. This opens the door to “atomic payments”, a technical advance that ensures that the sending and final receipt of money are executed simultaneously, eliminating intermediaries and waiting times.

This operational speed is reconfiguring the perception of risk in the boardrooms of regional financial centers, where cryptoassets have gone from being seen as a threat to consolidating themselves as a strategic ally.

“In recent quarters, banks have begun to recognize cryptocurrencies as an essential improvement to their core infrastructure,” explains Luis Ayala, CEO and head of Latin America at BitGo, according to their report.

The key to this corporate trust lies in the fact that the technological transition is no longer carried out clandestinely, but under the protection of regulated American suppliers; BitGo itself has a national trust charter from the US Office of the Comptroller of the Currency (OCC).

However, the support of international custodians does not exempt this technology from face serious resistance from supervisors local. While proponents of tokenization highlight that stablecoins significantly reduce transaction costs and promote financial inclusionseveral central banks in the region maintain a cautious stance in the face of systemic risks and difficulties in detecting money laundering in high-speed transactions.

Likewise, although the fear of volatility has been reduced thanks to the peg of these currencies with the dollar, the main concern remains the possible loss of control over national monetary policy, a factor that has been highlighted in reports from the International Monetary Fund (IMF).

This efficiency race is no longer exclusive to banking and forces traditional postal operators to react. The clearest example is the recent launch of USDPT, the official Western Union stablecoin issued on the Solana network and backed by Anchorage Digital Bank.

With this movement, the firm seeks to optimize its own profit margins by moving capital in seconds between its agencies, skipping the times of traditional banking.

The migrant’s pocket will decide between banking and bitcoin

This new scenario places the Latin American migrant at a practical crossroads about how to move their heritage. On the one hand, you can opt for the institutional model of regional banks and firms like Western Union, which offer convenience, integrated accounts and legal support in exchange for accepting strict financial oversight.

On the other hand, it maintains the autonomy of open options such as bitcoin, Tether (USDT) or Circle’s USDC. With these assets it is possible to have greater resistance to censorship depending on how they are handled, although they transfer all technical and conversion responsibility to the citizen.

The evolution of the sector in Latin America no longer depends on convincing institutions to participate, but on seeing how the user will react. At the end of the day, Actual adoption in remittance corridors will be measured under a purely pragmatic logic.

It will be where the migrant will choose the option that manages to translate the speed of the blockchain into a real reduction in costs in their shipments, deciding whether the support of traditional brands compensates for the loss of financial sovereignty of the original digital ecosystem.

At the end of the day, actual adoption in remittance corridors will be measured under purely practical logic. The migrant is not interested in technical debates, but in his own pocket.

Therefore, you will choose the option that charges you the least fees for sending your money. The final decision will depend on whether families prefer the comfort and support of the usual brands.or if they are willing to learn how to use independent creptoactive apps in exchange for maintaining full control and privacy of their funds.