Solana eliminates the wait, but formal registration excludes the undocumented.

Bank support implies giving up resistance to censorship of open networks.

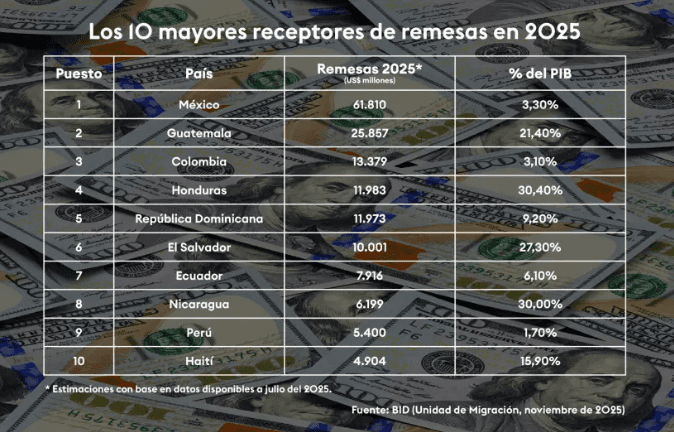

Sending remittances from the United States to Latin America has traditionally depended on correspondent banking systems that take between one and three days to settle and that expose the recipient to exchange fluctuations. However, now Western Union claims that its USDPT stablecoin, issued on Solana, allows settlements in seconds.

Currently, the asset has moved from the technical phase to regional execution, operating as an efficient settlement rail in strategic corridors such as the Philippines and Bolivia, the latter selected for its complex foreign exchange access situation.

For a region that represents a substantial part of the company’s global revenue, this technological leap, reported by CriptoNoticias, is a strategy to recover lost ground compared to digital alternatives that already offer immediacy. Among them are stablecoins widely adopted in the region, such as (Tether) USDT and USD Coin (Circle).

Unlike the native stablecoins of the digital asset ecosystem, the deployment of USDPT does not seek, in the first instance, mass adoption in independent digital wallets, but rather a silent transformation of Western Union’s internal architecture.

For example, the asset currently operates as an efficient settlement rail in specific corridors, allowing the firm to move value between its headquarters and local agents without depending on correspondent banking times. For the user at the window, the change is almost invisible because the Solana network It acts as the hidden engine that ensures that capital is available for physical withdrawal almost instantly.

Western Union seeks to reduce traditional remittance costs through USDPT over Solana. The model eliminates several intermediaries from the correspondent banking system, which according to the company allows it to offer transfers at a lower cost than the market average, which ranges between 3% and 6%.

However, this operation remains within a “walled garden.” Although the asset already runs on the Solana network and is supported by Anchorage Digital Bank, its use is restricted to the company’s infrastructure, which marks a fundamental difference with the free market of USDT or USDC.

In the end, Western Union does not seem to compete for total user autonomy, but for use code efficiency to optimize your own liquidity and profit margins, maintaining institutional control over each link in the payment chain.

This integration between the stablecoin ecosystem and the traditional Western Union infrastructure generates several specific advantages and disadvantages, detailed below:

Advantages of USDPT for the Latin American migrant

1.-Settlement speed

The implementation of USDPT on the Solana network allows Western Union to execute liquidity almost immediately between the company and its local agents, eliminating the days of waiting imposed by the traditional correspondent banking system from the equation. This immediacy optimizes the firm’s internal liquidity and guarantees that the migrant’s capital is no longer “in transit” and subject to exchange volatility.

2.-Simple physical cash-out

This ‘invisible engineering’ translates into tangible benefits for those who send and receive. This is because it solves the conversion gap that native cryptocurrencies have not yet mastered for the general public. Unlike a digital asset that requires the user to learn how to use an exchange or find someone on a P2P marketplace to exchange it for local currency, here the agency network does all the work.

A migrant, for example, send money from New York using USDPT infrastructure. In a matter of seconds, the capital arrives digitally at an office in La Paz or Santa Cruz (Bolivia). The recipient simply goes to the Western Union window with their identification and receives cash in hand, just as they have always done, but without the 48-hour waits that the traditional banking system previously imposed.

3.-Greater protection

Unlike the technical irreversibility of public networks, this architecture allows assets to be recovered in the event of fraud or errors. It is a model that prioritizes consumer protection and federal oversight over the technical autonomy of the cryptocurrency ecosystem.

The cost of regulation: disadvantages and structural limitations

However, moving to a system regulated under the GENIUS law implies accepting structural limitations that affect user sovereignty. In contrast to the advantages:

1.-Centralization and financial surveillance

under the regulated model of bank issuance, Anchorage Digital Bank NA retains the technical authority to freeze or intervene balances in response to judicial or regulatory requirements. This capability, inherent to assets issued by supervised entities in the United States, eliminates the censorship resistance that characterizes purely decentralized protocols.

2.-Access barriers (KYC)

Strict identification requirements exclude the undocumented population or those who prioritize privacy, limiting the real scope of the promised financial inclusion.

3.-Technical limitations and dependence on the physical network

At this stage, USDPT lacks interoperability with Decentralized Finance (DeFi) protocols, leaving the balance trapped in the firm’s ecosystem. In addition, it remains to be seen whether Solana’s efficiency will translate into lower commissions or if it will only serve to widen the company’s margins.

Meanwhile, in the user communities in Latin America, positive opinionswhere many highlight the combination of speed that blockchains allow with reliability and ease of cash withdrawal through the Western Union agency network.

They believe that USDPT represents a safer and more accessible option for families who prioritize stability and institutional protection over total decentralization. However, in cryptocurrency forums on X and .

Some critics argue that Western Union’s stablecoin is a defensive response by the company, that its final fees will likely not be competitive against USDT on Tron, and that it implies a greater loss of privacy and financial control for the user.

In that sense, the launch of USDPT places the Latin American migrant before a choice where on the one hand it has institutional security, regulated support and the ease of physical withdrawal. On the other hand, it has the lowest regulatory friction and greatest autonomy offered by stablecoins such as USDT and USDC.

Therefore, actual adoption of USDPT will ultimately depend on whether Western Union is able to translate its operational improvements into a tangible cost reduction for the end user, and whether that greater institutional protection compensates for the additional loss of privacy that its model entails.