In this cycle, retail investor euphoria is absent and there is little ETF capital inflow.

Strategy adds growing systemic risk to the price of bitcoin.

The bitcoin (BTC) market is undergoing a structural transformation in 2026 compared to previous years. Gone are the traditional explanations for mass adoption or the impact of exchange-traded funds (ETFs) to support price increases.

According to the most recent report from the financial analysis firm 10x Research, published on May 17, 2026, the recent behavior of the price of bitcoin responds almost exclusively to a centralized and predictable corporate dynamic.

The firm clearly warns in its report: “A single engine has driven the bitcoin rally until 2026. It operates monthly, belongs to a single entity and represents 70% of every dollar that has entered bitcoin this year.” Under this scenario, analysts maintain that “if you have been trading bitcoin based on macroeconomic catalysts, statements from the Federal Reserve or news about ETFs, you have been watching the wrong clock.”

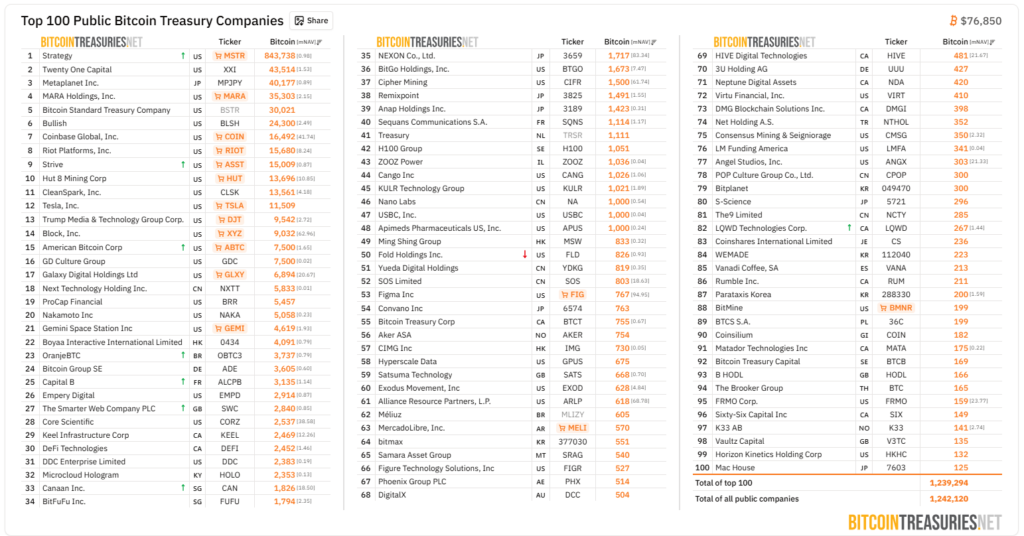

And what is that “single engine”? As the title of this publication suggests, it is about Strategy (formerly called “MicroStrategy”), the company founded and led by Michael Saylor that has become the largest corporate holder of bitcoin.

This extreme concentration of demand translates directly into capital flow balances. The report details that, “taking into account flows through stablecoins, ETFs and futures, Strategy represents $11.4 billion of the $16 billion that has entered bitcoin so far this year, 70% of the total.”

Such a capital injection, if analyzed on an annualized basis, is equivalent to $31 billion or the acquisition of 382,000 BTC per year. This gives an average daily purchase rate of 85 million dollars, a figure that doubles the total daily production of bitcoin miningwhich generates only 450 BTC per day, equivalent to about 36 million dollars.

There was a change of players in bitcoin

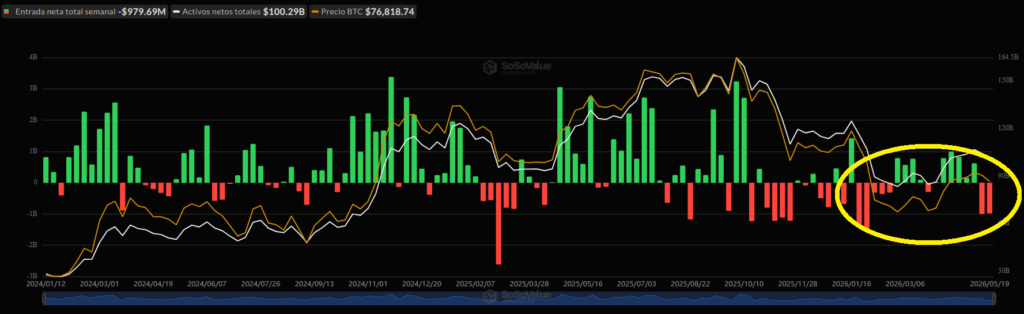

In this cycle—according to data managed by 10x Research—the euphoria of retail investors and ETF capital inflows are absent. The research firm states that accumulated inflows into bitcoin ETFs stand at just $2.8 billion so far this year, far below the $6.1 billion recorded in the same period of the previous year and the $12 billion expected for the same date in 2024.

Annualizing the current ETF projections points to a total flow of 7.6 billion dollars, what it represents just a fraction of the $34 billion consolidated in 2024.

