The alliance seeks to neutralize the imminent deregulation of digital assets in Congress.

The new tokens will operate under institutional control, excluding the use of private keys.

After years of looking askance and even disparaging Bitcoin technology, the four Wall Street giants, JPMorgan Chase, Bank of America, Citigroup and Wells Fargo, decided to put aside their fierce competition to form an unusual digital alliance.

Their plan is ambitious since they plan to develop a joint network of “tokenized deposits” that converts money from checking accounts into digital tokens capable of moving in real time, 24 hours a day and 365 days a year.

Behind this technical display, provisionally baptized as The Bridge or The Chain, according to the report from The Wall Street Journal, There is no sudden love of innovation, but a calculated survival instinct.

Why is Wall Street launching tokenized deposits?

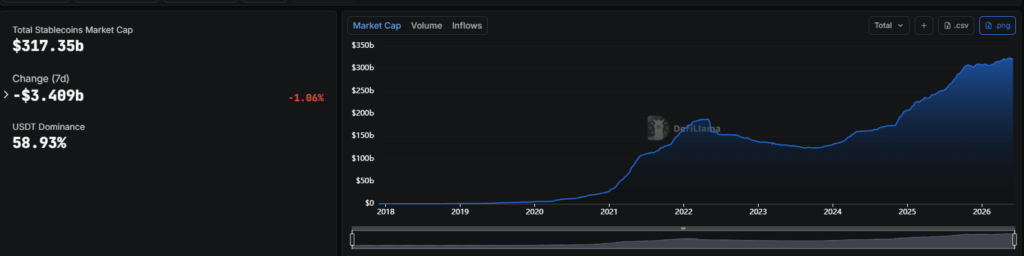

During the last year, issuers of Stablecoins like Tether (USDT) or Circle (USDC) have become global financial highwaysabsorbing billions of dollars in cross-border payments and corporate fund managementas CriptoNoticias has previously reported.

The urgency for megabanks intensified with a bill in the United States Congress that seeks to allow that stablecoins pay interest to their usersan advance promoted under the deregulation stance towards virtual assets of the Donald Trump administration.

For Wall Street, the fact that the stablecoin sector begins to pay interest represents a direct threat to its waterline by attracting deposits. If a multinational can move its capital in seconds on a Sunday night without going through a bank locker and, in addition, obtain attractive returns, The traditional banking model is creaking.

The strategy of these entities is to adopt the operational characteristics of block technology, such as immediate settlement and automation through smart contracts, but applied to their own balance sheets.

By channeling the project through the operating company The Clearing House (TCH), the resulting tokens do not represent an external liability like stablecoins, but rather formal bank deposits that remain within the traditional regulatory framework and under the direct custody of the participating institutions.

Traditional banking versus stablecoins: speed or control?

Precisely that is the argument of the banks defending the project. They point out that tokenized deposits combine stablecoin speed with regulatory security. Shamir Kalik, Citigroup’s chief services officer, said the network will serve to “further consolidate the dominant role of banks in finance and capital markets.”

The analyst Alfredo Muñoz García opened the debate on professional networks such as LinkedIn, about the difference between bank stablecoins and deposits tokenized. In the comments of your posts, Some users question whether the bank is “trying to ‘disguise’ the long-standing model.” with blockchain technology to avoid losing control.

Others wonder if the project represents “a true evolution of money or simply a desperate attempt” by traditional entities.

Meanwhile, the project is currently in the design phase and the alliance of megabanks plans to expand the network to entities throughout the United States by the first half of 2027. Although executives such as Marc Monaco, from Bank of America, admit that “corporate clients are not yet asking for tokenized deposits,” Wall Street has decided to get ahead of itself to ensure control of the market.

As this infrastructure advances, A custody war will probably break out in the financial sector. If the fiat money system is successfully digitized, state pressure to stifle independent and decentralized alternatives will increase dramatically, forcing the average citizen to choose between the comfort of banking tutelage or the freedom of real mathematical scarcity.