The euro represents only between 0.2% and 0.3% of the global stablecoin market.

Europe postponed the debate on rules for multi-issue stablecoins until 2027.

Europe enters a new stage of the debate on stablecoins. While the European Central Bank (ECB) maintains a cautious stance due to its possible effects on banking and financial stability, a report published on May 20, 2026 by the Bruegel think tank warns that limiting its development could produce the opposite effect: accelerate Europe’s dependence on stablecoins in dollars and weaken the role of the euro within the digital economy.

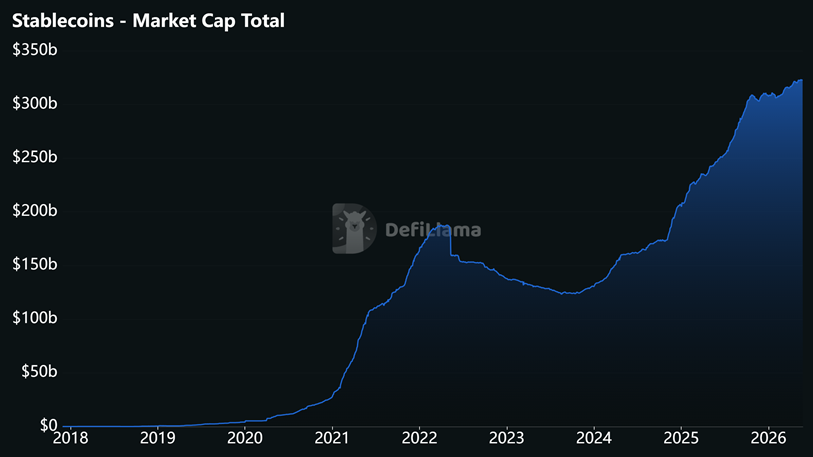

The discussion comes at a time when these assets have reached a scale that is difficult to ignore. Only in 2025, Adjusted stablecoin transactions exceeded 28 billion dollarswhile the total market capitalization exceeds 323 billion dollars.

Despite this growth, the ecosystem maintains an extreme concentration: About 99% of existing stablecoins are denominated in US dollars, while the euro represents only between 0.2% and 0.3% of global supply.

For Bruegel, this imbalance could lead to “infrastructure dollarization,” a scenario in which European tokenized markets—including payments, settlements, and collateral management—end up using dollar-linked instruments as an operational reference. In this context, the euro would continue to function as the official currency, but would lose prominence within the new digital financial networks.

It is worth noting that the warning appears while Europe is trying to build its own alternative, as reported by CriptoNoticias. Recently, the Qivalis banking consortium expanded its network to 37 financial institutions from 15 countriesincorporating entities such as ING, ABN AMRO and Rabobank to promote a stablecoin backed 1:1 by euros under the MiCA regulatory framework.

However, The project starts from a position of structural disadvantage. The European stablecoin market is located between 680 and 910 million dollarsequivalent to about 650 and 900 million eurosa reduced figure compared to the dominance of assets linked to the dollar, which already exceeds 311,000 million dollars.

The advance also occurs amid regulatory paralysis. The European Commission recently suspended a technical guide that sought to clarify the treatment of “multi-issue” stablecoins, that is, models where European and foreign issuers share the same fungible asset.

The ECB and sectors of the European Parliament questioned the proposal because they considered that this scheme could expose European reserves to external crises and reduce supervisory control. As a result, the debate was postponed until the MiCA review scheduled for 2027.

The United States advances while Europe debates

European concern does not respond solely to internal factors. While Brussels discusses limits, reserves and risks to financial stability, the United States moves forward with the Genius lawa regulation designed to promote stablecoins in dollars and consolidate their presence within the digital financial infrastructure.

Bruegel considers that This difference in approach could end up working in the United States’ favor. If Europe maintains restrictions that make it difficult to develop competitive alternatives in euros, part of the demand could shift towards stablecoins issued outside the bloc, reinforcing liquidity, adoption and the network effects already existing around the dollar.

Therefore, The report proposes making certain aspects of MiCA more flexibleremove the obligation to hold a large proportion of reserves in bank deposits, allow limited remuneration for euro stablecoins and facilitate closer integration with the ECB infrastructure.

Currently, the European debate no longer revolves solely around whether stablecoins represent a risk for banking or monetary policy. The new point of discussion It’s whether they have become too big to ignore.

With the United States actively promoting the digital dollar through stablecoins and concentrating close to 99% of the market, Europe faces a strategic decision: contain this ecosystem to protect its current financial architecture or accelerate the construction of its own alternatives before the next global monetary infrastructure is defined outside the euro.