According to the analysis firm, “the structural reason is simple: the base operation is broken.” Bitcoin funding rates average -1% in 2026, completely eliminating any arbitrage opportunity for hedge funds, which used to prop up ETF purchases when these rates were +6.2% in 2025 and +12.4% in 2024. With a recent average of -5% over the last 30 days, institutional paralysis is a direct result of the absence of financial incentives.

To explain it simply, many large investment funds – according to the hypothesis of 10x Research – did not buy bitcoin ETFs out of the conviction that the price would rise, but to execute an arbitrage strategy. This mechanism consisted of buying bitcoin through ETFs and, at the same time, selling futures contracts taking advantage of the fact that the market paid them a very high and safe return for maintaining that position.

Now that market interest has fallen and these rates have become negative, the operation no longer leaves profits, but losses. When this easy money incentive disappeared, financial institutions simply stopped buying ETFs..

Along with the disinterest of institutional funds, the retail sector has decreased its participation drastically. 10x Research shows that daily volumes in spot markets average $110 billion in 2026, up from $140 billion in 2025.

This decline is clearly seen in markets with a strong retail base such as South Korea, where daily volume fell to $1.4 billion this year, down from $2.8 billion in 2025 and $3.4 billion in 2024.

The explanation behind this behavior lies, according to the research firm, in the alternative performance of local stock markets: the Korean KOSPI index generated a return of 224% in the last twelve months driven by semiconductor companies, while bitcoin suffered a fall of 21% in the same period.

This disconnection is critical because, as the report points out, “the low interest in bitcoin is logical and not surprising” and “if the supply of retail investors is eliminated, the entire chain is broken,” given that they are the ones who raise the financing rates that make ETF arbitrage operations attractive.

Given this panorama, even the natural supply has changed, since miners are pressured to liquidate all of their produced coins to fund artificial intelligence hosting infrastructure, so “the only structural buyer that supports the price is a single entity [Strategy] leveraged company operating a preferred stock machine, and the miners who previously provided a natural accumulation supply have been replaced by sellers.

A strategy for now effective, but fragile

The report details how this single buyer operates under a strict time cycle tied to Strategy’s STRC preferred shares.

“The buying window is now completely determined by Strategy’s monthly STRC buying cycle. “Investors must own STRC by the 15th to qualify for the 11.5% month-end dividend, concentrating buying demand in the week or two before then.”

When this flow pushes the value of STRC shares towards its face value of $100, the company’s ATM program is activated, injecting the funds directly into the purchase of spot bitcoin.

According to the cited 8-K corporate reports, purchases are concentrated exclusively in this biweekly period and fall drastically thereafter. Due to the closing of the monthly buying calendar, 10xResearch warns that “the largest buyer in the market will be silent for approximately three weeks,” so “the realistic expectation for the next three weeks is that mechanical demand will be absent and that bitcoin will consolidate until the June cycle begins.” The direct advice to market participants is: “Trade the clock, not the narrative.”

From the x-ray of flows provided by the firm’s market analysis, it is evident that Strategy adds growing systemic risk to bitcoin price. By absorbing 70% of structural purchases in a context where the organic capital of ETFs and retail interest are paralyzed, the financial architecture of this corporation stands as the single point of failure of the entire asset pricing ecosystem.

The danger of this concentration model lies in the fragility of the capital engineering that sustains it. The operation of the perpetual issuance program depends entirely on the preferred shares maintaining their attractiveness and trading near their face value.

If the price of bitcoin were to experience a drop sharp enough to damage the company’s books or if questions arose about the sustainability of the 11.5% dividend, the market would lose the incentive to purchase these preferred shares. By trading below face value, the issuance machinery would come to a complete halt.

Faced with a disconnection from this financial engine, bitcoin would find itself in a situation of unprecedented vulnerability. Without the regular injection of billions of dollars, and with miners acting as forced sellers to cover their technological infrastructure operating costs, the spot order book would lack the organic depth necessary to sustain current quotes.

Absolute dependence on a single highly leveraged corporate entity exposes the asset to any internal turbulence or loss of confidence in said company immediately translating into a systemic correction of the price of bitcoin.

Strategy follows “a recipe for disaster,” says Ricardo Fernández

This is not the first time that the risks of Strategy’s actions have been exposed. On May 18, CriptoNoticias reported the analysis of Ricardo Fernández, a Chilean specialist in stock markets.

“The essence of the strategy lies in buying BTC with highly overvalued MSTR shares,” said Fernández. According to him, this mechanism can become “a recipe for disaster” if the market stops valuing Strategy at a high premium to its net asset value.

Fernández also warns about the growth of Strategy’s financial obligations. Currently, the company maintains more than $8.2 billion in debt and about $13.5 billion in issued preferred stock. These preferred instruments include series such as STRF, STRK, STRD and STRC.

He considers that this is one of the main risks of the model. “The 10% dividend on preferred stock and convertible debt obligations forces continued dilution or the sale of BTC, which undermines long-term value for shareholders,” he maintains.

Therefore, it seems that there is an absolute dependence on this company. If Strategy loses the ability to issue debt, the bitcoin market would suffer a serious systemic correction lacking real organic demand.